Yeoman's Work

Yeoman's Work

VLO shares macro insight & we share an Indonesian colloquialism

VLO rehashes our natural gas-diesel commentary

On their 4Q21 earnings call today, VLO had the following to say about high international gas prices:

“You see some switching of crude diets as a result of the high natural gas prices still $30/MMTU in Northwest Europe, so you see some people kicking out medium and heavy sour grades of crude … So people idling and cutting hydrocracking capacity as a result of very high natural gas prices which again puts less diesel on the market and is one of the reasons why we’re experiencing all the tightness around diesel.”

We again contend that the globe is not short crude, it is short diesel. The market is bidding up diesel to incentivize refiners to produce more of this secondary product.

As VLO puts it, the high price of natural gas (the highest single contributor to a refiner’s operating expense) has forced either outright closure or process reconfigurations, especially in the marginal European refineries.

Those refiners that are staying online are doing so in part by eschewing heavy sour crudes and running crude grades that require less natural gas to process into products. This has naturally resulted in less diesel production (and more gasoline production) than would otherwise be the case.

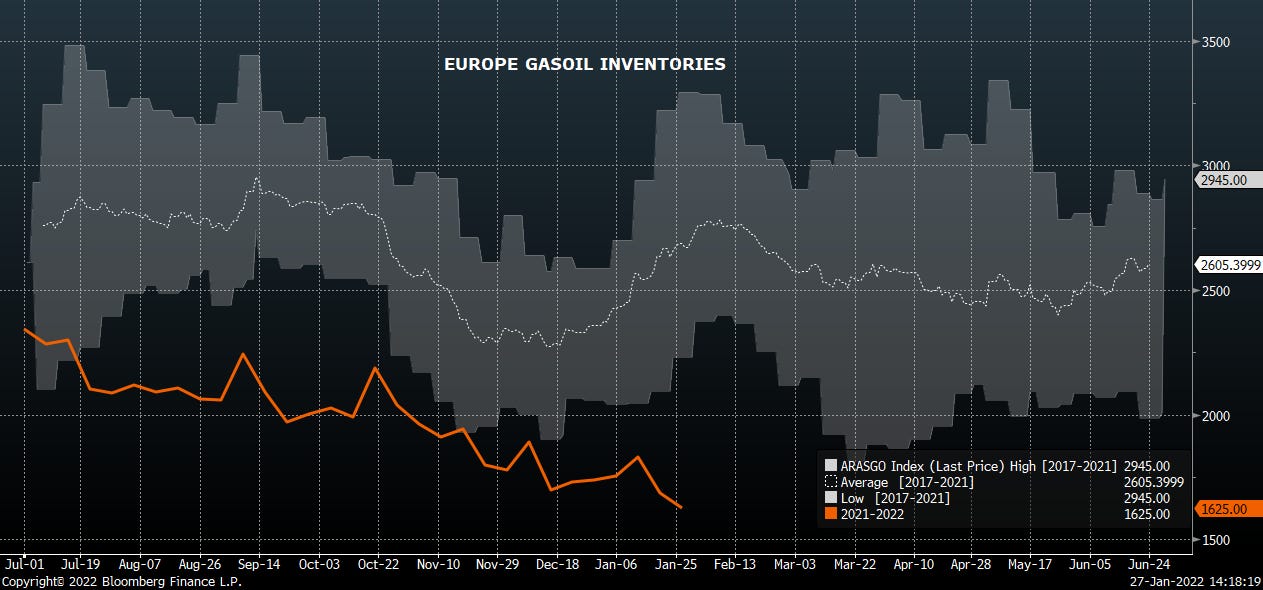

European gasoil inventories have remained pressured and well below seasonal norms.

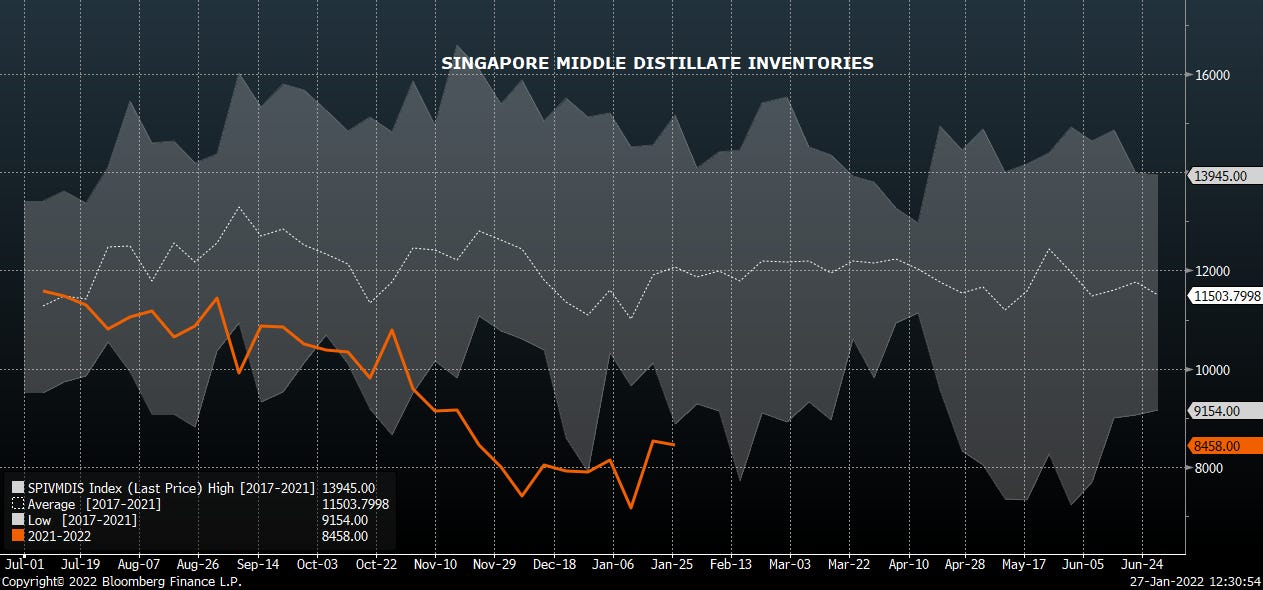

The same trend in Asia.

European natural gas prices are arguably the most relevant input into the calculation of how global diesel inventories trend from here. Where inventories go, crude prices will move inversely.

Hence the continued emphasis on Russia natural gas imports into Europe and how this fiasco in Ukraine evolves. Another potential respite-inducing anecdote in that vein today (heavy emphasis on the word “anecdote”):

To reiterate our thinking, we do not believe the market is in the early innings of an energy supercycle. We’ll try to post data that supports this contention, and begrudgingly make an effort to share data that contradicts this as well.

There’s an expression in Bahasa Indonesia that has stuck with us for years: hati-hati

We remember hati-hati as translating in English as something akin to “watch out” or “beware.” Here’s our hati-hati chart of the day as it pertains to energy markets.

The premise is simple enough, energy equities and option-adjusted spread (OAS) should travel in opposite directions (we’ve inverted OAS above for aesthetic reasons). As junk debt prices less risky in the market, so too should the equities.

OAS reached their lows in early 4Q21 and after a brief bit of tightening that started in December, have begun to widen again. The equities have not followed suit, and in the last week or so have rallied despite the fixed income part of the energy cap structure telling us that’s the wrong direction to move in. It will be hard for these two to move directionally divergent for long.

The relationship between the two indeces has been consistent since the COVID vax lows. The gap today is worth noting.

Energy equity index vs Energy HY OAS since 11/10/20

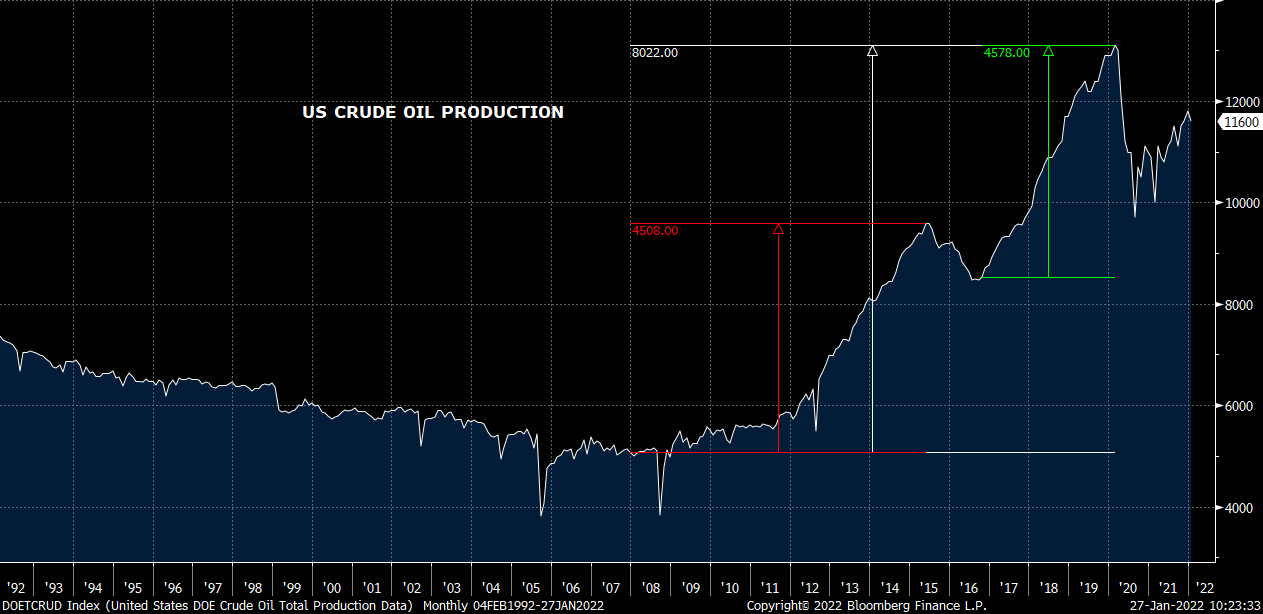

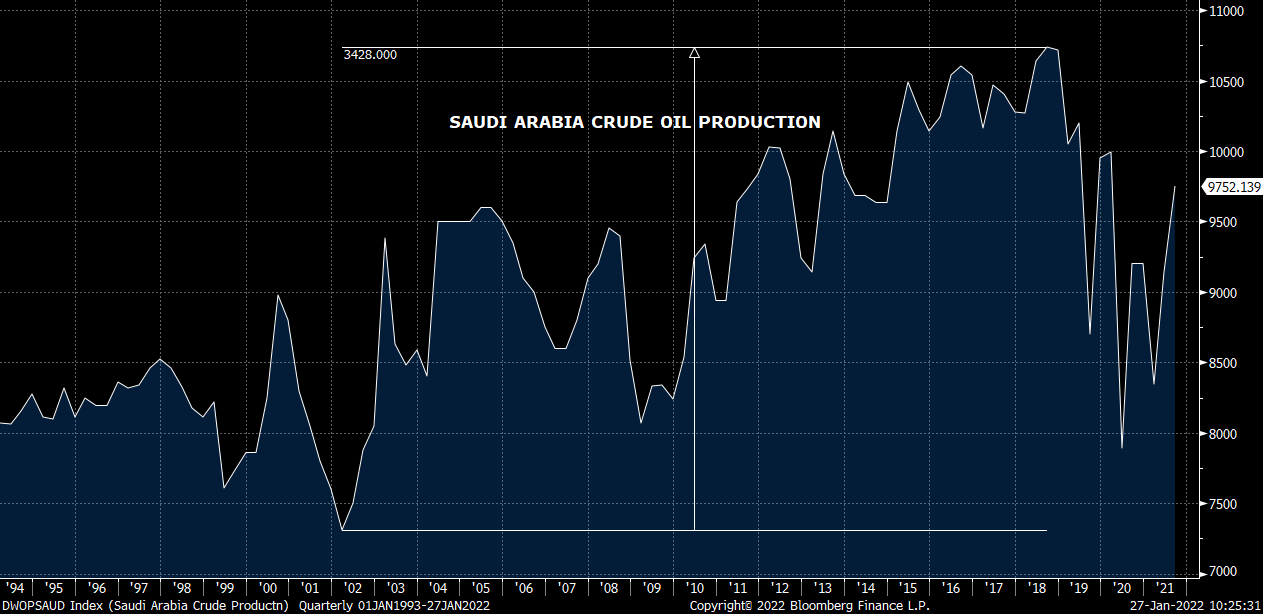

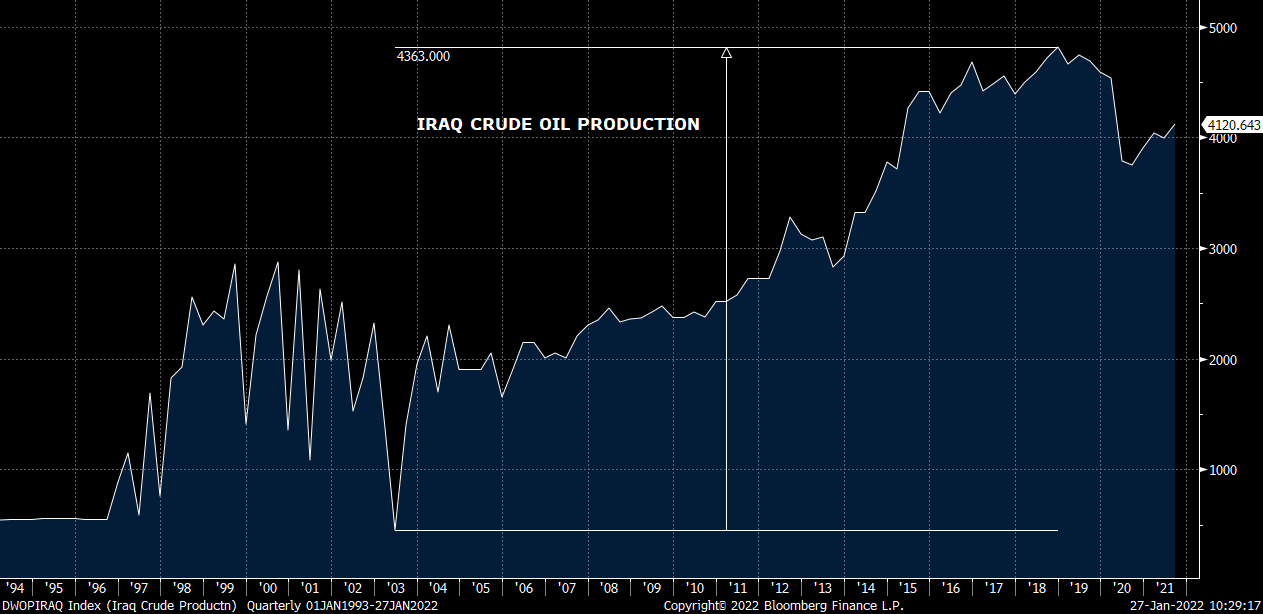

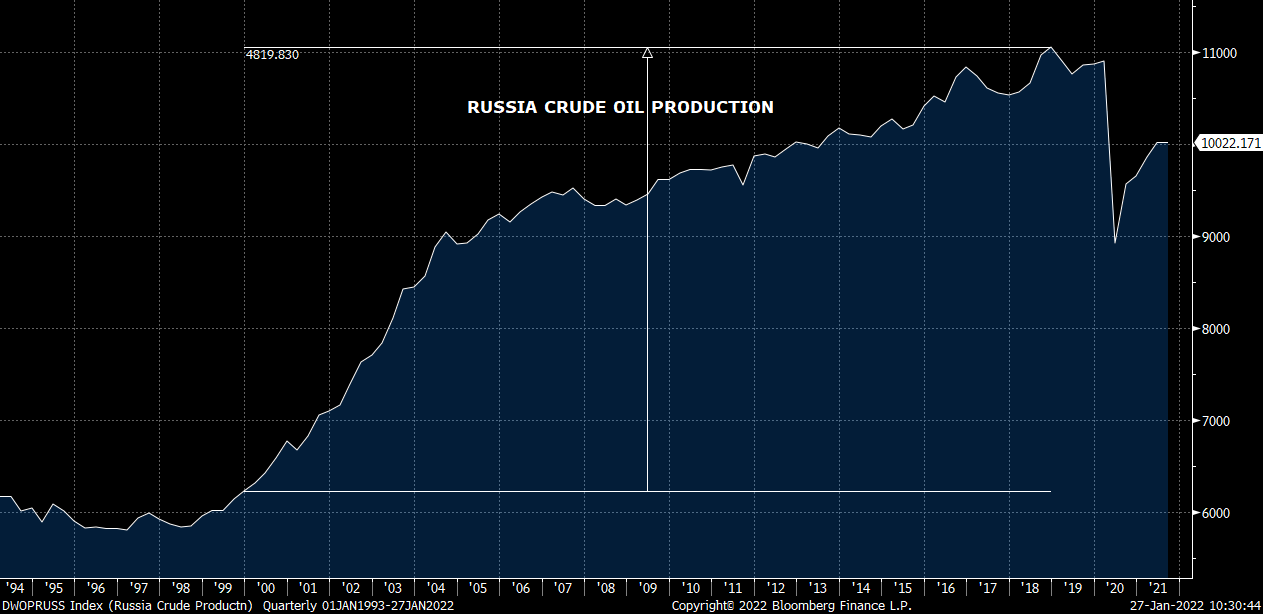

Fun Fact

Did you know that the US has grown crude oil production by 4.5 mmbbld twice in the last decade or so? First in the initial shale boom, then again after the post-OPEC ‘14 crash reset.

What other country has performed this feat this century?

Saudi comes close, but not close enough.

Canada’s growth has been impressive, but not nearly at the absolute level to have achieved this level of growth.

Iraq has, but if you start measuring from the 2003 war lows. That’s kind of cheating.

The answer is Russia.

Valero Reports 4Q

We’ve been hyper focused on the US refining segment recently, under the premise that the market is miscapitalizing earnings across the subsector for a number of reasons.

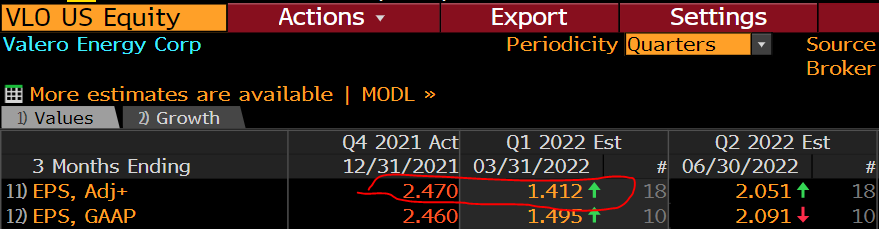

The headline: Adjusted 4Q22 EPS of $2.48 exceeds consensus at $1.82. By segment, North Atlantic & ethanol are the be biggest positive outliers vs expectations.

Refining is thought to be one of the hardest energy businesses to model, rightly or wrongly. Many of the refiners have kindly taken to regularly reporting “indicated margins” on their websites to help directionally guide analysts. VLO does the best job - see for yourself.

VLO Indicators

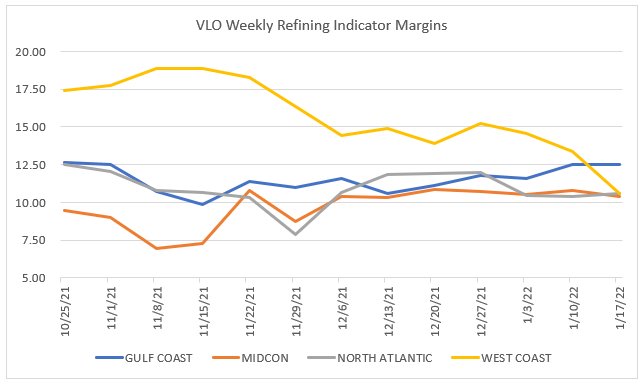

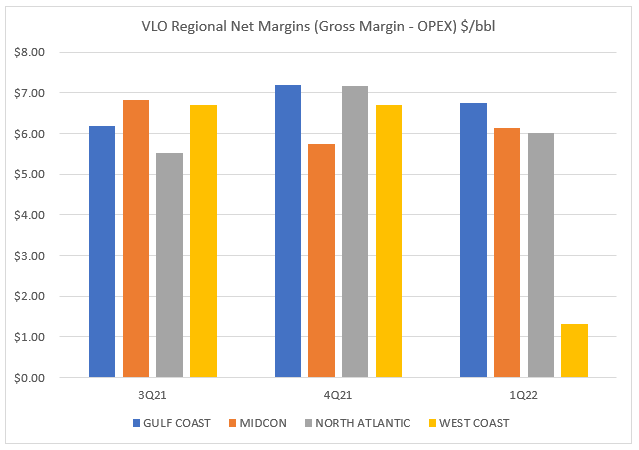

VLO’s reported regional refining indicators generally ended the year on a high note.

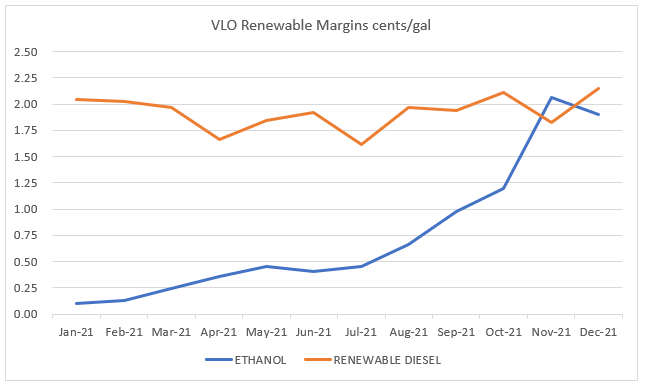

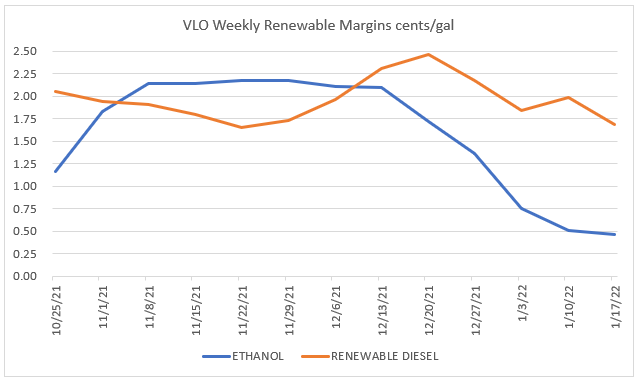

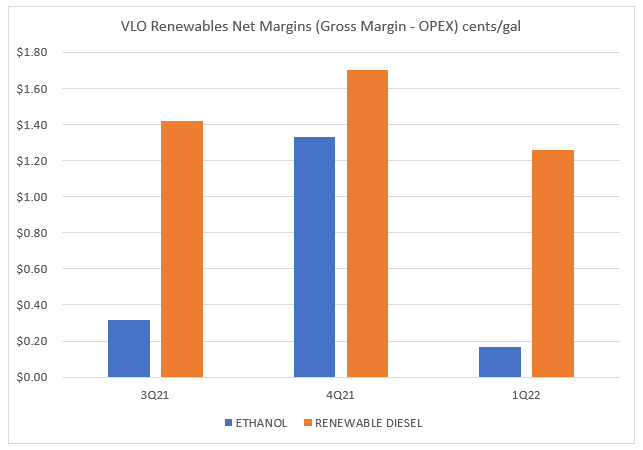

Their renewables segment, consisting of ethanol and renewable diesel product lines, similarly finished with strong indicated margins at the end of the year.

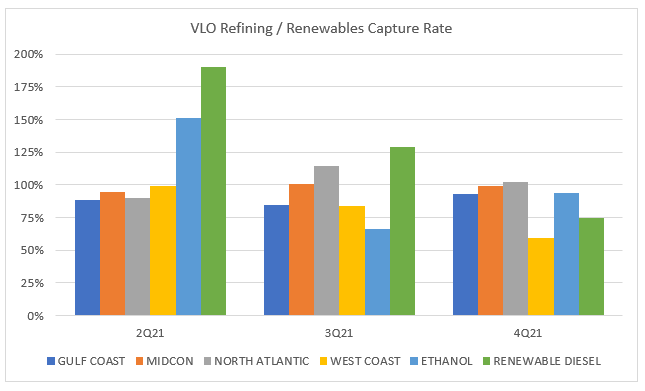

The analyst’s value-add in covering the refiners is to guesstimate the “capture rate.” This is how much of the indicated margin the company actually delivers. Note that regional capture rates have been trending flat/down throughout 2021

The indicator trend, though

We remind ourselves that stocks are (ultimately) forward looking. We look at the trend in weekly indicators from late 4Q21 into 2022 YTD. Not exciting for refining.

Even less so for the renewables.

Extrapolating YTD gross margins, historical capture rate, and 4Q21 opex, we get the following outlook for 1Q22 margin. Generally down sequentially.

Ethanol is going to be a big headwind. 4Q21 was a windfall - thanks to low ethanol inventories and associated high crush margins. But that gift has faded as inventories have caught up and breeched the high end of the 5yr range .

We expect VLO’s ethanol to print 1Q22 near breakeven. This alone could be over $0.75/share earnings headwind from 4Q to 1Q.

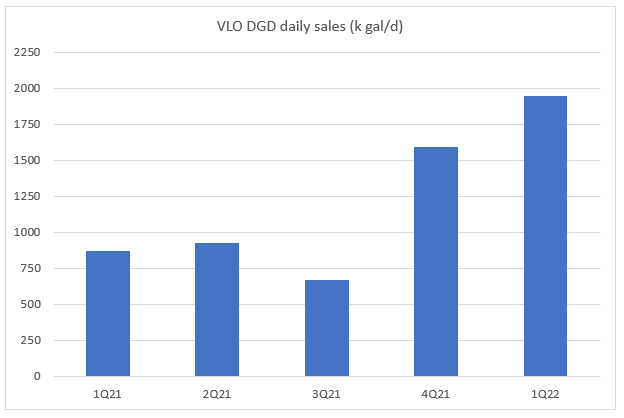

With a full quarter from the recently started DGD Phase 2 in its renewable diesel (RD) segment, VLO’s RD prospects look better. Increased throughput will offset a good chunk of the sequential drop in margins.

Consensus already has a drop in sequential earnings baked in.

If the admittedly early YTD trajectory holds, VLO is looking at sequential earnings decline in its refining business, a sharp drop in ethanol earnings, and flat renewable diesel contributions.

We’ll take the under on $1.41 for 1Q, though it should be a while before the negative revisions start rolling in. And this is the refiner we’re long!

As we said earlier, the market has utterly miscapitalized every refiner. We just prefer this one’s competitive positioning vs the others. We’re holding this long fully expecting absolute downside, but just not as much as the offsetting short. We don’t like the risk/rewards skew for a long in the refining group at all.

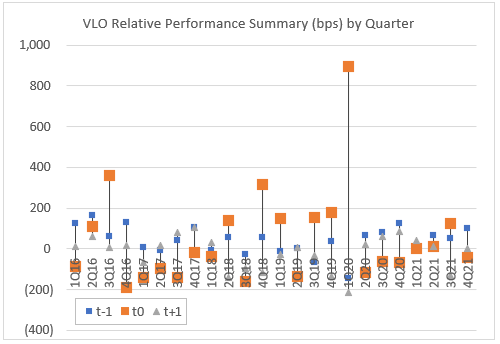

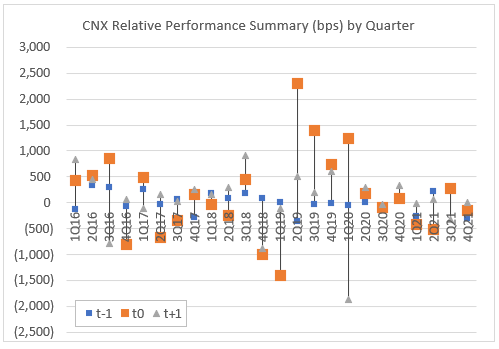

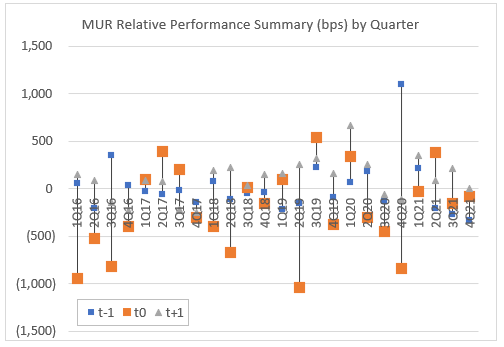

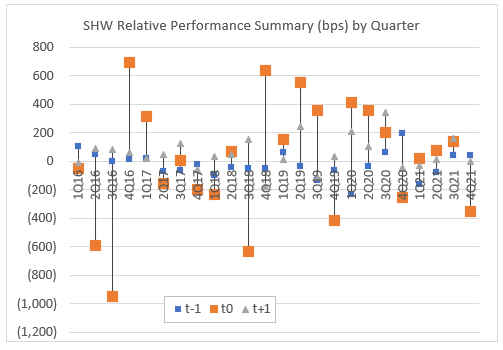

Today’s Earnings Performance Charts

VLO. Unremarkable.

CNX. Same.

MUR. Again sidesteps the plague of blowups on earnings reports that once plagued the name.

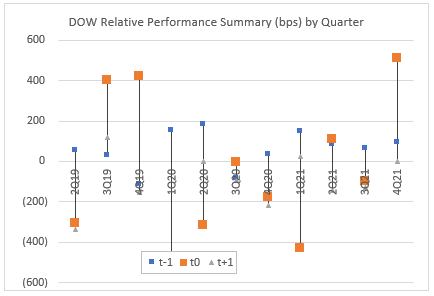

Interesting in the Chems space, you’ve got the Value vs Growth on in spades. Commodity chems DOW crushing specialty chems SHW

SHW. Rare earnings disappointment, after a series of recent guidedowns that had already knocked the name.

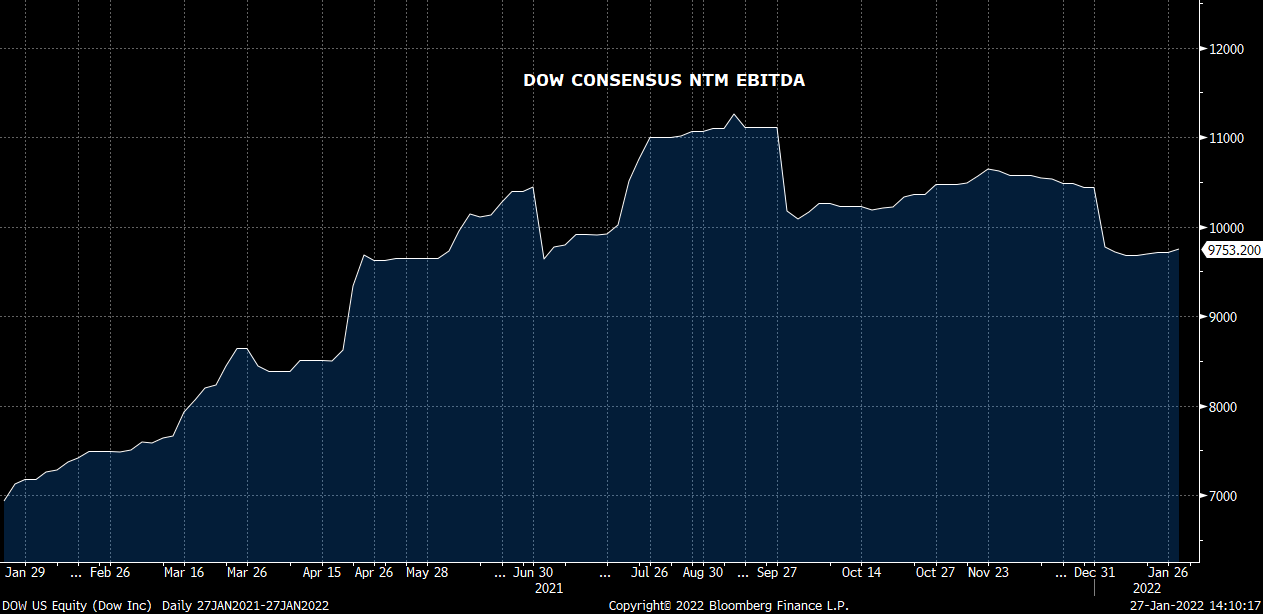

DOW. Big day for this name that’s been battling the prospect of peak earnings.