Whither demand (analysis)?

We broadly classify the drivers of oil price as supply, demand, and macro. Qualitatively, we find that the demand component always gets short shrift on the analysis front. One can speculate as to why. We think it’s in part because it’s much easier and intriguing for the barrel counter to traipse the globe (in Excel) adding up production from various contributors.

We are of the mindset that a fulsome approach to crude oil analysis will ask - why are the purchasers of crude oil buying crude oil?

A terribly brief intro into crude demand:

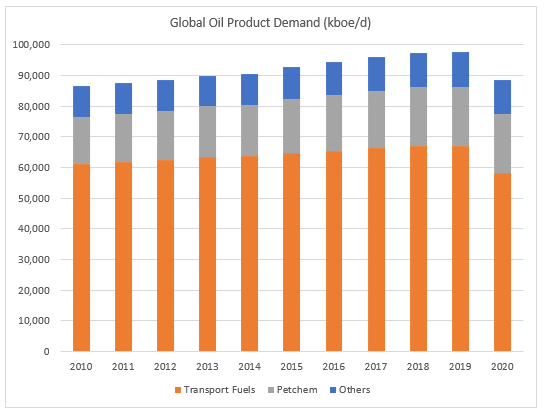

No consumer directly burns crude oil for final use, it’s purchased and processed by downstream intermediaries (refiners) that convert it into a range of products for ultimate end user consumption. We aggregate the categories of oil products into transport fuels, petrochemicals (petchem), and other.

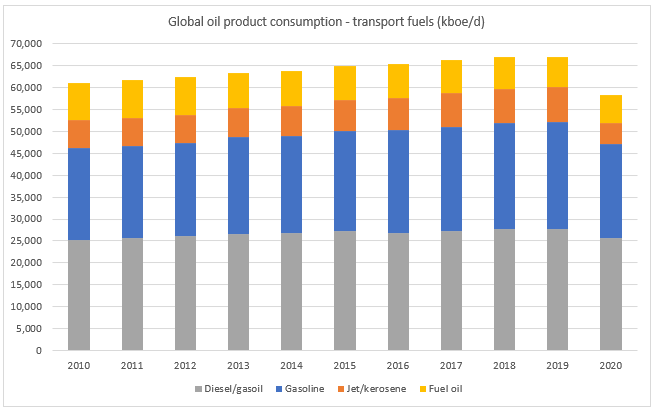

Transport fuels are the workhorse of global oil demand on an absolute basis, running about 70% of total oil product consumption. Within transport we include gasoline, diesel, jet, and fuel oil. Globally, diesel consumption just inches ahead of gasoline in the 27-30 mmbbl/d range (ex-COVID of course). Jet comes in next in the steady 6-8 mmbbl/d range (ex-COVID again). Fuel oil clocks in at a similar 6-8 mmbbl/d level.

Courtesy of the EIA, we share the definition of petrochemicals:

“Organic and inorganic compounds and mixtures that include but are not limited to organic chemicals, cyclic intermediates, plastics and resins, synthetic fibers, elastomers, organic dyes, organic pigments, detergents, surface active agents, carbon black, and ammonia.”

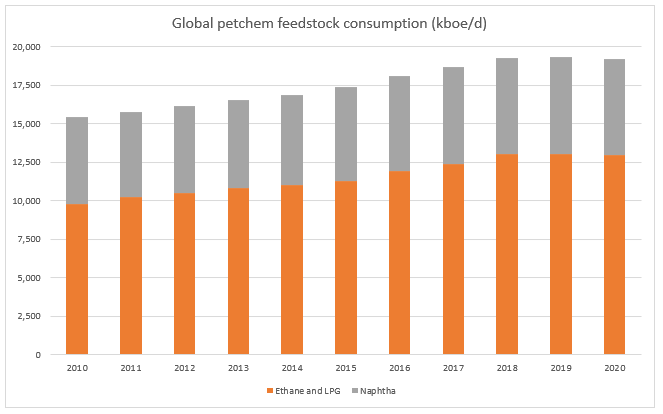

Feedstocks for production of petrochemicals are often

“derived from refined or partially refined petroleum fraction, principally for use in the manufacturing of chemicals, synthetic rubber, and a variety of plastics.”

In this layman’s terms, part of the refined crude oil’s product stream is used as a feedstock to make plastics and a bunch of other chemicals. The base feedstock categories, derived from crude oil, for our purposes are ethane/liquefied petroleum gas (LPG) and naphtha.

Nearly 20 mmbbl/d total consumption up from 15 mmbbl/d in 2010.

The following chart was the reason for the post. A holistic view of energy markets should in our opinion include a healthy analysis of demand, on par with supply, alongside with macro.

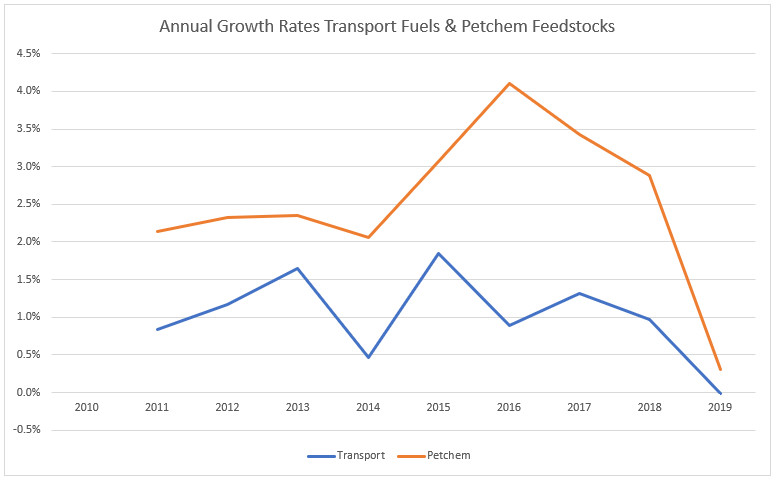

Global demand growth for crude oil has for years been driven by the growth in petchem industry - a growth rate (yes, off a lower base) that is multiples of the traditional transportation demand growth.

If you’re watching crude, watch demand as much as you watch supply. If you’re watching demand, pay special attention to global petchem trends.

Petchem is the future of crude.

We stopped the graph at 2019 for illustrative purposes, but in case the reader is wondering, demand for transport fuels and petchem feedstocks dropped 13% and 0.5% in 2020, respectively.

Petchem is the future, but diesel is the here and now.

A quick reminder to take a gander to discern why refiners are buying crude. What is driving their economic decision to purchase the feedstock for conversion into products?

Globally, gasoline + diesel represent >50% of total oil product demand. We start there.

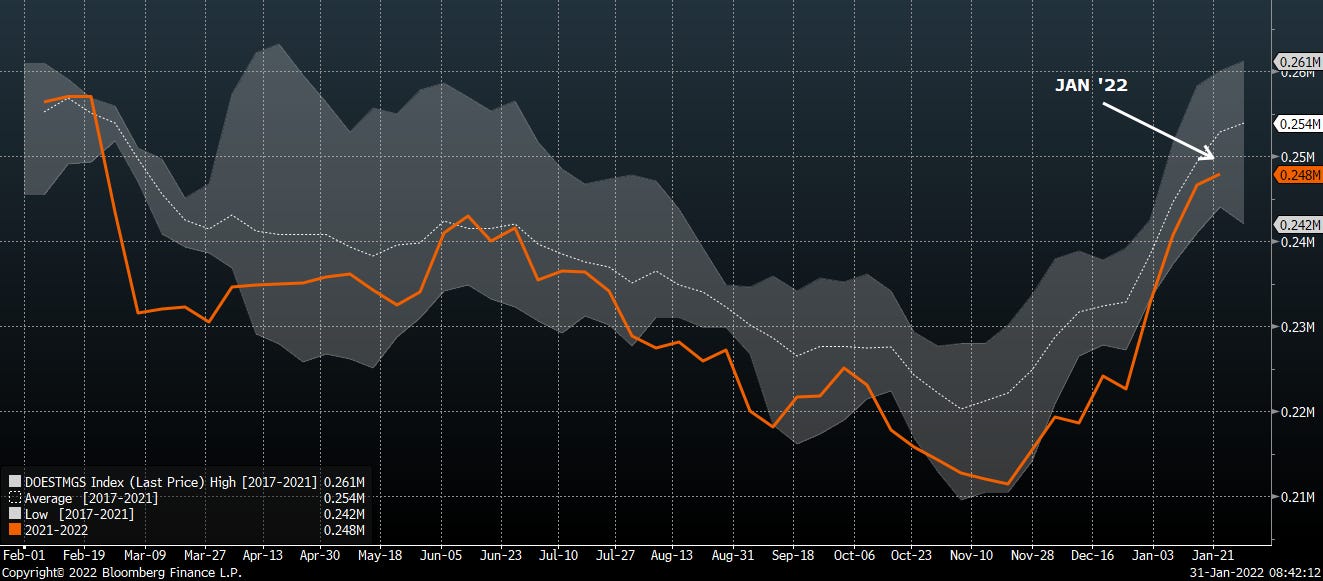

It’s not gasoline. Inventories are effectively in normal territory, having quickly made up a seasonal deficit in 4Q21 with some big builds.

US gasoline inventories

In fact, adjusted for inflated pass-through costs (RINs, etc…), refiner economics for converting crude oil into gasoline today are little changed versus the prior year. This is not the reason they’re in the market for crude.

US generic adjusted gasoline crack

Diesel, however, is a different story.

Cracks are strong, unusually strong.

Regional generic diesel cracks

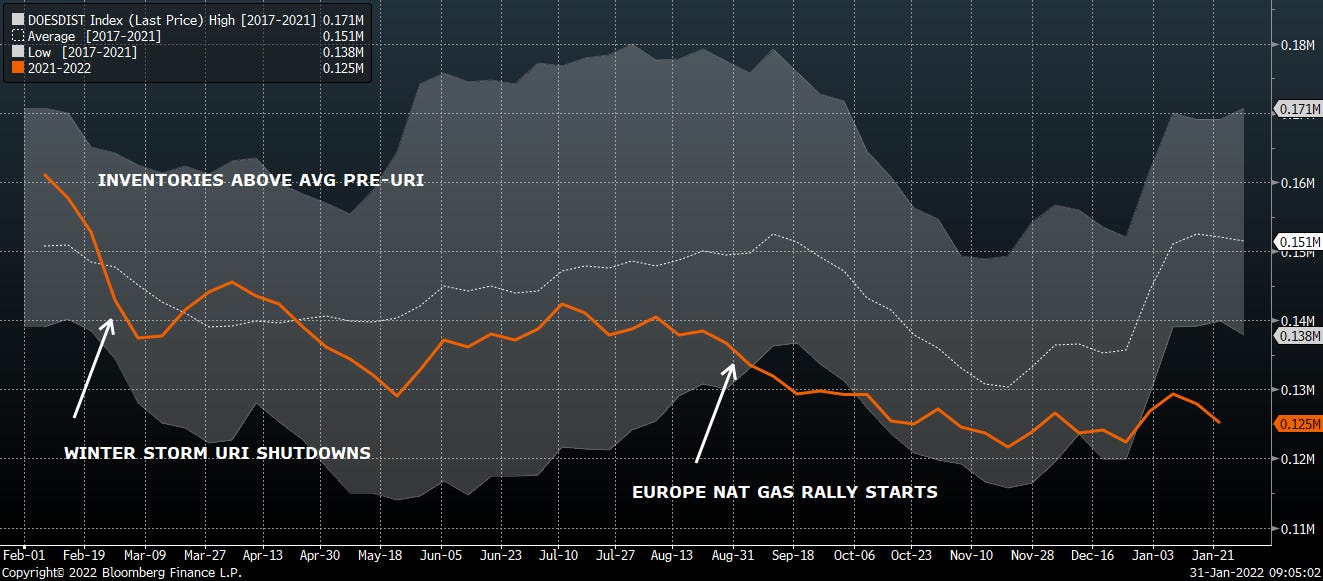

Because inventories are low.

US distillate inventories

As long as global storage hub inventories stay depressed and refining operating costs stay elevated (international nat gas prices), there will be a bid for diesel and derivatively, crude oil. We will be watching inventory trends (is Asia starting to normalize, or is it noise?) and fundamental data to look for future direction.

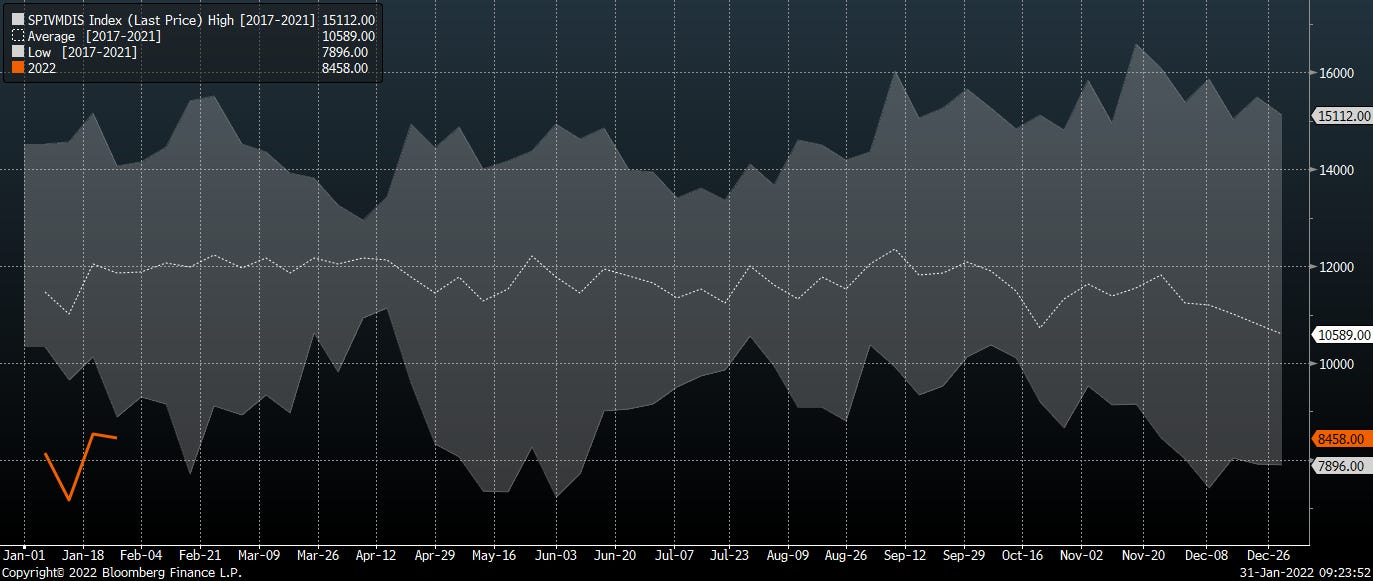

Singapore middle distillate inventories

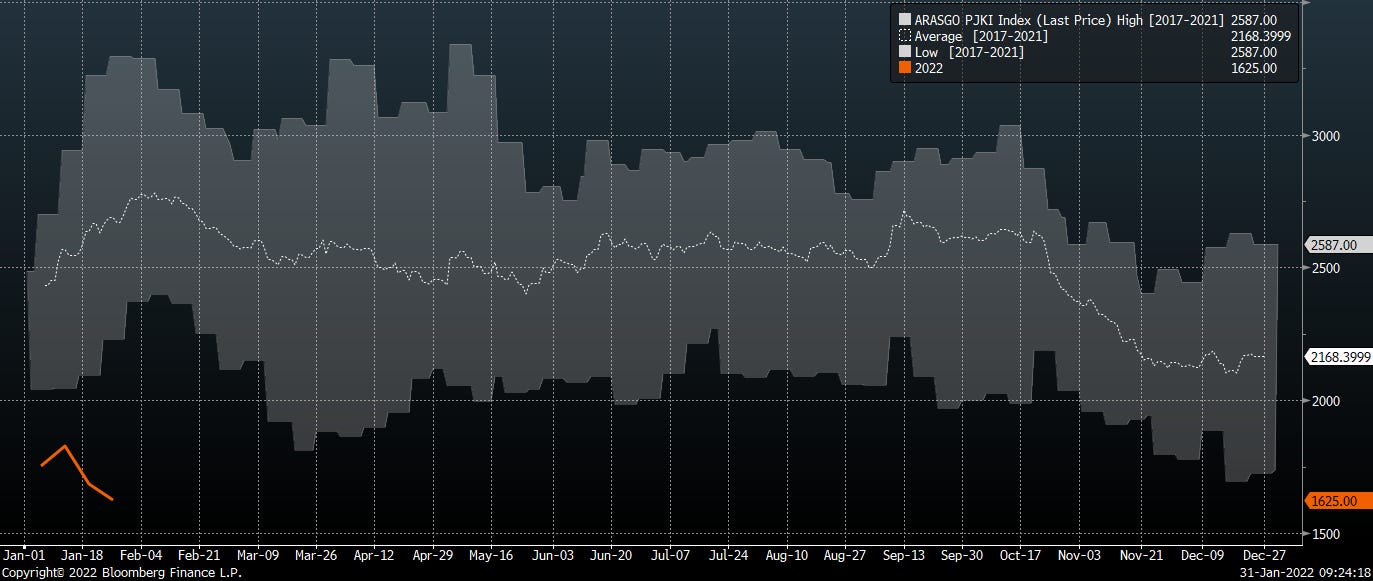

Europe gasoil inventories

We urge investors to pay attention to refined product demand as much as the supply side narrative.

Refiners aren’t bidding up crude because they’re worried OPEC won’t meet its quota - they’re buying because they’re making money turning into products - especially diesel.

Up Next

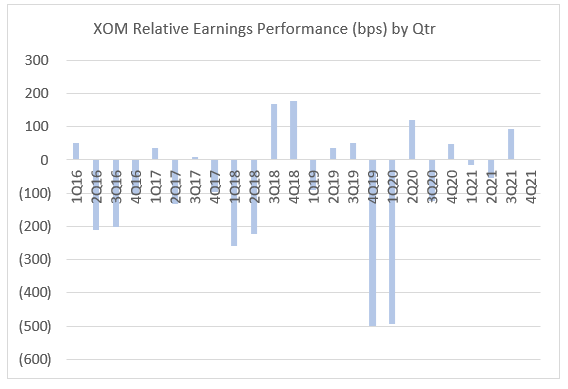

Pet project XOM reports 4Q21 earnings tomorrow before the open. Consensus is looking for $1.93 EPS in 4Q and $6.35 in 2022.

Peer CVX missed and underperformed the group last week, XOM could right the large cap ship if it’s able to more deftly navigate some of the headwinds CVX suffered. CVX surprised the market with weak production guidance due to expired Production Sharing Contracts (PSCs) and mismatch on LNG sales timing. We’d be surprised if XOM hit the market with similar bad news on this front, though we do note that higher commodity prices will mathematically have a negative volumetric impact on the company’s PSCs due to reduced company takes - risk to downside on price-driven impacts, but not the evaporation of entire contracts like CVX.

A 5 yr lookback shows that XOM has in recent quarters turned in better stock performance in/around earnings days after years of pretty consistent underperformance. Here’s to hoping for a decent quarter and outlook…

Something interesting to your point on the portion of demand, petchems and transportation fuels - increasingly petchems making up a larger component of demand, but inventory data very lacking vs. crude and transportation fuels. The result: "days demand is very low". Focus increasingly needs to shift to what crude oil supply demand, ie. Refinery demand, is vs. "oil" supply demand.

Naive question about demand -- I remember reading a few years ago a prediction that aviation would be one of the main sources of increased oil demand. The argument went that the number of passenger miles traveled per year would triple in the coming decades due to increased flying from the new middle class in EM countries, and also there would be a lack of more fuel efficient engines.

Obviously COVID might have permanently reduced demand from flying (e.g. it sure does feel like China might not re-open up years), but otherwise what are your thoughts about that bull argument?