What is Alpha?

A crash course in “alpha”

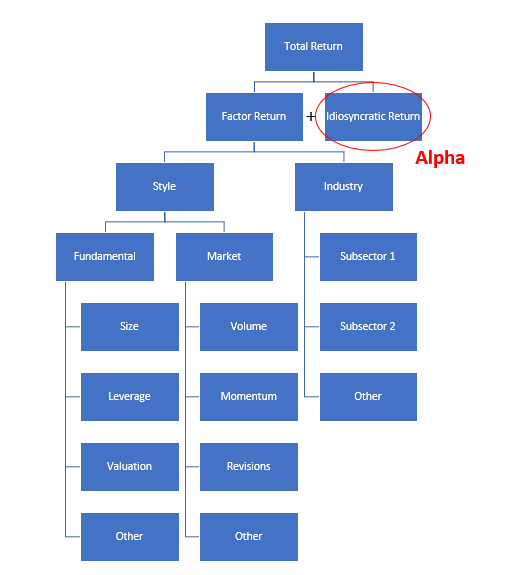

The performance of a stock, or any financial asset for that matter, is a function of multiple inputs.

The more sophisticated shops disaggregate asset returns into different buckets. They use risk models to find structure in the markets to identify sources of correlation.

Once they attribute all of an asset’s returns to other correlated drivers, the remainder of the (uncorrelated) return is the idiosyncratic return - or Alpha.

Alpha is thus imputed - not calculated - as it’s the unidentified leftover of returns once everything else has been accounted for.

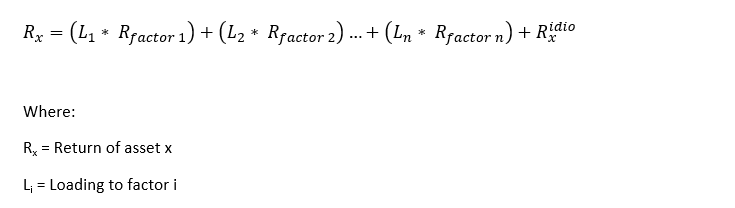

Mathematically:

Expanded:

The horsepower in the big shops is dedicated to identifying the factor risks and correlations. The more accurately they can attribute factors’ contribution to a return stream, the more they can hedge away and optimize capital allocation on idiosyncratic risk. Some firms look at a few factors, while others drill down into tens, even hundreds of factors in the effort to strip out everything that is not alpha.

To illustrate, a conscientious risk manager will look at their portfolio and see where their aggregate momentum exposure lies. If they’re long too many names with high momentum, they may be asked (or told, depending on the firm) to reduce momentum exposure and approach a more neutral stance. This is repeated ad nauseum across the breadth of factors a firm decides to monitor and manage.

Why focus on factors and alpha?

Play to your strengths. Good stock pickers are really good at finding alpha. Like - they have 0 edge in market timing or factor selection.

Few stock pickers generate exceptional risk-adjusted returns in discretionary factor risk allocation. The market participant that is able to create outsized P&L by timing exposure in the Size factor, for example, is exceedingly rare. So the big funds measure and manage factor exposure and focus on alpha.

There is of course a side benefit to targeting idiosyncratic risk exposure that is spoken about in hushed tones:

The less factor exposure in a portfolio - the lower the portfolio’s daily volatility.

The lower the volatility - the more leverage it can (ostensibly) handle.

The more leverage on a book - the higher the returns on equity (if the manager is correct in security selection).

How and why we do what we do

Having spent the bulk of our careers on the buyside in terribly volatile cyclicals like Energy, we’re conscientious of net risk exposure and the potential for volatility to move exponentially at any moment.

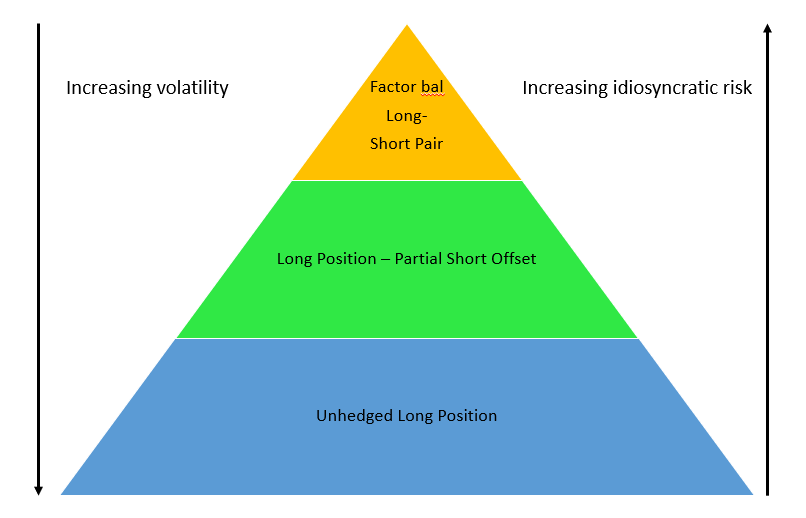

We are advocates of employing a risk model and targeting a certain level of minimum idiosyncratic risk exposure - cognizant of the fact that low idiosyncratic risk allocation is a bet on the market, while high idiosyncratic risk is a bet on one’s stock picking acumen. We believe there are rare periods wherein low idiosyncratic risk is acceptable, but for our risk tolerance, we like to run a portfolio with a high idiosyncratic allocation more often than not.

We pair trade. A long position gets an offsetting short position. We aim for the long to outperform the short, independent of market direction or factor performance.

The name of the game is capital preservation and staying in the seat.

Trades 1/25

We were unusually prescient in covering DVN short and going long yesterday for +940bps VWAP-VWAP. We’re not that good & won’t be annualizing those returns.

We’re cutting a couple losers in the book at a loss. We’re early and wrong and taking our lumps:

SHW-LYB (-7.2% return). SHW is a great company, but it’s too expensive and growthy for this environment. We’ve exited SHW and moved the LYB short to the existing VLO long

DAR-MPC (-14% return). We really like the DAR business model but it’s the second biggest player in a thematic renewables market that is slowly being uneconomically overcapitalized by recent entrants (US refiners). We’ve flipped to DAR short vs a new BG long (we like mmore after today’s ADM report). We continue to believe MPC is buying back its stock at >50% premium to fair value and are looking for negative ‘22 revisions (only because half of its refining business is incinerating cash today), so we’re keeping the short and adding a PBF long under the premise that the market buying one uneconomic refiner in MPC will buy more of an even less economic refiner in PBF

In addition to new pairs VLO-LYB and PBF-MPC today as a result of position shuffling, we’ve added ADM-NESTE. The former is derisked after a respectable earnings report and the latter is undergoing a monster derating as its moat is being whittled away by desperate competitors.

Trying a new depiction, we show the portfolio’s open and closed positions & life to date return by day below. Today was the final day on SHW-LYB and DAR-MPC.