The Trade You're Not Allowed to Disbelieve

The Trade You're Not Allowed to Disbelieve

Everyone is a contrarian

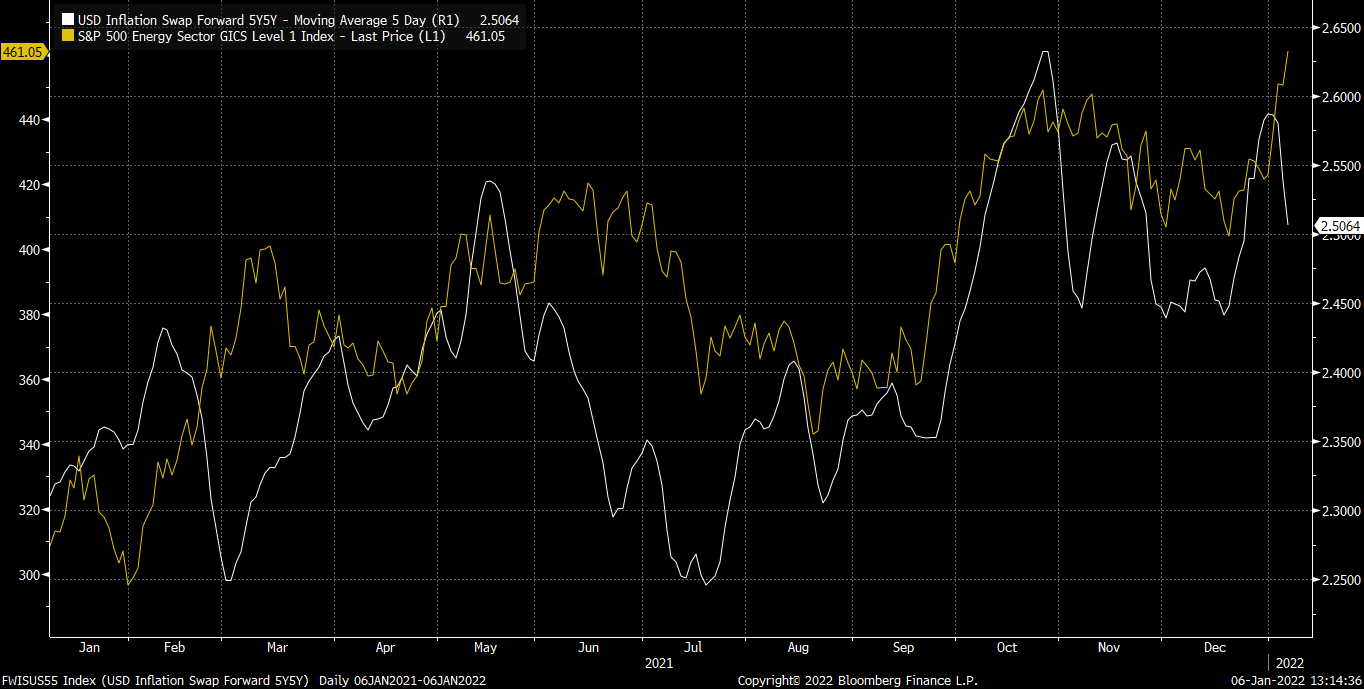

Do not forget: funds are the most underweight Tech and most overweight Cyclicals they’ve been in over 5 years.

Everyone is in the trade no one is in. Everyone is a contrarian. No one may disbelieve the energy bull thesis.

There is no energy crisis. There never was an energy crisis - at least this decade.

Well to be fair, there have been crises of oversupply multiple times in the last decade. And there was, for a brief spell, a global energy shortage in 2007. But nothing since then.

There is a regional acute shortage of certain types of energy for fleeting periods, but there is adequate energy globally. This is not “just the beginning of another supercycle.”

That doesn’t mean you can’t trade it like one, however.

Everything will break. It always breaks. Energy is a cyclical sector. It runs in cycles. This is a cycle, not a supercycle. Today we briefly look at what got us here and what we are watching for the first break.

The catalyst was rates meeting positioning. By late ‘21, Growth had demolished Value and there was no blood left to squeeze from the stone that is the long Value short Growth trade.

The Fed’s barrage of warnings of taper and pending rate hikes finally got the market’s attention. As rates rose, long duration assets, particularly unprofitable ones, got sold hard.

Rates rose and Energy duly followed.

Then, things got funky. Narrative was shaped to rationalize price action. Supply disruptions. Inflation surprises. Demand surge.

It happens.

So that’s where we are today. Everyone is in cyclical sectors, especially energy. There’s a global shortage of hydrocarbons. There is no spare capacity. There is a tsunami of imminent consequences stemming from years of underinvestment (party game idea: take a drink anytime you find someone using the word “underinvestment” on Twitter). There is chronic, not transitory inflation.

The narrative, in this author’s opinion, is exaggerated. But cyclical sectors need a supportive narrative to work - so use it. Simple narratives always work best, especially when they cannot be falsified.

This is typical of a late stage business cycle dynamic and that’s OK. We still have several months of a macro backdrop that will at the very least fail to disprove the prevailing narrative. Growth will stay elevated, inflation will do the same. Then we start lapping the '21 bounce around midyear ‘22, but we’ll worry about that later. For the time being, Energy is (still) the no brainer trade they say.

Crude price follows global inventory trends. And although every bank and forecasting agency has crude building in ‘22 thanks to OPEC unwinding its cuts, it will take a while for the data to materialize and dispel notions of a shortage. Energy still works.

But there is a corner of the energy market that will break first. One could reasonably contend it’s already started. Natural gas.

I’m darn certain there’s no shortage of natural gas, especially in the United States.

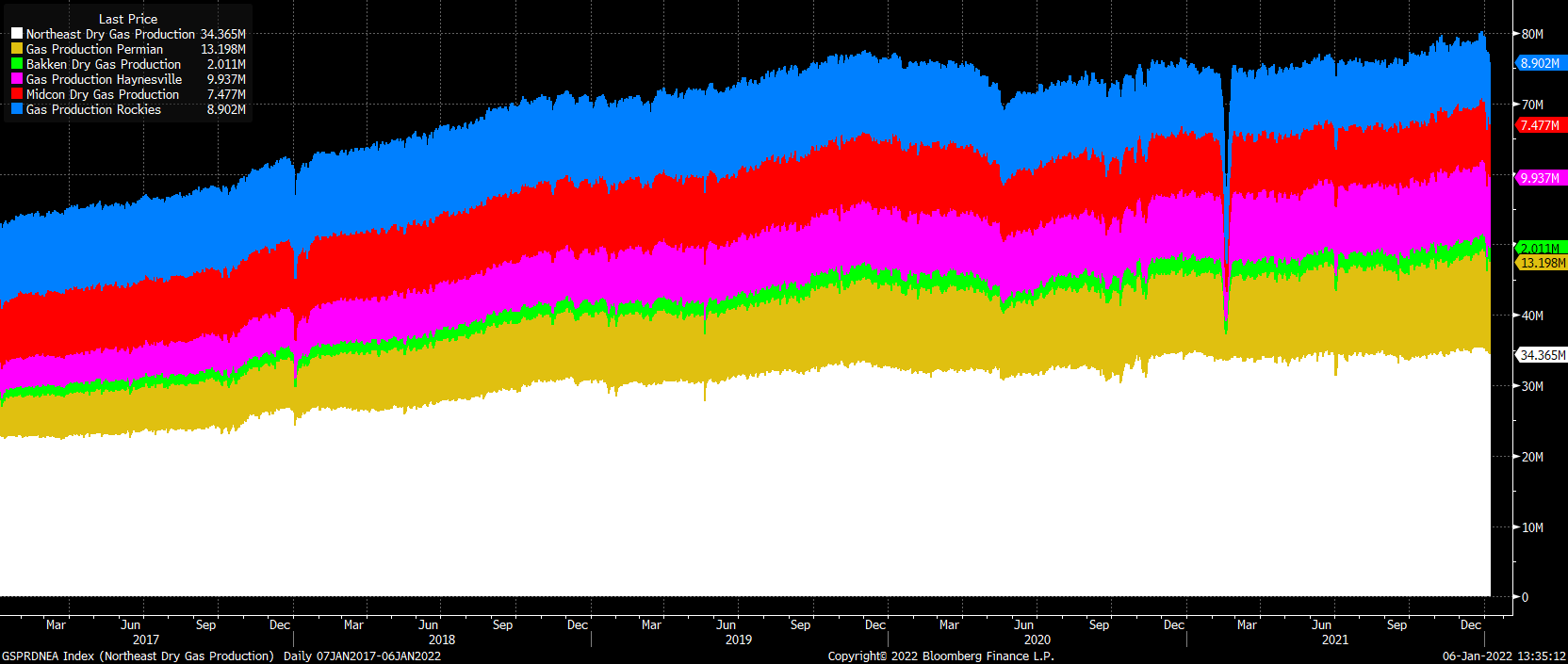

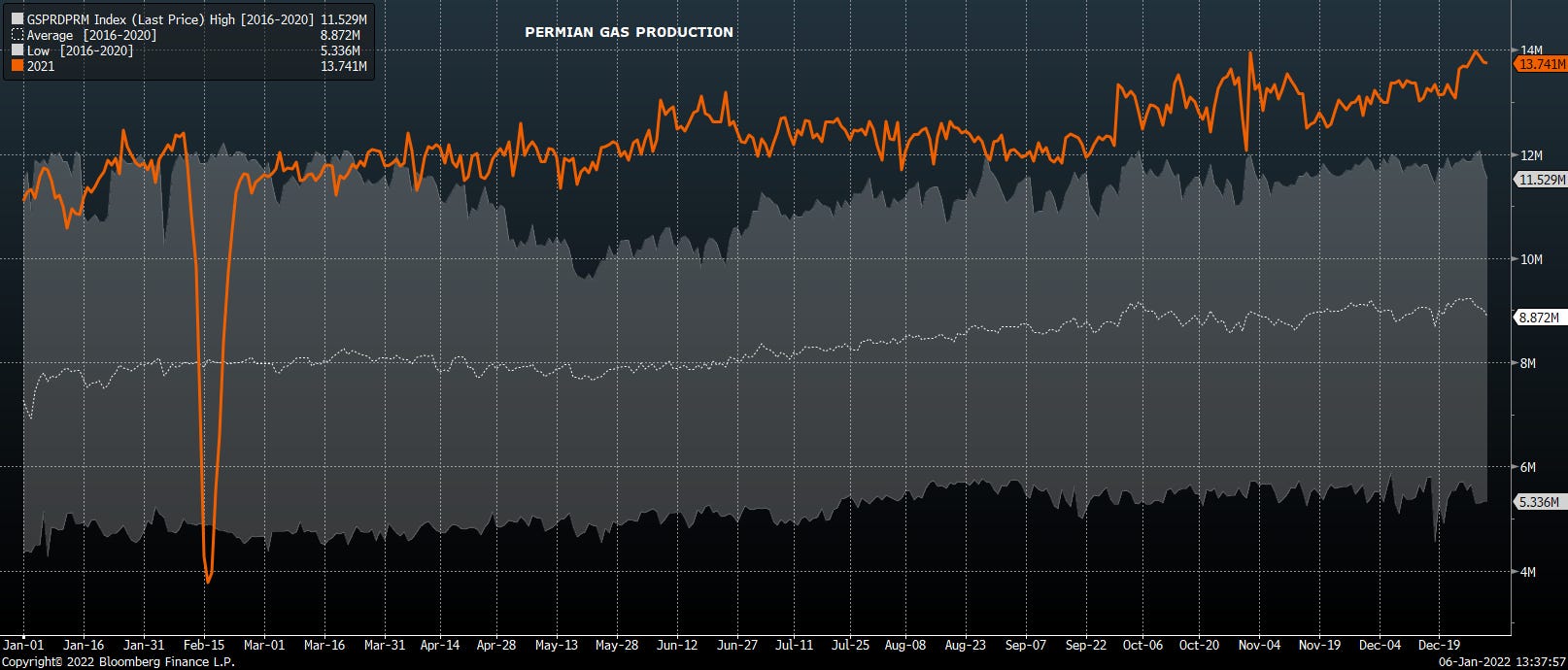

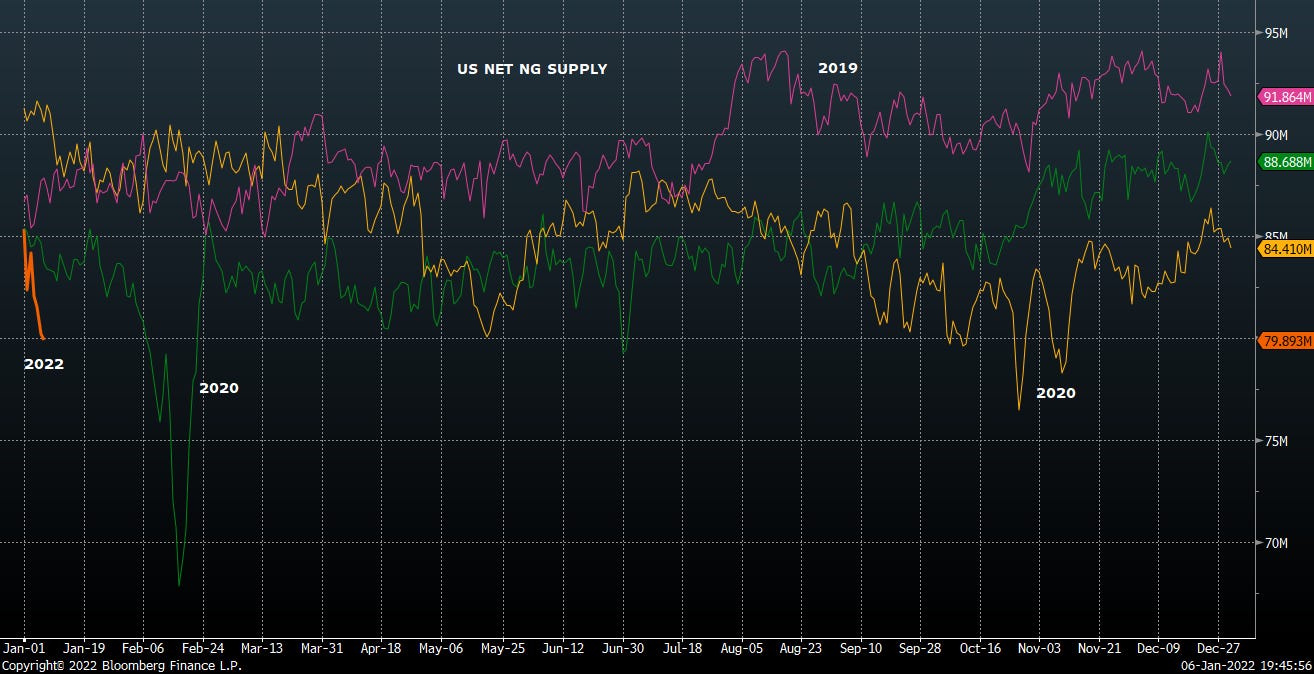

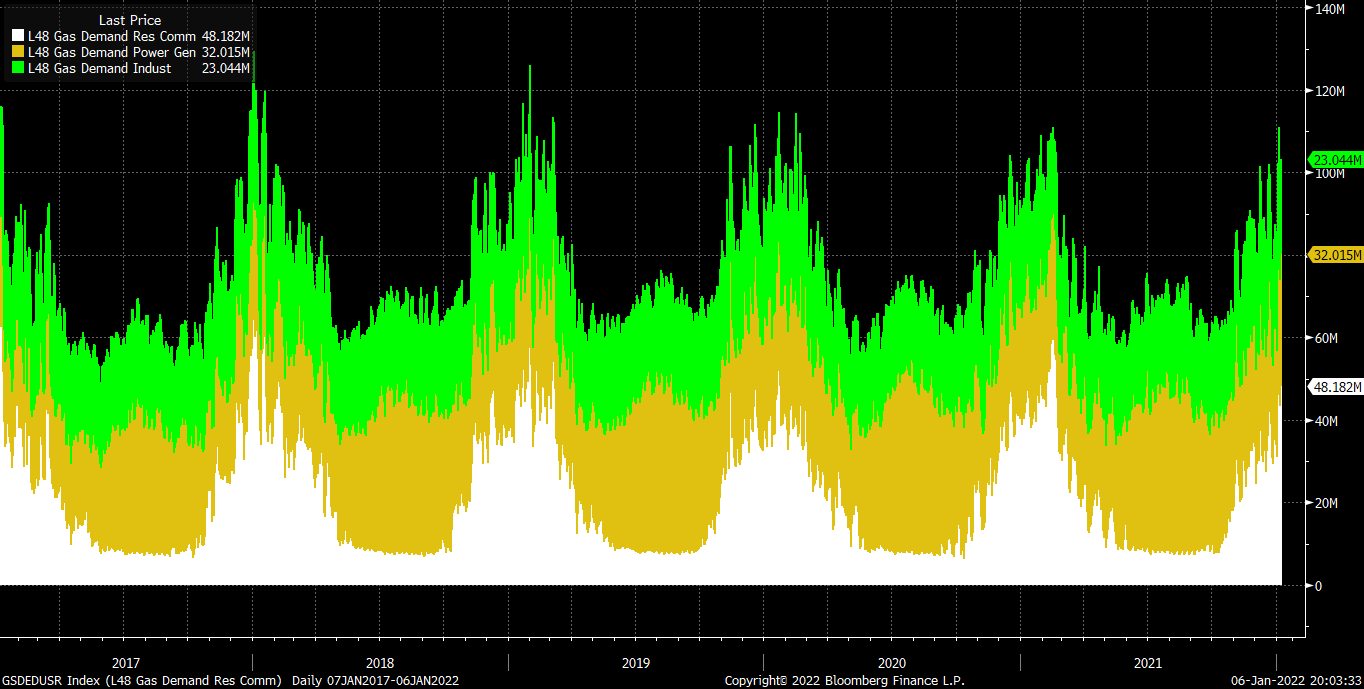

See below production for some US largest producing regions.

Northeast gas production vs 5 yr range

Permian gas production vs 5 yr range

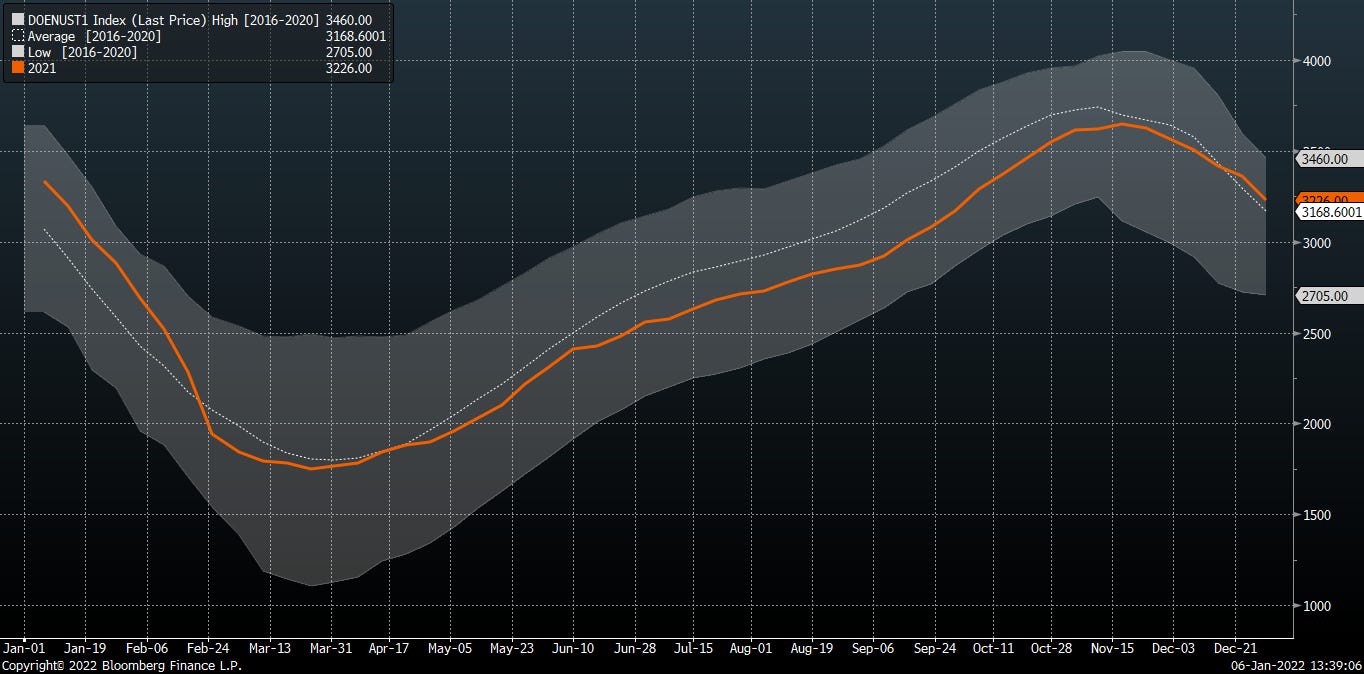

US natural gas storage seasonal - looking fine

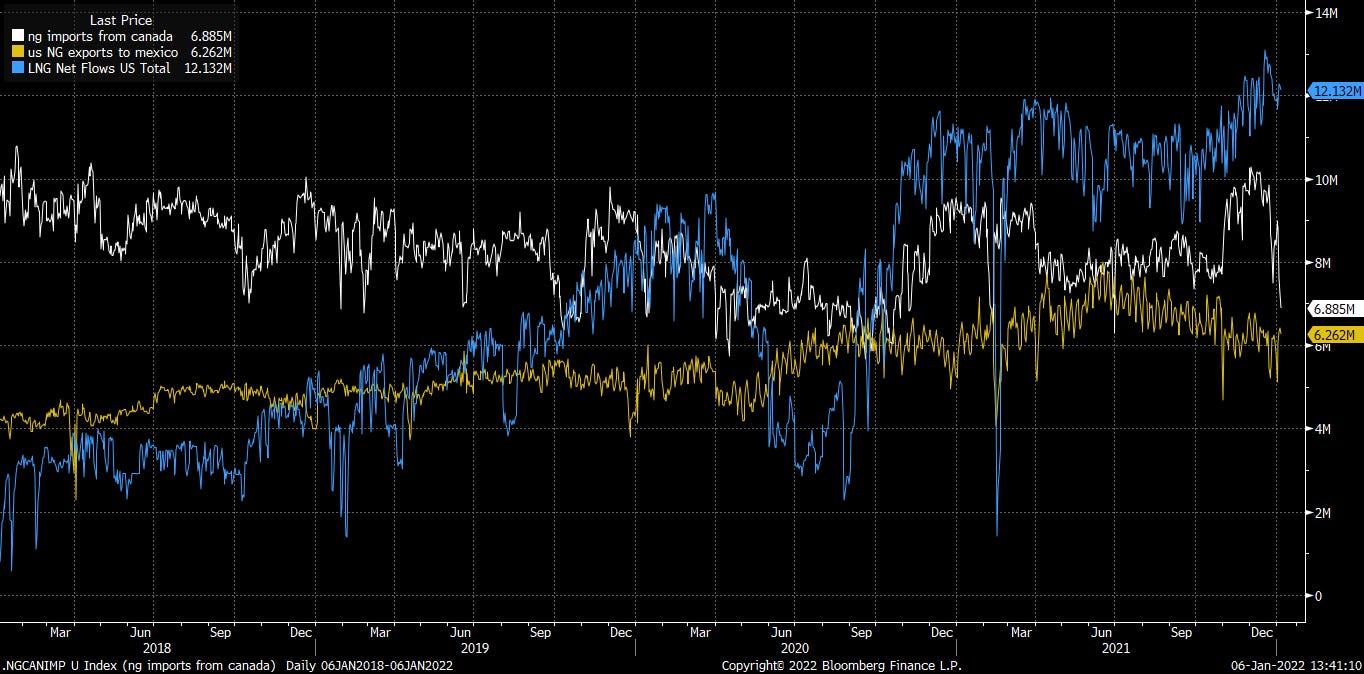

Trends in nat gas import/export flows. Imports from Canada steady ~8 bcfd. Exports to Mexico 6-7 bcfd. LNG exports out of US maxed out ~12 bcfd.

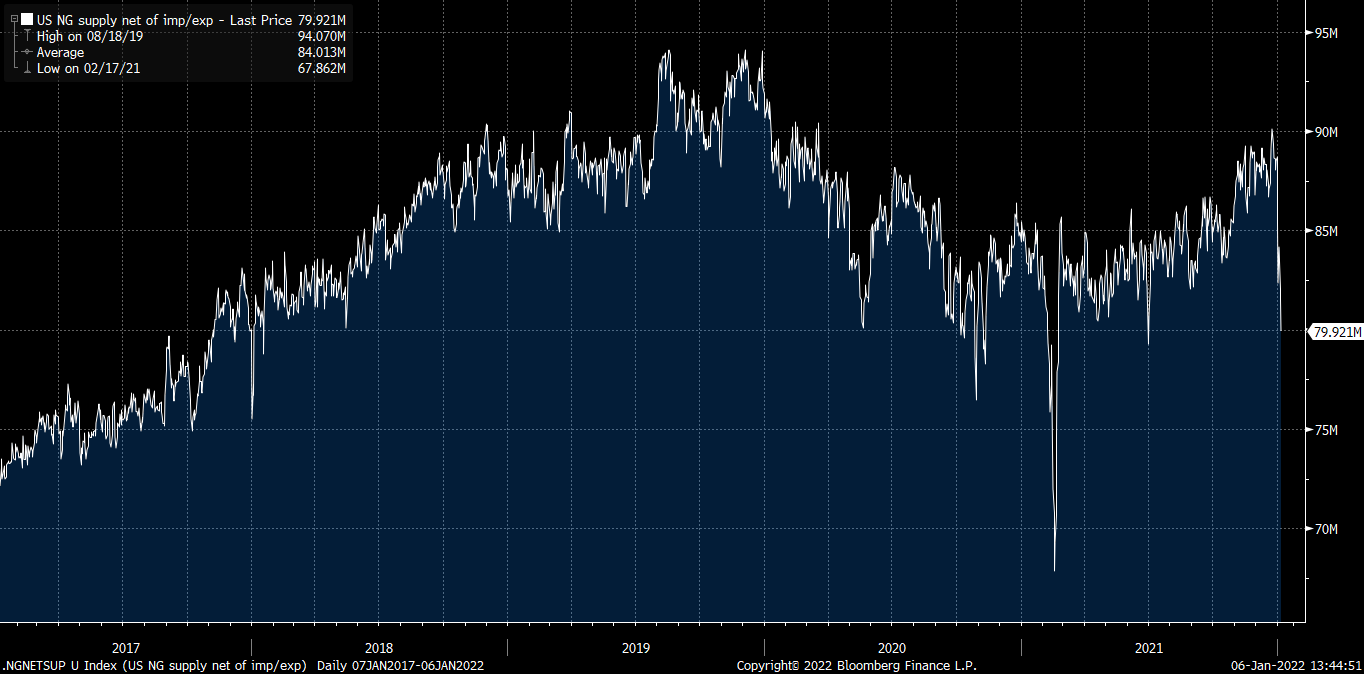

Notwithstanding this week’s weather-related supply drop, total US supply net of imports/exports is making its way back to prior highs.

So the overall supply/demand picture doesn’t look terribly tight in the US.

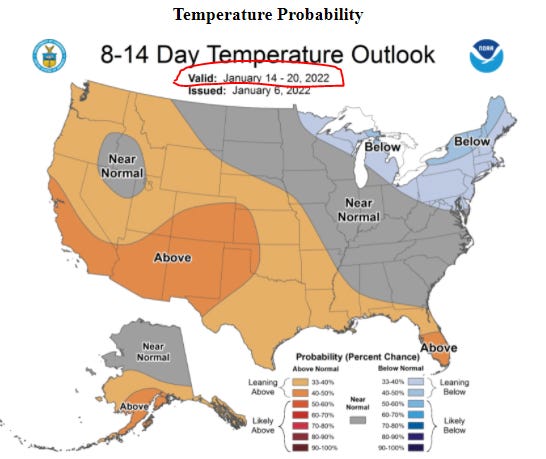

Unless the US gets another storm rivaling 2020’s Uri in the next month or two, the comps are going to start looking pretty bad in a few weeks.

Uri part II is not in the cards at least through third week of January.

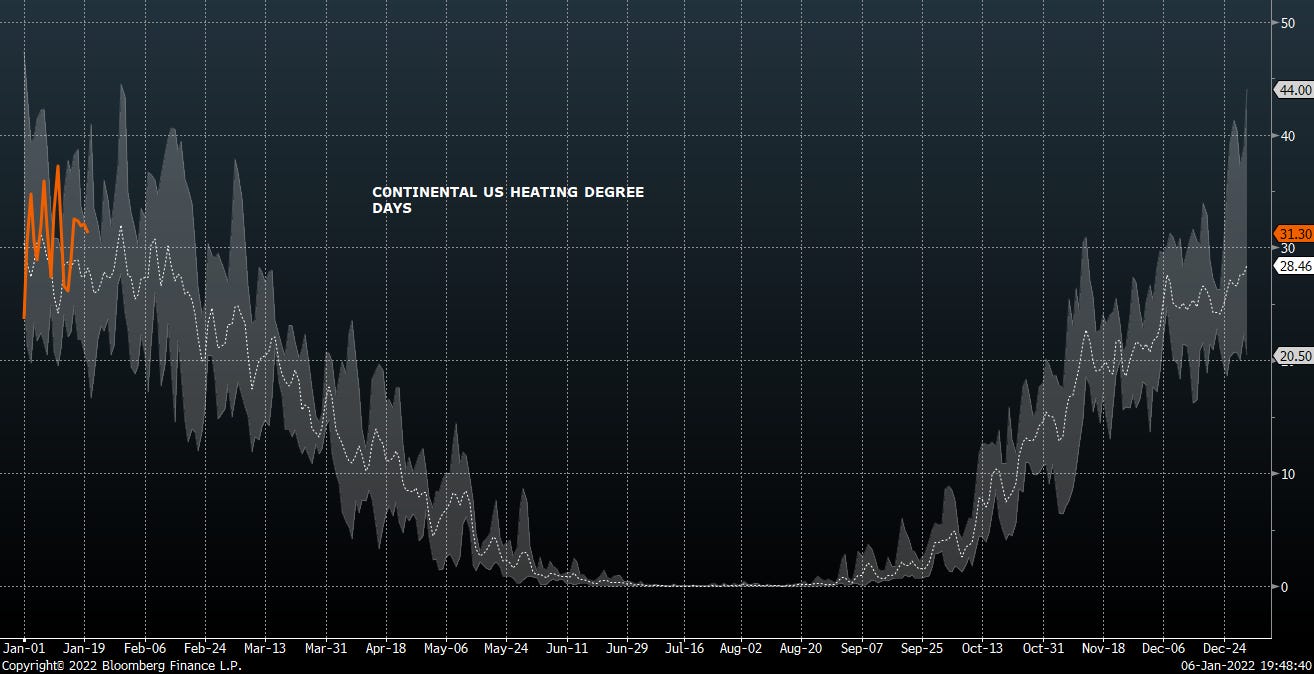

The winter calendar is thus getting really short really quick. Heating degree days seasonally roll over by mid February.

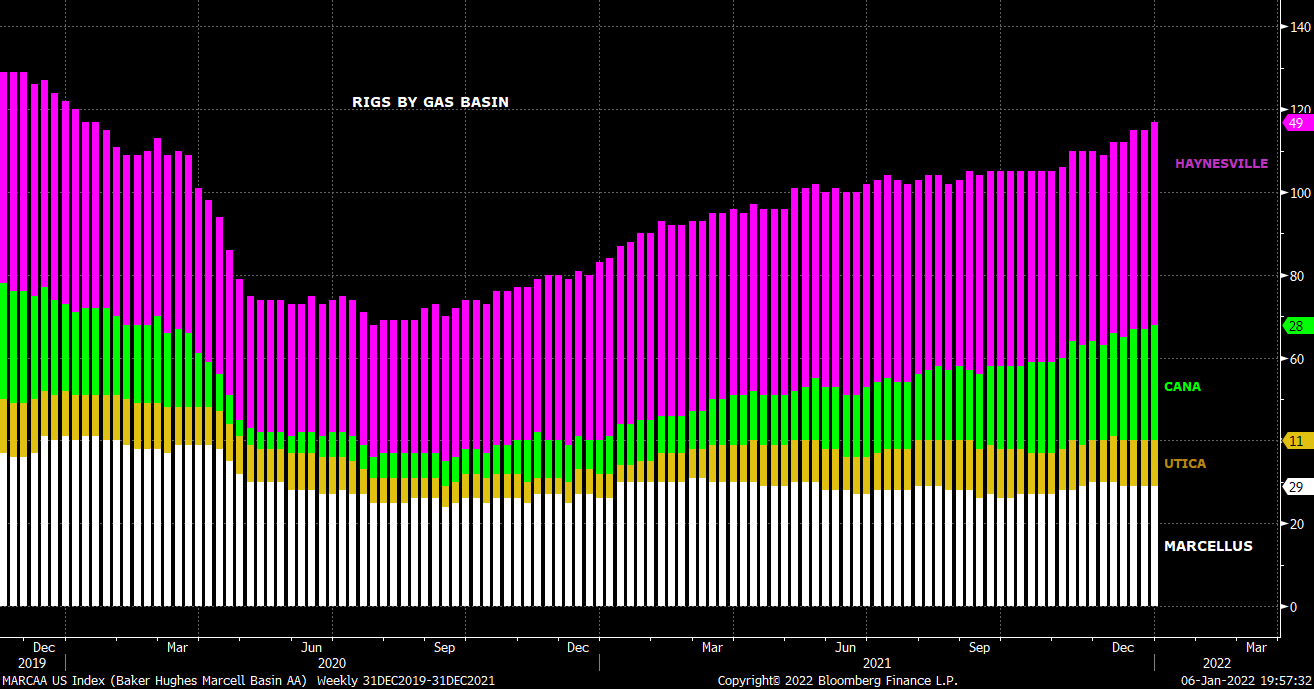

Rig count in the big gas basins above the pre-COVID level; trending up and to the right.

Net supply up and growing. Demand - fine, but not breaking any records.

Well within the seasonal range.

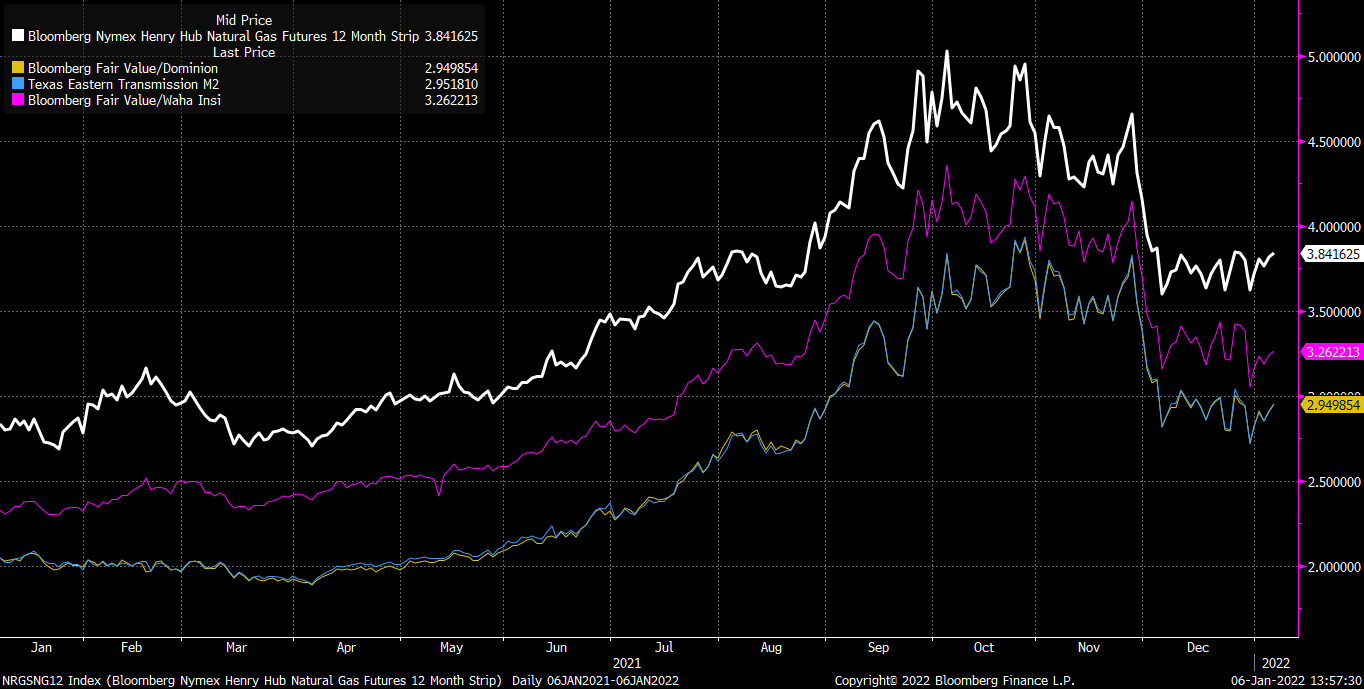

So we’re looking for the curve to come down as winter fades, resulting in negative revisions.

That’s before we consider the effect of basis differentials.

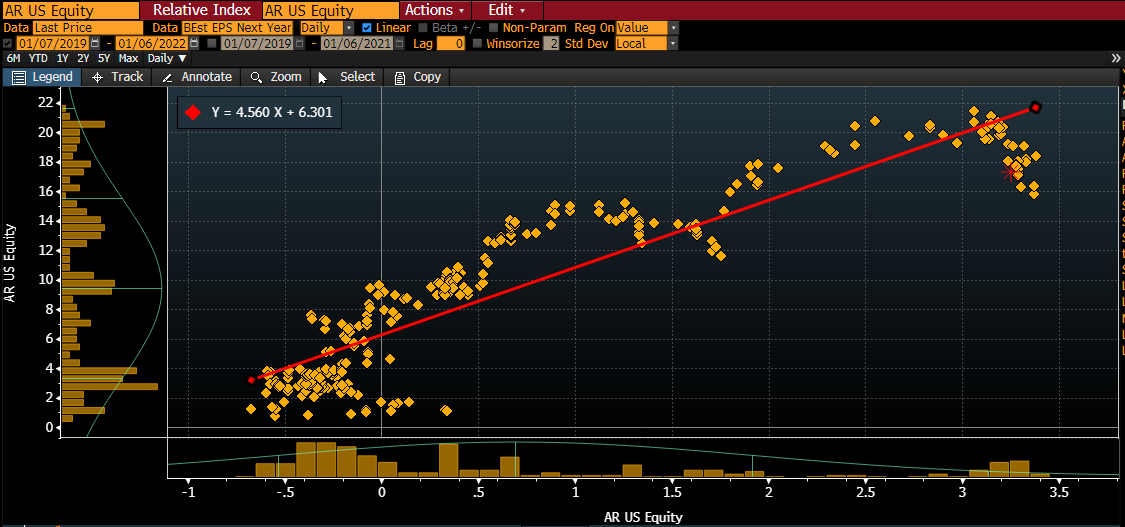

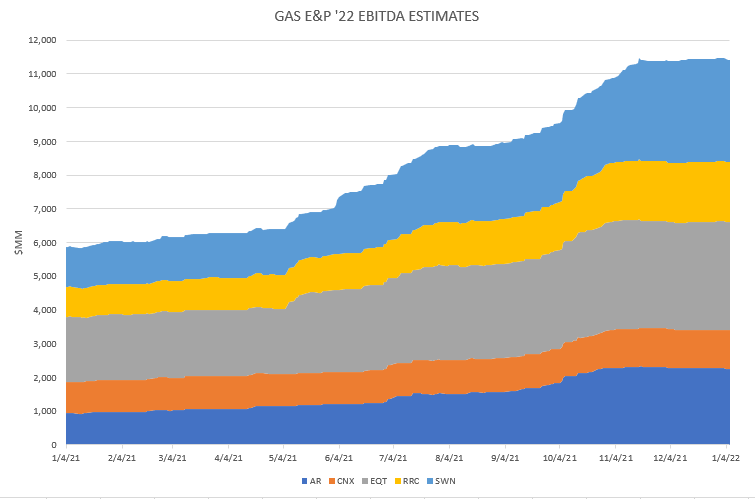

A tenet of our energy investing process is stocks follow numbers, even for the nat gas equities. Antero (AR) here

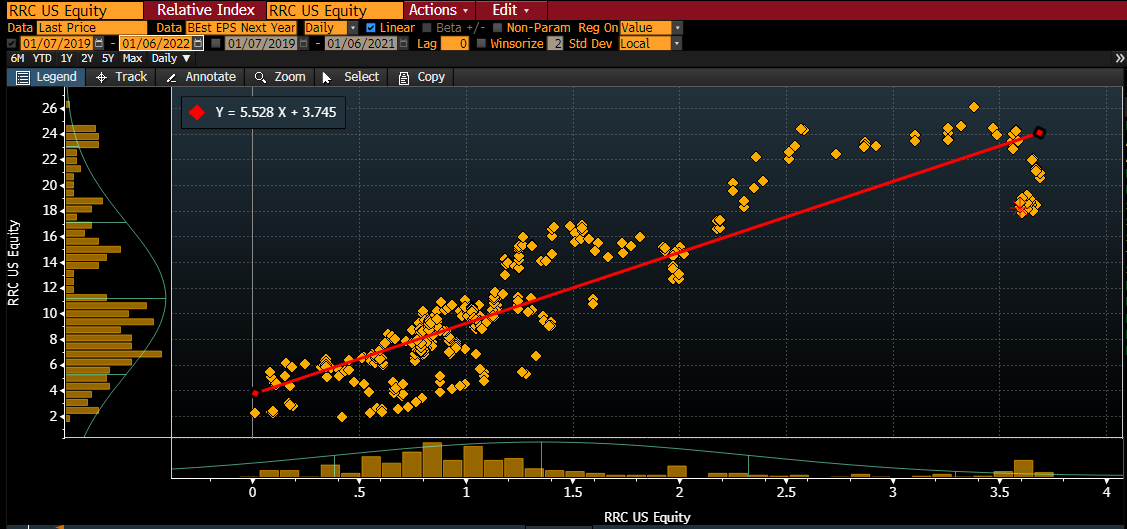

Range Resources (RRC) here.

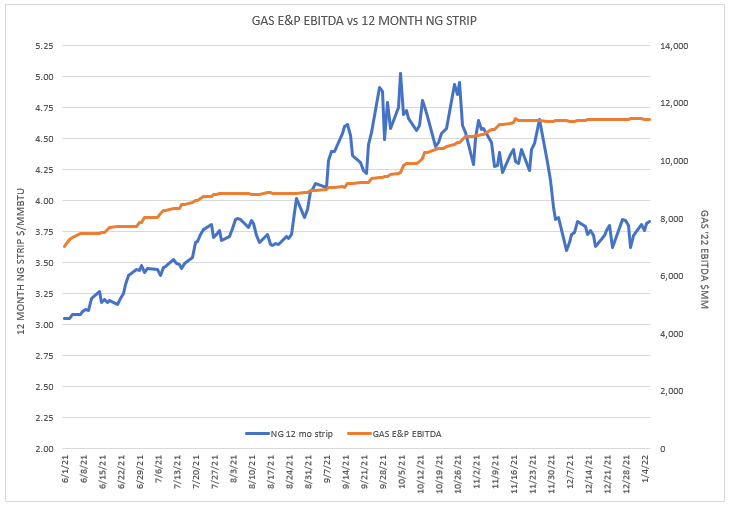

The big 5 nat gas equities ‘22 EBITDA estimates have plateaued of late. We look for these numbers to roll over soon (unless we see more deals like EQT and SWN prosecuted in ‘20).

We like this kind of setup. Fundamentals turning down. Equities oblivious. Buyside complacent. Long energy-short gas

Positioning/Trades

Pairs trades in the cyclicals space (long - short):

HES-OXY

LNG-EPD

CTRA-EQT

DAR-MPC

VLO-PSX

PXD-HFC*

MRO-APA*

CTRA-EQT*

OVV-RRC*

CLR-AR*

GPRE-REGI*

DBA-XOP

- DVN short

- AMTX short*

*new 1/6/22

- VR

viscoscityredux@gmail.com

Hi. Quite the sea-change between this article’s views and the March/April ones. Besides Ukraine, what changed?

What is your opinion of these bull arguments regarding US nat gas?

1. The number of drilled but uncompleted wells has been steadily falling, which means the same capex budget will soon lead to fewer completed wells: https://twitter.com/DoombergT/status/1487011406214053889

2. Producers are disciplined with their capex budgets

3. Tier 1 acreage is depleting quickly: https://www.resilience.org/stories/2020-02-27/peak-permian-oil-production-may-arrive-much-sooner-than-expected/ (sorry I don't have a more recent link)