Violence inherent in the system

Corporate (Un)hedging

In a presentation today, Pioneer announced that it had closed out the bulk of its 2022 hedges at a cost of $328mm. We are always intrigued when E&Ps unwind hedges AFTER prices have rallied.

Case Study #1 EQT. EQT suffered (relatively) most of 2021 after layering on hedges to protect economics of acquisitions. Then nat gas rallied and EQT lagged its peers. It was a pernicious overhang - at one point EQT had mark to market losses of over $5B and was the subject of margin call speculation.

By early 4Q21, with the 12-month strip having moved from $3/mmbtu to $5/mmbtu (with particularly painful exposure in 4Q21/1Q22 months), EQT capitulated. They unwound a portion of 4Q21 and 1Q22 hedges AND bought upside exposure to the same time frame.

The 12-month strip is down 19% since then.

Case Study #2. Of course, the most famous incident of hedge lifting was that of Continental Resources in 4Q14 in what turned out to be the 1st, not 9th inning of a OPEC-driven crude crash.

U.S. oil CEO Hamm goes out on a limb, scraps hedges

Crude prices fell 36% to year-end ‘14, and 62% to year-end ‘15. It’s not really a hedge if it goes away at management’s discretion.

At the industry level, energy is approaching a rational cooling off point. We don’t expect it to break through resistance levels set at the most recent pre-COVID highs. The sector is overbought

And we do expect that increasing supplies and lower demand will pressure prices.

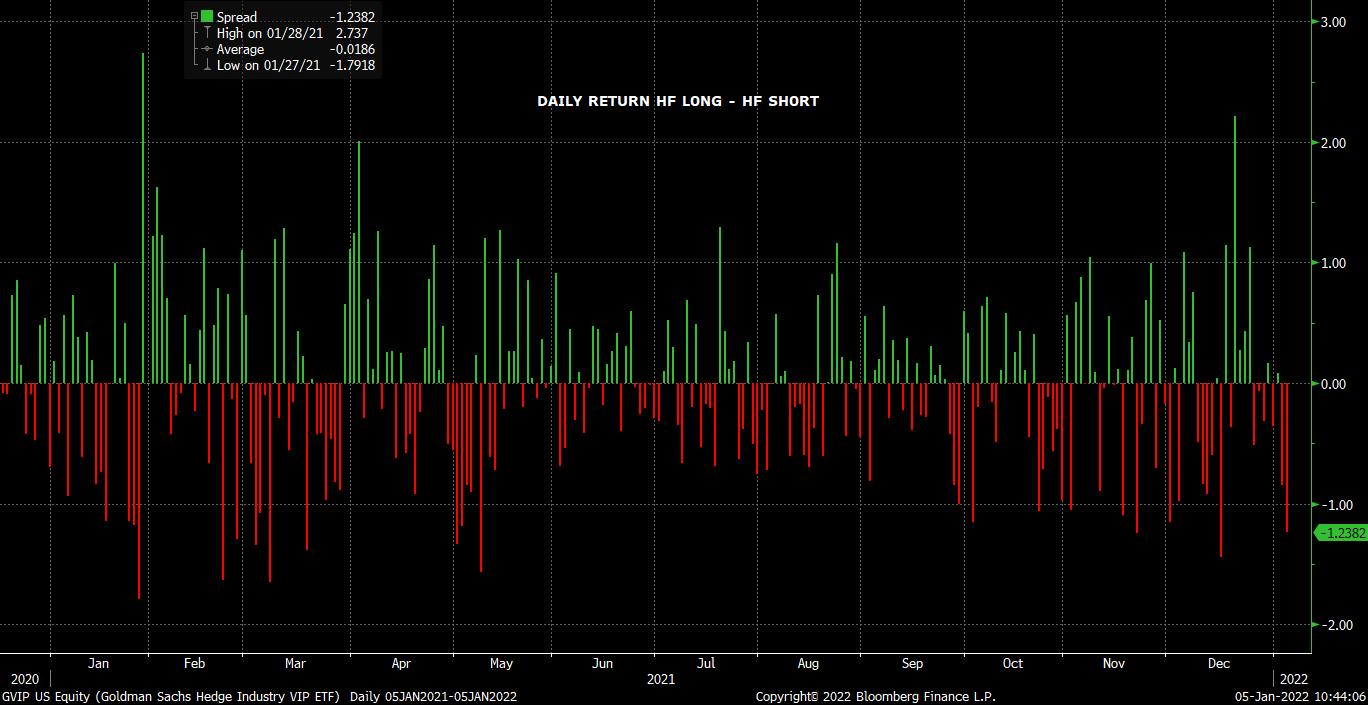

Pain is rampant. Hedge funds are “derisking.” Meaning they’re wrong. Again. So they’re selling longs and covering shorts. Again. Volumes are high and hedge funds have sold more tech in the last 3 days than they have ever before. They’re now more underweight tech than they have ever been.

Check out the spread between HF hotels (white) and HF shorts (yellow)

Racking up a decent string of back to back to back days of underperformance.

Value vs Growth - energy has undoubtedly been a beneficiary. Not interested in extrapolating this trend for the coming days though.

A little professional insight: Energy is not a contrarian trade. Quite the contrary.

According to GS, exposure to funds are the most underweight Tech and most overweight Cyclicals that they’ve been in over 5 years.

Where do you think 10Y can top out before we beg for the Powell put again?

What happens after everybody goes from one side of the boat to the other in the blink of an eye?

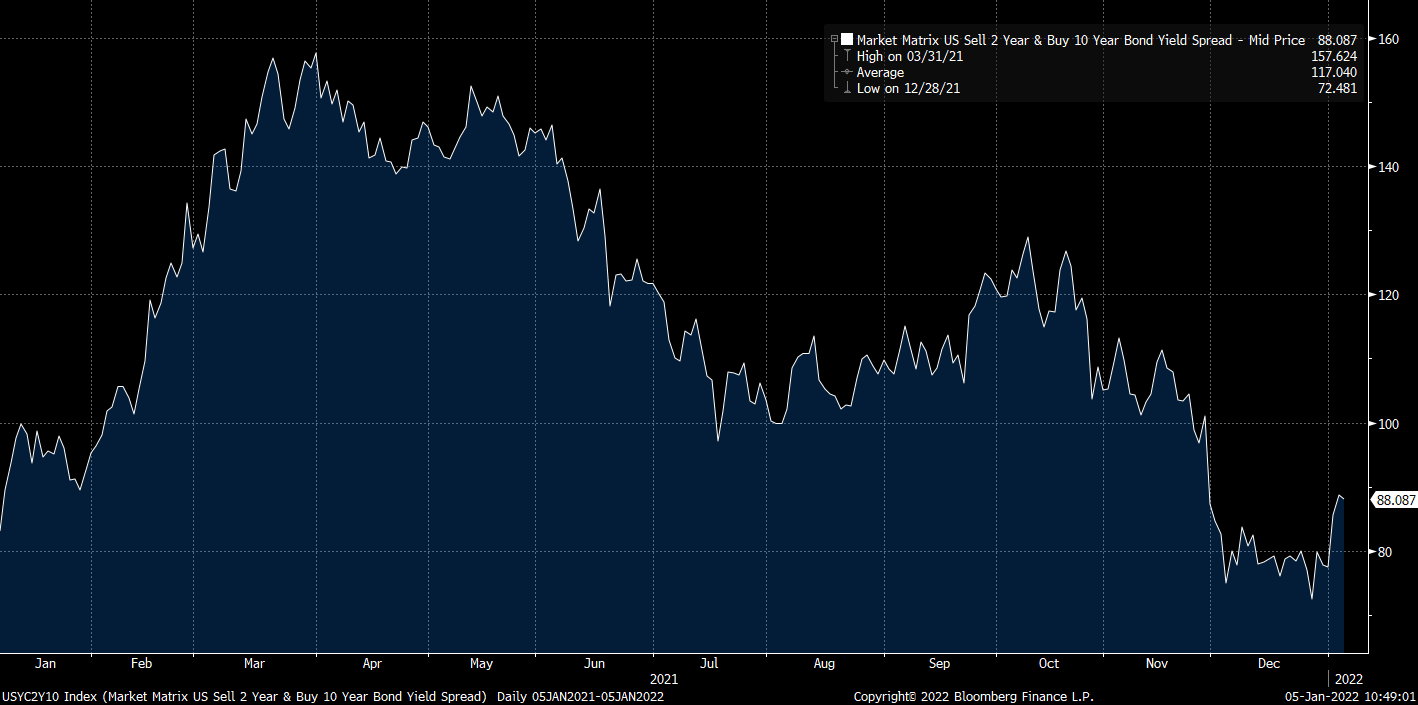

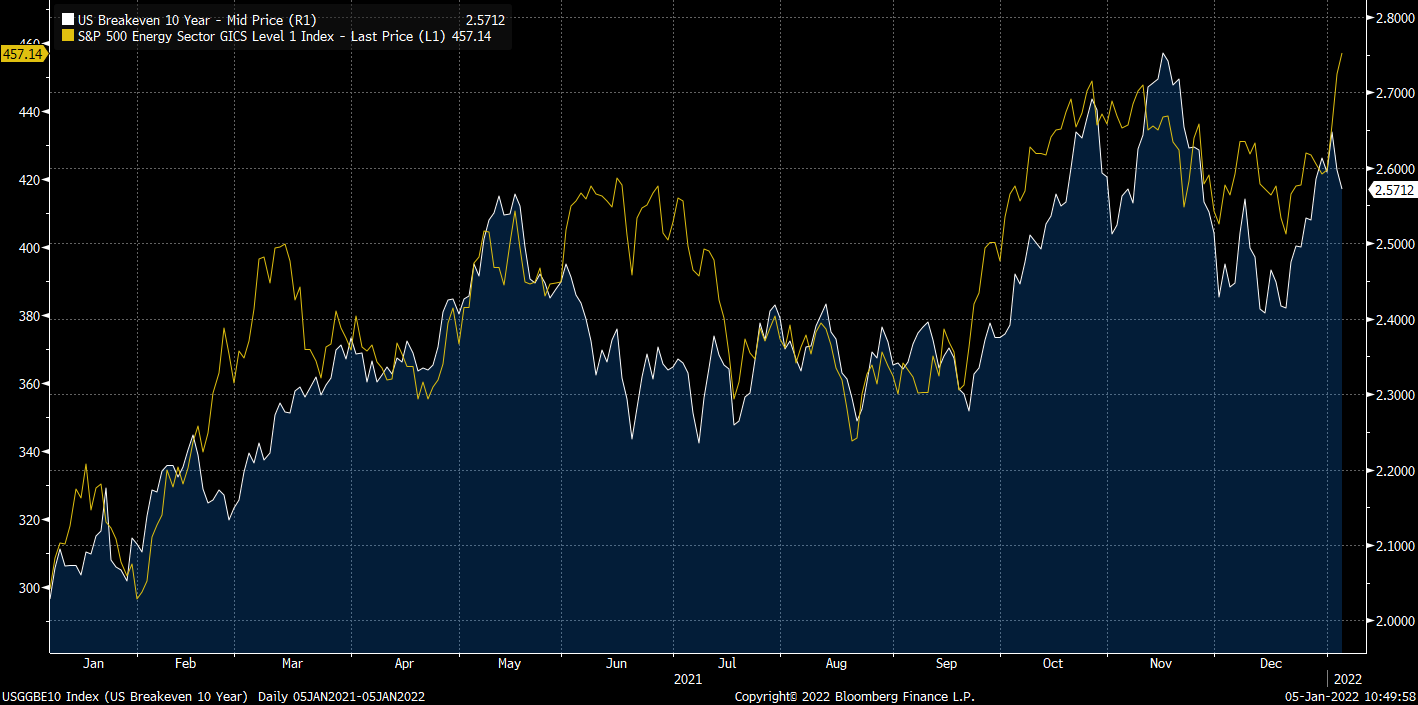

A few charts that suggest this move was too much too fast and may be inflecting:

2s-10s curve

10Y Breakevens

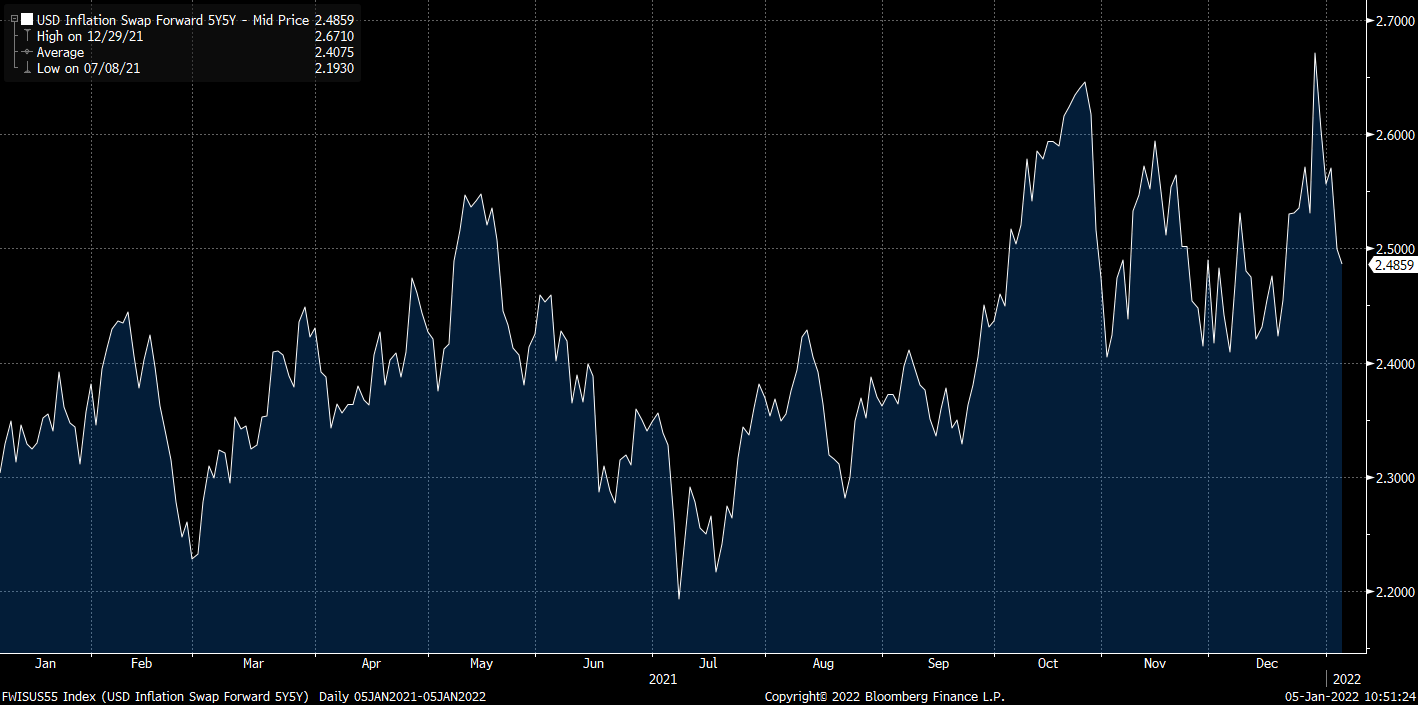

5y5y inflation swaps

Positioning/Trades

New pairs trades in the cyclicals space (long - short):

HES-OXY

LNG-EPD

CTRA-EQT

DAR-MPC

VLO-PSX

DBA-XOP

In addition to the following positions from 1/4:

SHW-LYB

Short DVN

- VR

viscoscityredux@gmail.com