You'd best start believing in RD stories

You're in one

CVX for REGI at $61.50/share???

We borrow and bastardize the iconic line from Geoffrey Rush’s Captain Barbossa in Pirates of the Caribbean. Renewable diesel (RD) is moving from the fringe to the mainstream in oil and gas, particularly if last week’s rumors of Chevron’s takeout of Renewable Energy Group (REGI) come to pass. Too much capital is being deployed in the space to ignore.

The setup

We started digging into renewable diesel about a year and a half ago. Finland-based refiner NESTE’s stock was bullet proof and its multiple kept expanding as the market valued the company’s global leadership in renewable diesel production at loftier and loftier levels.

NESTE Fwd EV/EBITDA

In the first half of 2020, HollyFrontier announced dropped a series of related announcements that found it shuttering two MidCon refineries with plans to convert them into renewable diesel service.

HFC’s announcements marked the early stages of an industry-wide explosion in renewable diesel projects and capacity growth for the 2020s.

Since then, every US refiner and integrated producer has announced plans to expand production of renewable diesel. Along with the established petroleum-based players, there have been several startups announcing similar plans to enter the renewable diesel space. We tally over $10 billion of capital committed to date for new renewable diesel capacity in North America, based only on projects with disclosed capital commitments. We expect the total amount of capital committed to the space in the 2020-2025 to reach $15-20 billion.

Friday’s REGI takeout rumors

The second of two speculative takeover announcements last week came last Friday after the close, when Bloomberg reported that Chevron was looking at a $3 billion deal to acquire Renewable Energy Group (REGI) at $61.50 per share.

According to the article:

Chevron Corp. is in advanced talks to buy Renewable Energy Group Inc. for about $3 billion, according to people familiar with the matter, as the oil major looks to make a big bet on green diesel. Renewable Energy rose more than 36% in after-market trading on the news.

Chevron is discussing paying $61.50 per share for Renewable Energy, said the people, who asked to not be identified because the matter isn’t public. A deal could be announced as soon as next week, the people added. No final decision has been made and the terms could change or talks could still fall through.

The deal would give a significant boost to Chevron’s push into renewable fuels, demand for which is expected to grow in the coming years as businesses and governments move away from oil and gas to cut carbon emissions. Chevron said last year that it expects to invest $10 billion through 2028 on low-carbon technologies.

REGI 2 year stock price history

What is going on? First a quick reminder on the renewable diesel industry.

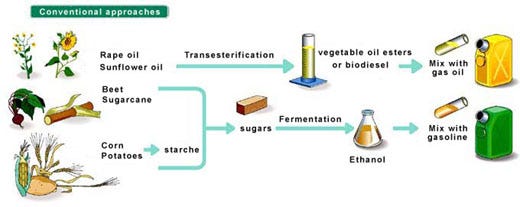

Biofuels 101: Biodiesel vs Renewable Diesel

Biofuels are fuels generated from biological material. Derived from biologic feedstocks, the lifecycle greenhouse gas emissions from biofuels are 20-80% lower than conventional hydrocarbon fuels, depending on feedstock. Well established in the US in the last couple decades primarily in the form of ethanol, the concept of biofuels in the transportation pool is deeply entrenched. Industry semantically breaks biofuels down into two groupings: Generation 1 and Generation 2.

Gen 1: first generation biofuels produced from feedstocks that are generally considered edible. First gen biofuels in widespread use today are ethanol and biodiesel. In the US, ethanol is generally sourced from corn and biodiesel from soybean oil. Of particular note are blending limits. Because the Gen 1 fuels are not chemically identical to the petroleum-based fuels they displace (ethanol-gasoline & biodiesel-diesel), they are subject to blending limits in the transport pool. In practice, ethanol is limited to a 10% blend wall in gasoline and biodiesel a max 20% of a diesel blend.

Gen 2: Second generation biofuels are produced from a wide array of feedstocks, including the edible feedstocks used in Gen 1 fuels, but also inedible feedstocks. The production process in Gen 2 biofuels is more complex and expensive, but results in a final product that is chemically identical to the displaced petroleum fuels. Thus, Gen 2 biofuels are 100% fungible with existing hydrocarbon fuels. Herein lies renewable diesel.

A summary of the puts and takes of the fuels.

Biodiesel vs Renewable Diesel Overview

The differences in chemical composition and eligibility for federal/state credits invariably place a higher valuable on renewable diesel relative to biodiesel. Biodiesel here is the inferior product and is gradually being pushed out as the renewable diesel industry ramps growth.

Renewable Diesel Capacity (billion gal/yr)

Who or what is REGI?

Back to our story where CVX is rumored to offer REGI $61.50. To speculate on why we first offer a cursory overview of what.

Renewable Energy Group today is the largest producer of biodiesel (not renewable diesel) with about 25% of total US capacity. It operates 11 plants with ~470 mm gal/yr capacity including a single renewable diesel plant in Geismar, Louisiana with 90 mm gal/yr production capacity.

US biodiesel production capacity (REGI in orange)

REGI is first and foremost a biodiesel producer of scale. It produces large quantities of biodiesel and much smaller volumes of renewable diesel.

REGI Production Volume (gal)

The company isn’t particularly transparent on feedstocks used in production of its fuels. We estimate its exposure to soybean oil ranges from 25-75% of total feedstocks depending on market pricing.

REGI Feedstock Mix

Exposure to soybean oil is of particular concern in light of ongoing weakness of the HOBO spread (generic diesel [Heating Oil] less soybean oil [Bean Oil]) that comprises its gross margin before the addition of environmental attribute uplifts (RINs, LCFS, Blenders Tax Credit). Show below, the biodiesel producer is deep in the hole before the inclusion of state and federal incentives.

Generic HOBO spread ($/gal)

Though, as commodity prices have rallied and renewable diesel feedstock demand has accelerated, the costs of any and all potential feedstocks for the production of biofuels have appreciated. Soybean oil as a feedstock yields poor economics, but even the cheaper feedstocks’ prices have rallied as well.

Various BD/RD feedstock costs ($/lb)

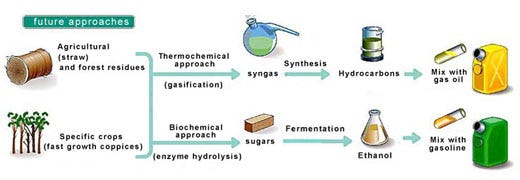

The REGI business model hasn’t been great owing in no small part in our opinion, due to REGI’s excess dependence on slowly-dying biodiesel as its main product.

REGI historical EBITDA & Free Cash Flow ($mm)

Writing on the wall with respect to a dim future dependent on biodiesel, REGI placed all its chips on renewable diesel. In 2020, the company announced plans to expand its small Geismar renewable diesel facility from 90 million gal/yr to 340 million gal/yr with a full rates targeted in 2024. Total estimated cost for the expansion stands today at $950mm, up from $825mm at the time of the announcement.

REGI 3Q21 Geismar update

With the base business generating insufficient free cash flow to support the addition of the $1 billion Geismar capital project, REGI raised $385mm in a follow on offering in 1Q21, issuing 5.75mm shares at $67.

REGI secondary

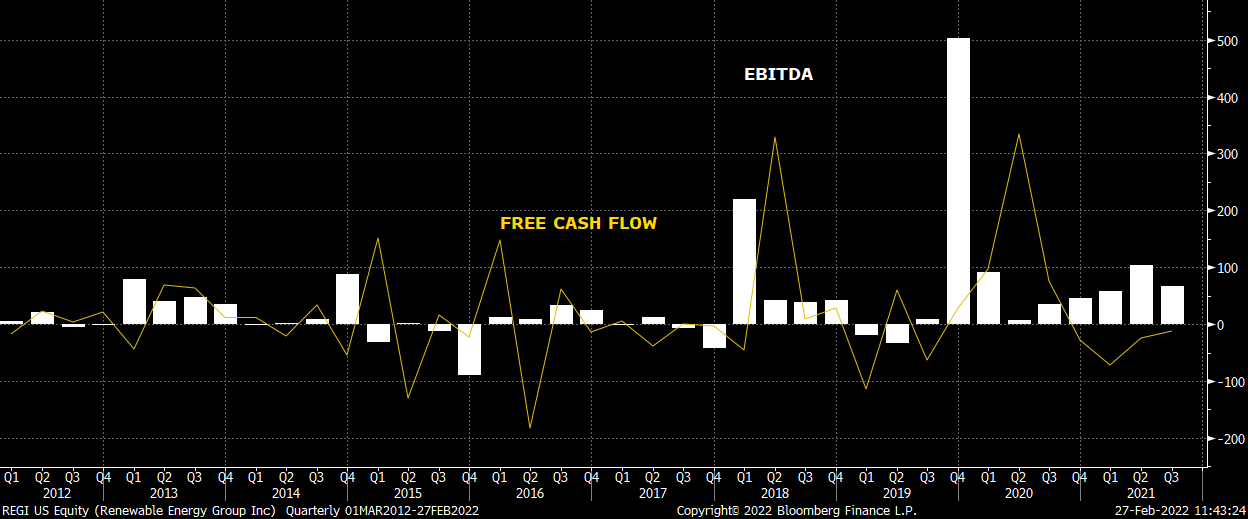

Slated to release 4Q21 earnings this week on 3/1, below we show the company’s most recent market cap at $2.2 billion and total enterprise value at $1.9 billion as of 9/30/21.

REGI mkt cap & EV

A recap of last week’s swirling rumors catches us up to today. On 2/23, before market open, REGI was said to have fielded takeover interest. Then on 2/25 after the close, Bloomberg followed up with the story that CVX was said to have offered $61.50 a share for REGI.

REGI YTD performance

To recap, REGI’s biodiesel business isn’t great. It has the potential for material margin/EBITDA uplift in 2024 with the startup of its large Geismar expansion, though ongoing pressure in gross margins and deteriorating value of environmental attributes muddy the prospects for a step change in value creation post-Geismar. Until 2024, REGI is by consensus estimates generating negative free cash flow every year (we take the under even on these given our stance on the viability of biodiesel as renewable diesel volumes hit the market). It’s just not a good business.

REGI Consensus Estimates

Why is CVX doing this?

They’re serious about decarbonization. They held a rather informative Energy Transition Spotlight Day last September where the company laid out plans for multiple paths to decarbonization across the portfolio - including a bold 100 kbd target for renewable fuels production by 2030.

Chevron Energy Transition Strategy

Starting effectively from dead zero (excluding a de minimus 2 kbd co-processing operating at its El Segundo refinery) Chevron last September announced its first step en route to 100 kbd renewable diesel production would come with a brownfield hydrotreater conversion to RD service. A few days ahead of the presentation, CVX also inked a JV with Bunge to develop low carbon feedstocks for yet-to-be-disclosed future renewable diesel production facilities. CVX contributed $600mm to the JV to facilitate Bunge’s expansion of existing soybean crush facilities.

News flow would suggest that Chevron indeed is committed to meeting decarbonization targets. In just the last six months it has announced other related enterprises with:

Iwatani: hydrogen fueling stations

Mercuria: CNG fueling network JV

Enterprises: carbon storage

Caterpillar: hydrogen collaboration

Gevo: sustainable aviation fuel

CVX is not pursuing its decarbonization targets solely in house and is using its scale and balance sheet to partner with existing expertise.

And based on last year’s Bunge announcement, Chevron seems to have an affinity for teeing up big announcements right ahead of analyst days (like this week’s analyst day on 3/1).

Valuation & thoughts on a possible deal

Horseshoes and hand grenades, the Bloomberg story from Friday says CVX offers $3B valuation and $61.50/share. REGI today has negative net debt, but that will be eroded over the coming years given the spending to get to the Geismar expansion startup. We use $3B as our valuation marker.

REGI Consensus EBITDA

The $3B valuation for REGI would equate to 10.5x EV/EBITDA in 2022, 11.7x EV/EBITDA in 2023, and 8.7x EV/EBITDA in 2024. For comparison, CVX is trading at 6.2x, 6.6x, and 6.7x 2022, 2023, and 2024 EBITDA.

We hope we’ve been clear in illustrating that REGI’s base biodiesel business doesn’t have a bright future. We hope Chevron sees it the same way and marks the NPV at $0 just as we do. That would ascribe all the value in the rumored deal to REGI’s existing/constructing renewable diesel operations at Geismar.

$3 billion for 340 mm gal/yr renewable diesel capacity equates to ~$8.80/gallon of constructed capacity. This number is off the charts relative to the cost of both greenfield and brownfield projects we’ve seen announced in the space - where the worst of these projects comes in at just over half the purported offer for REGI. We are tracking dozens of announced/in progress/under consideration progress and none have capital costs above $5/gallon of annual capacity.

Why would Chevron pay such generous terms instead of converting existing operations? This gets it done much quicker, we think.

Implications

For Chevron, we see little financial impact as the company is set to generate $25 billion in free cash flow in ‘22. Though we’d wager greater than 50/50 odds this gets written down below acquisition price by the time it reaches full rates. We don’t think this is a good deal for Chevron at all and they’ve rationalized it due to 1) 70% decline in REGI price since 2021 peak, 2) buying RD is easier than building RD, 3) likely misread on biodiesel economic outlook leading them to ascribe positive value for REGI’s biodiesel, 4) REGI possibly pulling the wool over CVX eyes with respect to unique ability to procure advantaged feedstock. We do not like this deal for Chevron on these terms.

For REGI, kudos. Management issued equity last year as the underlying business was crumbling and got a cash lifeline with the new project set to start in 2024. How they got $61.50/share from CVX will be a great story in time. Take the money and run. Well done.

For other renewable diesel producers with existing operations:

Diamond Green Diesel (50/50 JV between VLO and DAR). This is the most natural readthrough. DGD has two existing and one in-progress renewable diesel facility along US Gulf Coast with access to internal waterways for feedstocks and ocean for product delivery. We’ve no idea if CVX approached DGD, though we’d think it would make sense to have explored this. If REGI was able to milk $9/gal capacity for their facility, we’d contend DGD’s operations with lower opex, higher run time, and most importantly, legitimate vertically integrated access to lower carbon intensity feedstock, should command a material premium to REGI Geismar. A 25% premium would value DGD (full capacity post ‘23 DGD 3 startup) at $13 billion. A 50% premium would value the JV at $15 billion.

MPC: why didn’t CVX buy Dickinson? Is it because it’s deep inland without access to advantaged feedstocks and has high costs associated with moving it to best RD markets? This is a rhetorical question.

HFC: why didn’t CVX buy Cheyenne? Same question.

Viscosity Redux

viscosityredux@gmail.com