We're running out of oil?!?

We're running out of oil?!?

Quick - buy the companies that are short oil and ignore the premium valuation

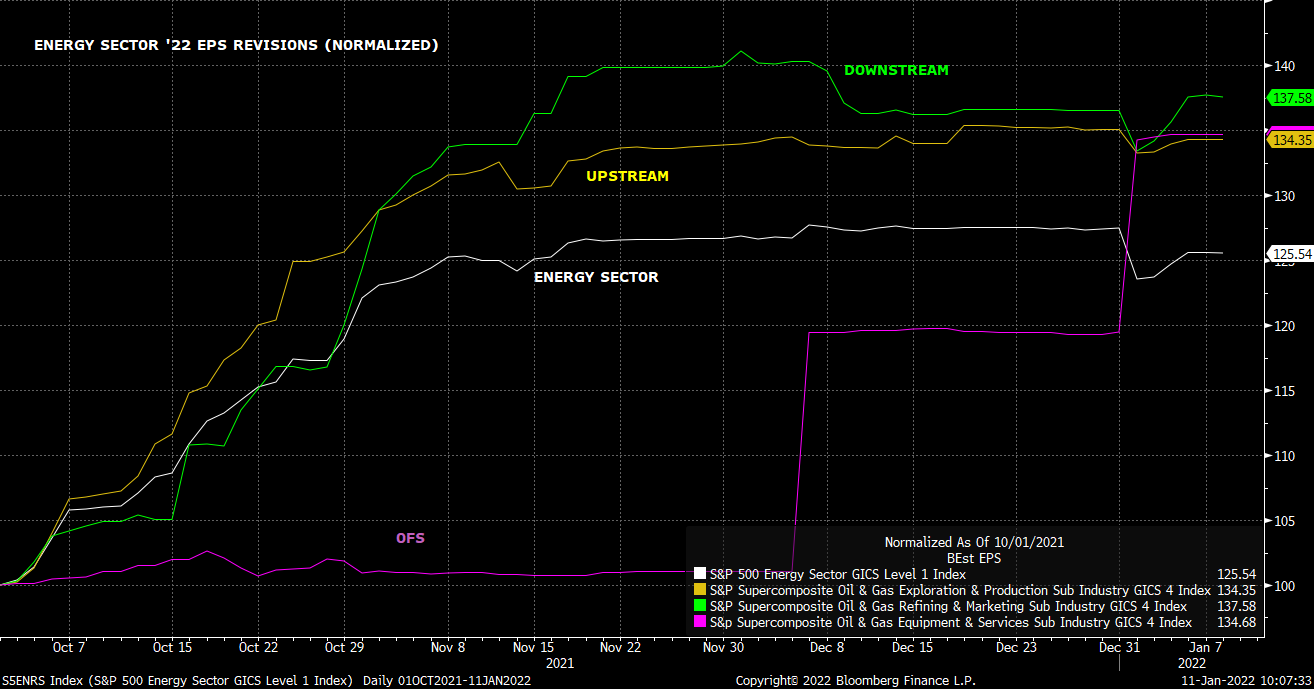

How have 2022 earnings estimates for the group trended over the last three months? Pretty uniform positive revisions, interestingly. Each subsector has seen ‘22 estimates up ~35% since the beginning of 4Q21.

Then how have these earnings been capitalized by the market? What is each subsector’s forward multiple today vs history?

Note the trend. Once NAM shale took off in 2010, multiples were generally flat/up small until the OPEC price war in late ‘14. As happens when earnings collapse, multiples expanded until peaking in ‘16 at the beginning of the sector’s recovery. Multiples continued to compress into the COVID crash of ‘20.

Then, once more, earnings collapse = multiple expansion. Subsequent recovery = compression.

Except for the expansion in the last couple months, that is…

How have multiples trended recently vs the 10 yr pre-COVID average? Downstream trading at a premium. OFS slight discount. Upstream at a hefty 35% discount

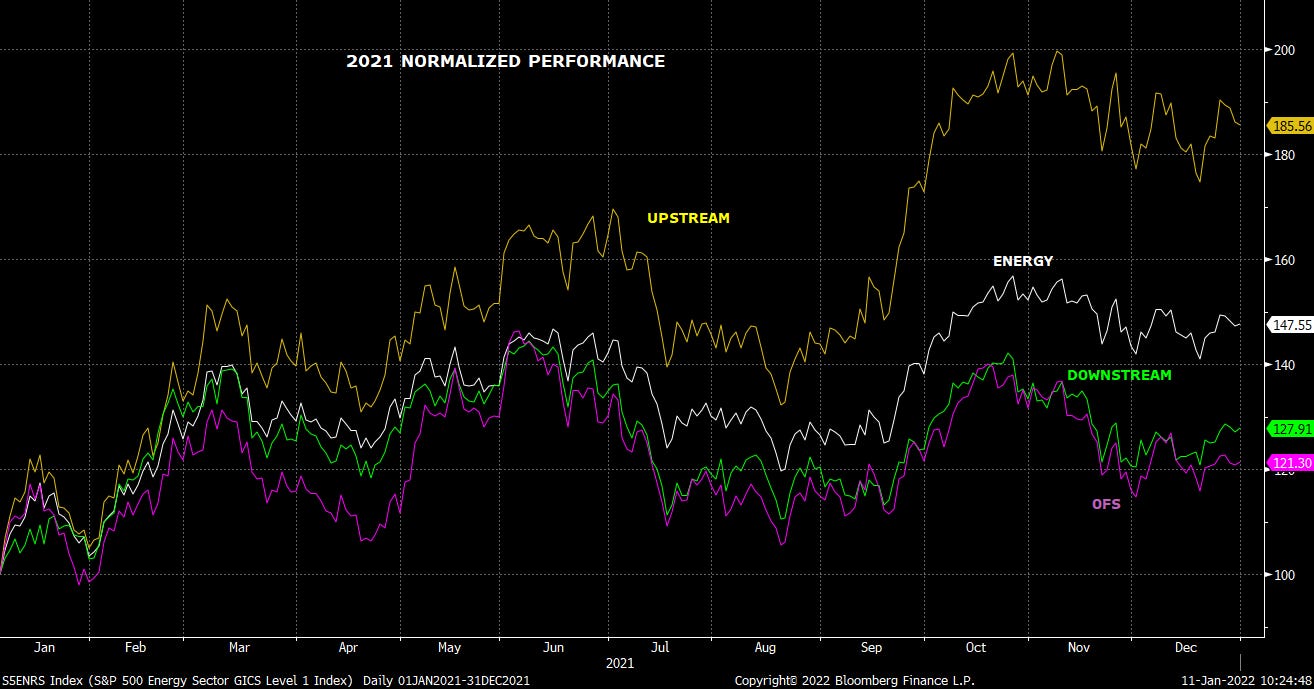

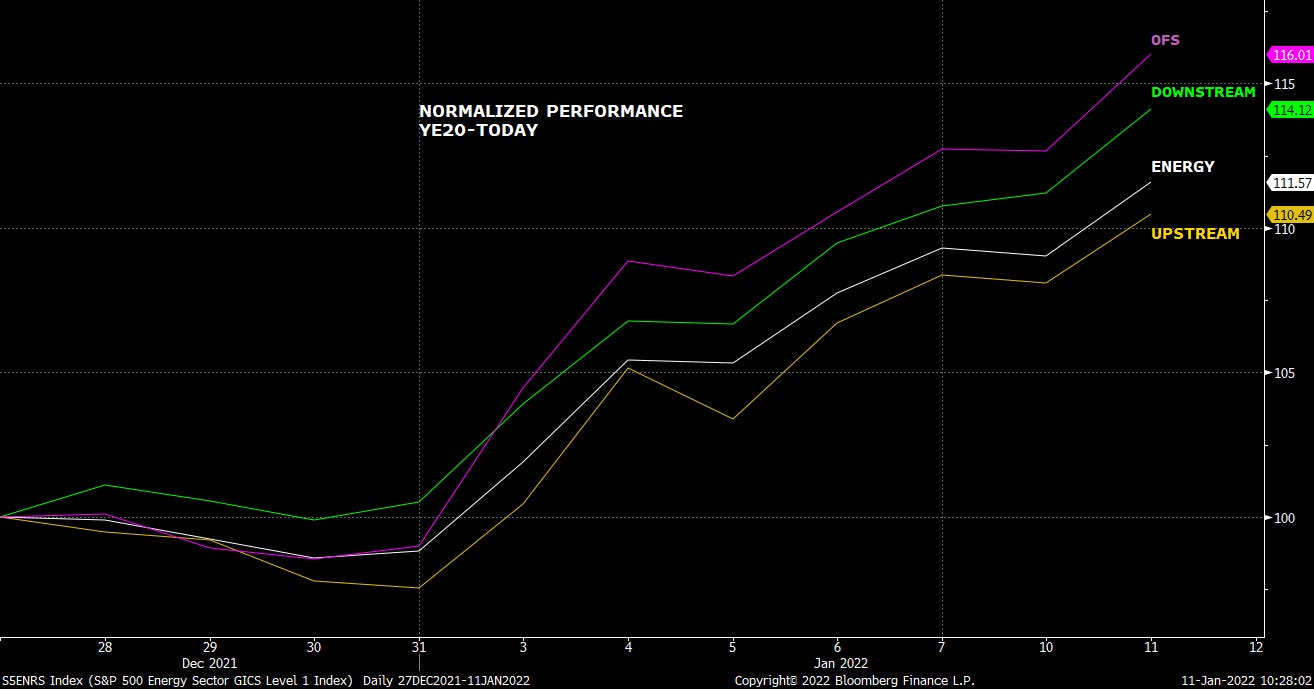

We point to a few reasons behind the discordance. First and foremost, Energy is rented, not owned. So the underperformers of 2021 (OFS & Downstream) ….

Are the winners today. Classic buy the laggards, fundamentals-be-damned approach.

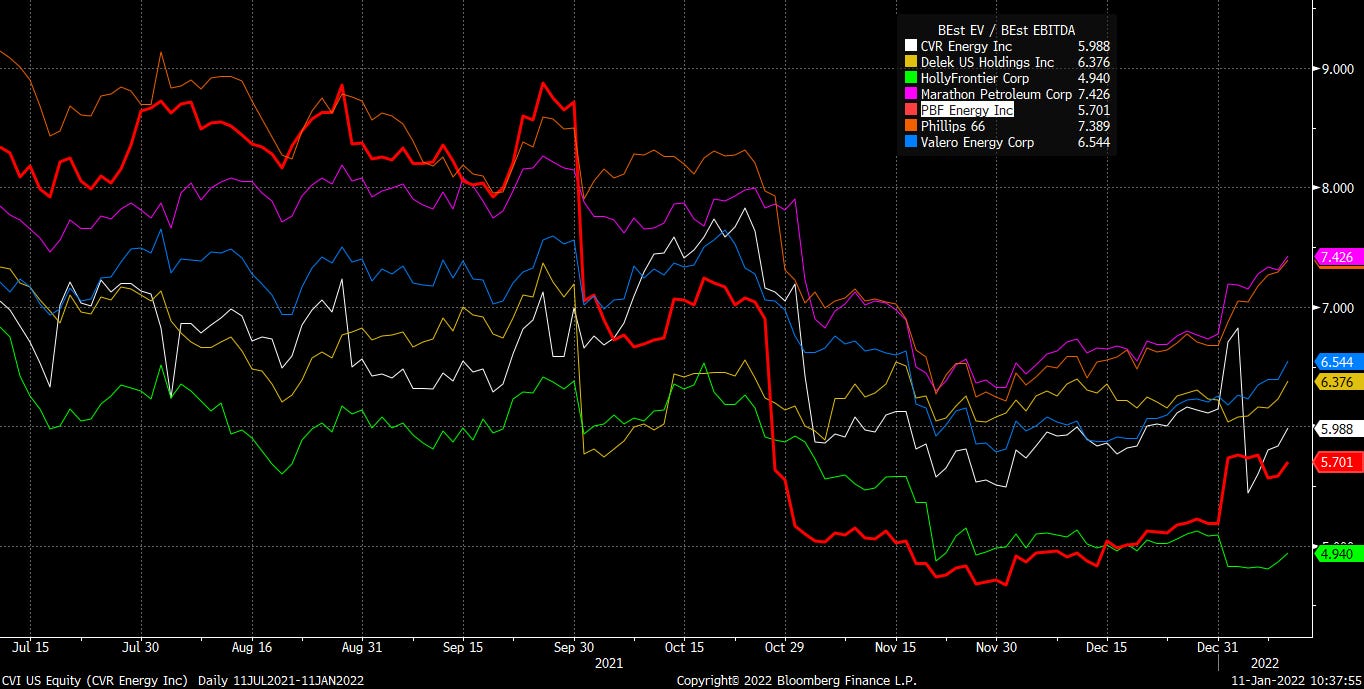

We zero in on the Downstream, the only sector trading at a premium to historical valuation multiples today. Interesting to see every downstream name is trading at a premium to the upstream group.

Interesting because the downstream subsector was the only subsector that made money in energy, and enjoyed positive equity returns, during the shale era up until COVID.

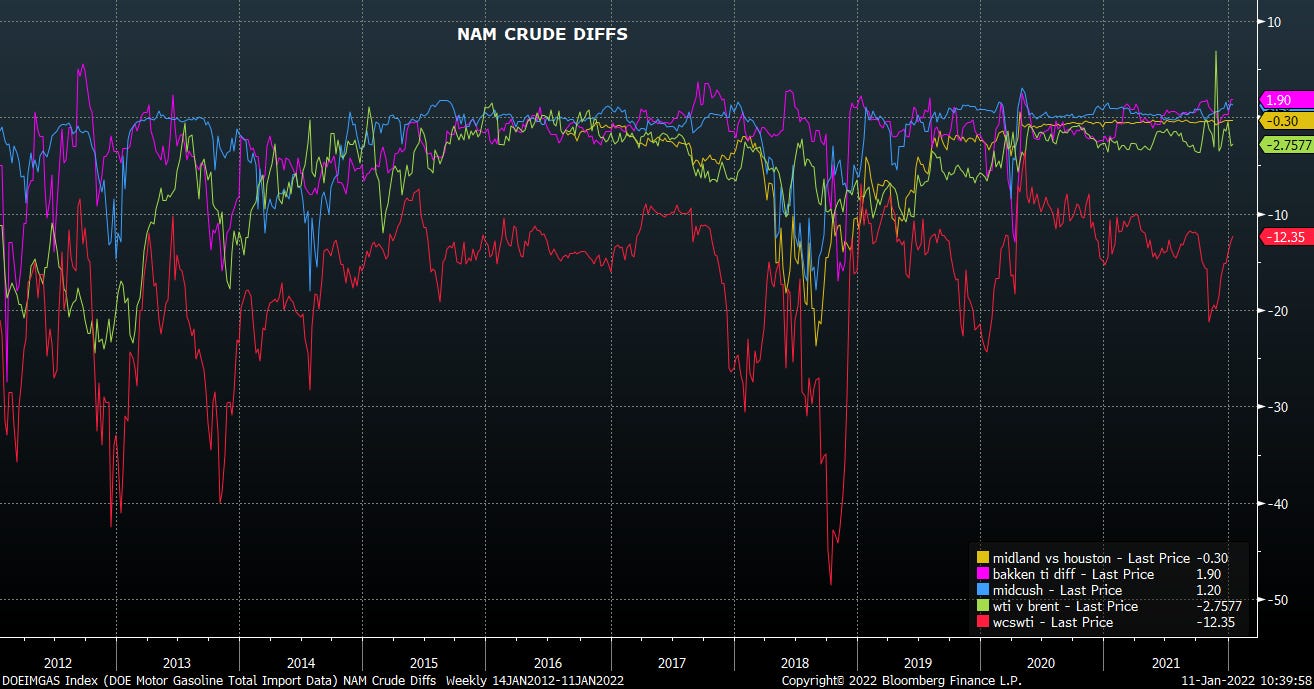

And the reason why? Dirty little secret is there is nothing unique about NAM refining. The sector was the beneficiary of the upstream blowing its brains out on production growth and selling its product at a discount to the refiners in the form of wide crude diffs that went straight to the bottom line. An earnings attribution shows near the entirety of downstream earnings during the pre-COVID shale era were attributable to wide crude differentials.

Now, the US is overpiped, and the upstream companies are taking a decidedly more conservative approach to production growth. Result = diffs effectively gone. Big crude sources even trading at a premium!

So with the primary driver of Downstream earnings gone or even inverted, perhaps there’s another fundamental angle behind the group trading at a premium multiple after suffering a structural impairment to the business.

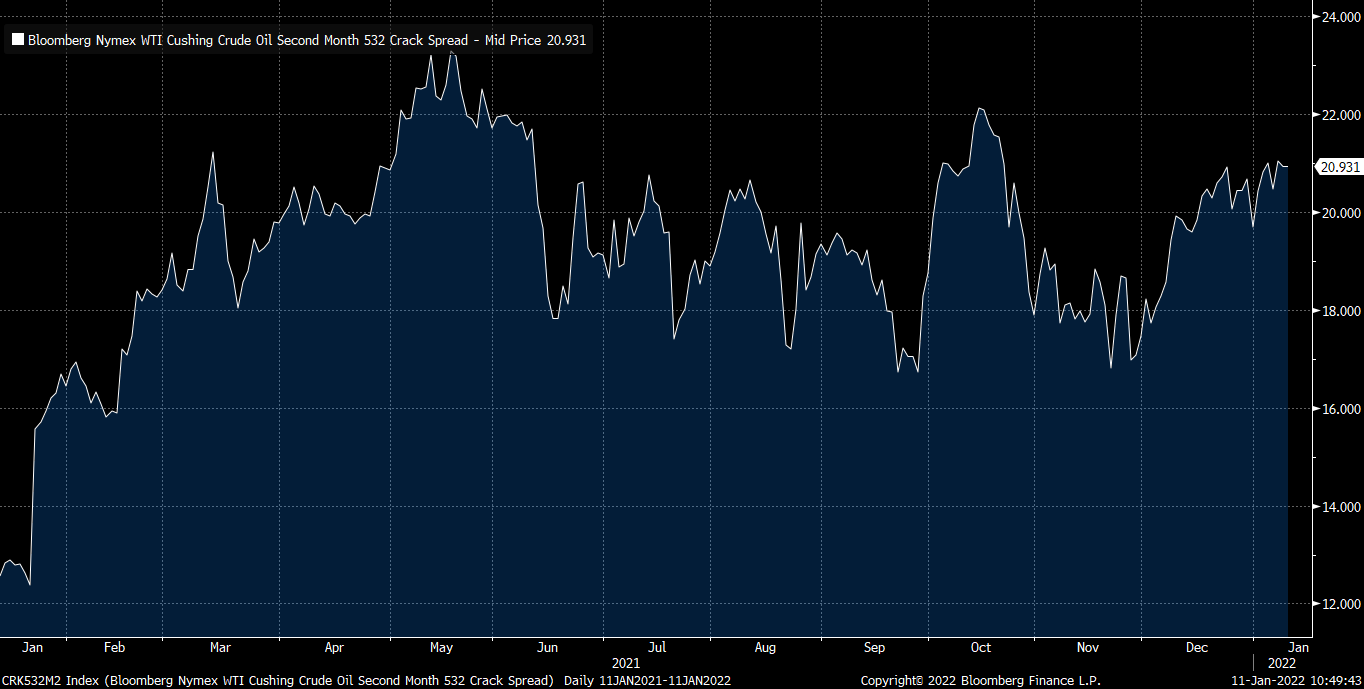

Screen cracks look OK, one could argue. Gasoline crack is meh. Distillate crack is OK at a glance, notwithstanding the fact that it is wintertime.

Thus the generic 532 crack strip looks pretty OK at near $21/bbl, right?

That alone, coupled with the fact that “people are driving and planes are flying” should be enough to sucker sellsiders and buysiders to advocate for the laggard sector. And so they have.

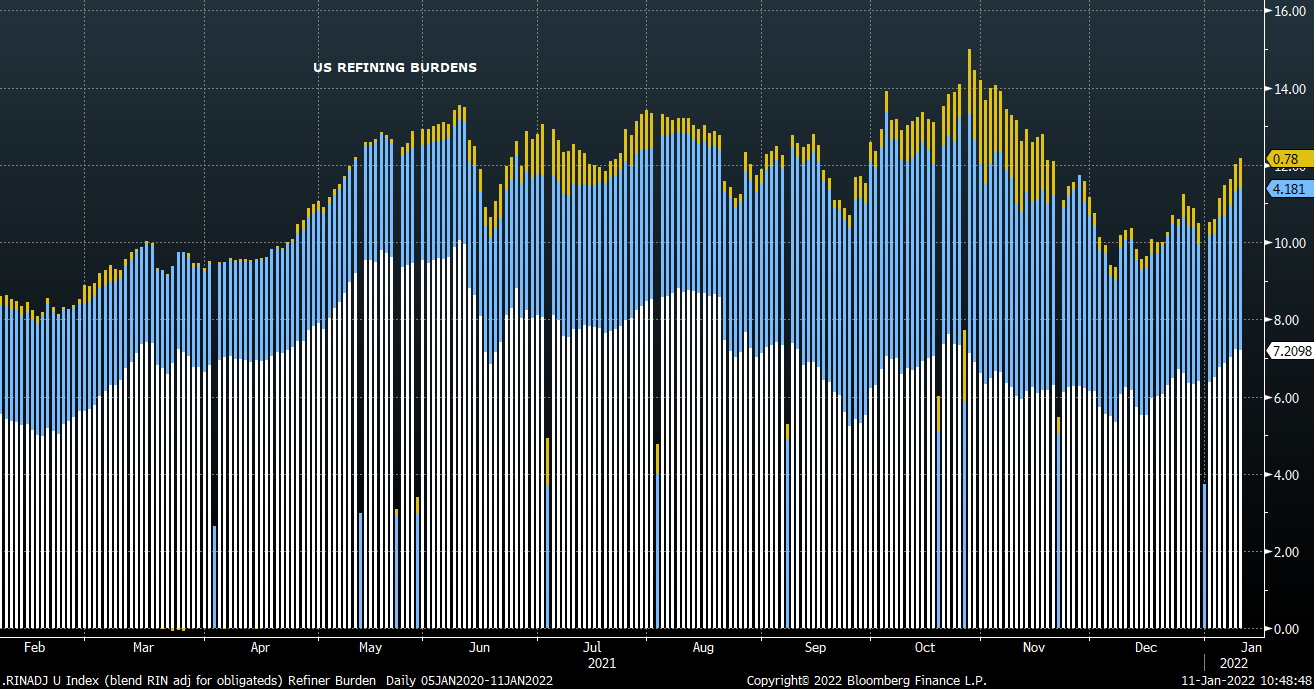

A more nuanced approach dissects the above 532 crack in an effort to discern a clearer picture of the sector’s overall health. First, from the screen cracks, one must remove what we call the “burdens.” These are costs borne by the refiners that are deducts from the screen price and include such costs as RINs, shape of the crude curve, and others. Hot dog, these are about $14/bbl today! That’s quite a deduct from a $21/bbl screen crack.

Netting out the screen crack and the burdens, we see underlying generic 532 crack is sub $9/bbl. For an industry that runs at $5/bbl opex and pays $2-3/bbl transport, this doesn’t look too great.

Which is weird for a sector in massive oversupply that has been forcing capacity closures for two years, in the face of monster new capacity additions. Weird that breakeven is best.

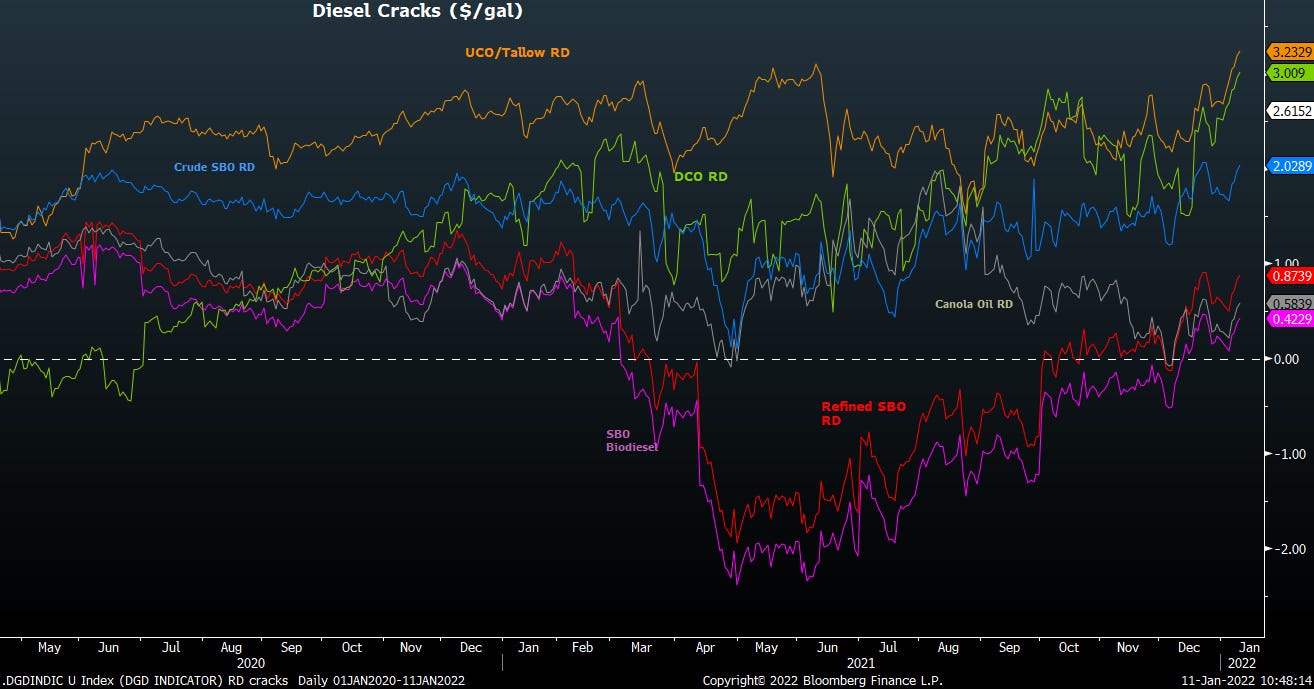

Maybe it’s enthusiasm behind every single downstream operator pivoting from O&G refining into biorefining with new renewable diesel facilities. Of course, with the lone exception of Valero, they’ve all rushed to sanction new renewable diesel facilities that are forced to procure the most expensive, least economic feedstock that’s already in tight supply - soybean oil.

Looking below, maybe this isn’t the reason. Gross margin of $0.50-1.00/gal on a facility that will cost $0.50-1.00/gal to operate probably isn’t the reason for excitement either.

So it’s the laggard trade. That can work, but fundamentals matter over any given time frame stretching beyond a few days.

Generalists trafficking in downstream energy have an excuse for not knowing better. Others who do it exclusively for a living - not so much.

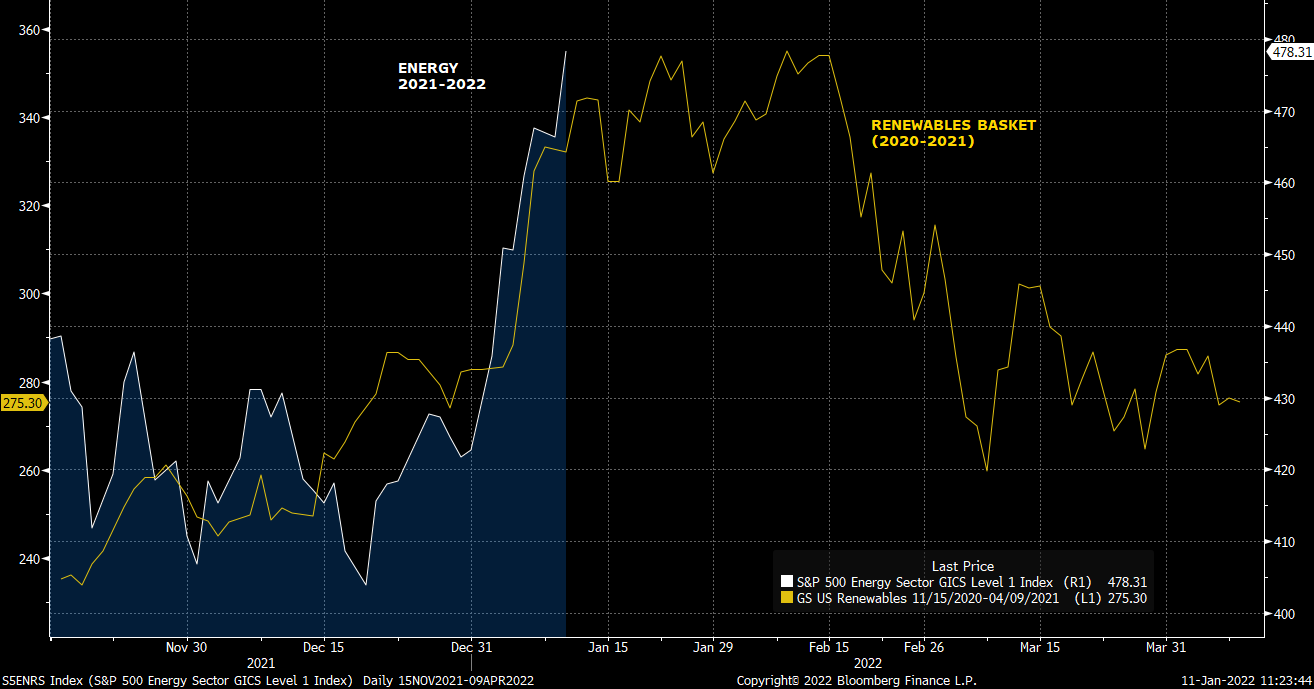

What changed on Jan 1?

We’re working on a hypothesis that 1Q22 is to old Energy what 1Q21 was to Renewable Energy. Big run to start the year on little news, but lots of narrative & (re)positioning. After panic buying was exhausted, the sector stalled and reverted - because it got ahead of itself.

Still way early to make this call again, though buying moves of this magnitude, of this velocity, from this high of a base, will prove to be a challenge to sustain.

A growing risk is that the market is paying for a good year in one month.

Pragmatism

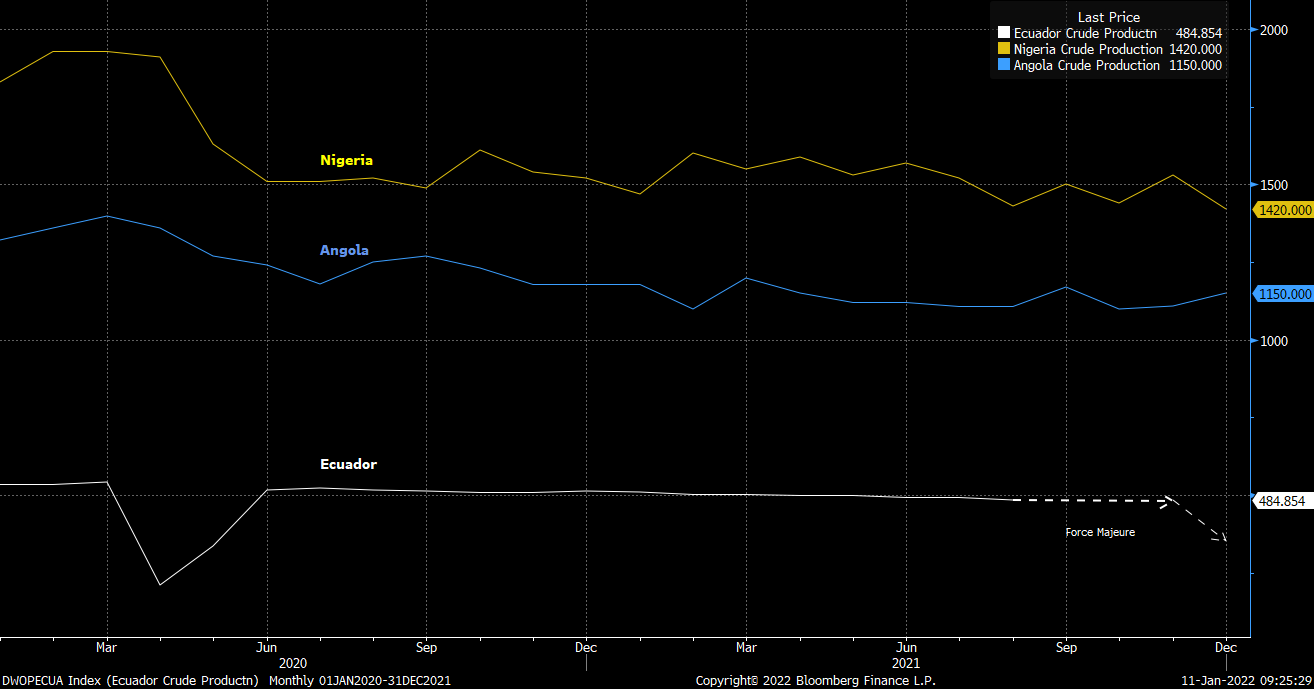

Part of the crude oil narrative in recent months has been some sort of derivation of “dwindling/no spare capacity.” It tends to be anecdotal and speculative and leans on shortfalls in the production behemoths of Ecuador, Angola, and Nigeria as confirming evidence.

Combined production from the three countries at around 3 mmbbld is down a few hundred thousand bbld since beginning of 2021, and took another leg down in December with Ecuador’s force majeure declaration (since remediated).

This overlooks the fact that West African countries continue to struggle to sell existing production and have little incentive to increase production. See West Africa floating storage volumes at multi-year high. Produce more to hit the numbers and store it offshore?

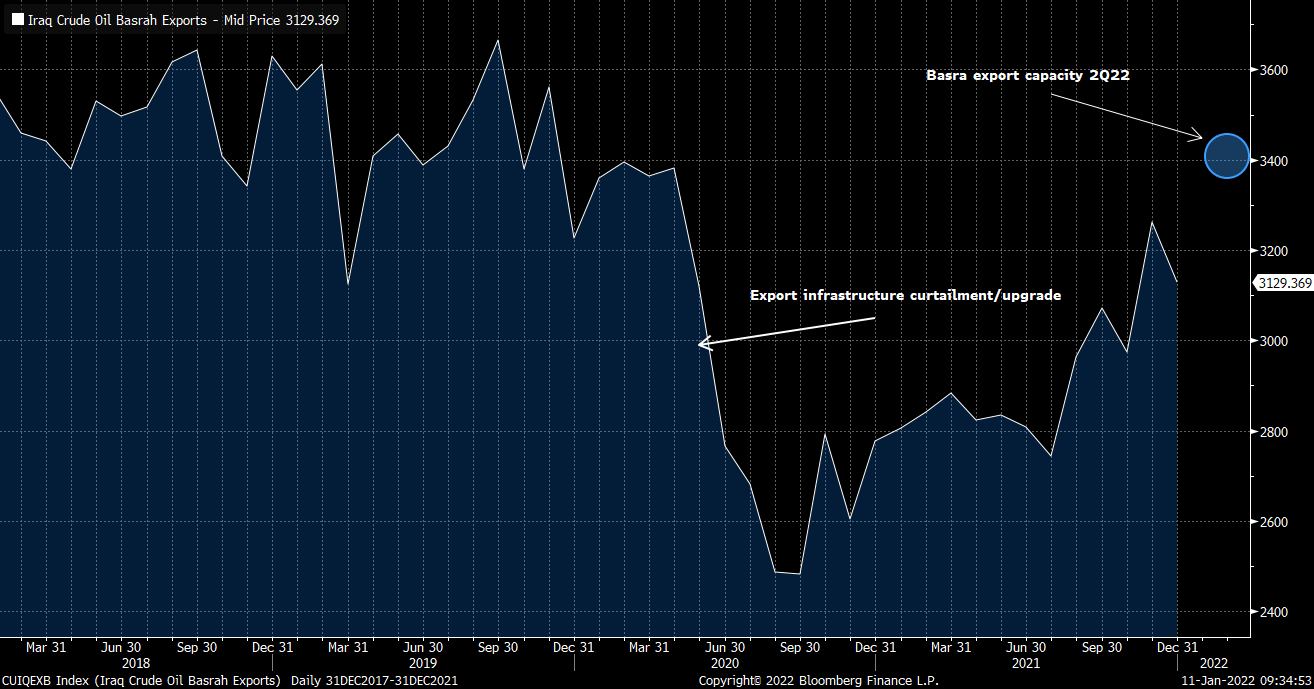

With a news release today, Iraq obviates that purported production decline.

Iraq to boost southern oil export capacity from second quarter - source

Iraq began curtailing exports from the Basra region in mid ‘20 as part of an upgrade/expansion project, now slated online in 2Q22 with an incremental 250 kbd export capacity.

Iraq, notorious for producing above its OPEC quota, will once again have the ability to overproduce its quota.

The narratives are in charge right now. They’re inflated, but in the driver’s seat. Appreciate them, monetize them, but respect what they are. The faster the sector appreciates, the sooner fundamentals take over.

“Price is what you pay; value is what you get”

VR

viscosityredux@gmail.com