Mosaic Theory

Maya Angelou and energy investing

Mosaic Theory in practice is putting together the pieces, gathered from a number of sources over an interval, to compile a view on the direction of a company or industry.

Earnings season can be a time for sifting through the rubble of reports to pick out potentially relevant piece of information to support or refute an underlying thesis.

We’ve learned through experience that management teams love to talk when the going is good and show little guile when the going is not so good.

“When someone shows you who they are, believe them the first time.”

Maya Angelou

The most mind-numbing part of covering energy can often yield the most valuable insight - reading earnings transcripts. We’re talking “evaporated-attention-span, brain-turned-into-congealed-pudding” kind of mind numbing. Yet, the process almost invariably yields something of at least marginal value.

We find it useful to hear what management teams have to say in response to the rare question from a sellside analyst that is neither a softball nor something that can be gleaned from the earnings release itself. We capture a few of these below from a select reading of last week’s earnings calls.

We precede each quote with our own context. That plus $3 (or $5 perhaps) are worth a cup of coffee depending on your city of residence. We have comments from upstream, downstream, midstream, and oilfield service participants below.

COP (Upstream)

Wow on the free cash flow

Turning to cash from operations, we generated $5.5 billion in CFO, excluding working capital, resulting in free cash flow of $3.9 billion in the quarter. For the full year 2021, we generated $15.7 billion in CFO, $10.4 billion of free cash flow, and returned $6 billion to shareholders

Going forward free cash flow outlook

We think it would be helpful for the market have an accurate sense of our stronger CFO generating capacity at a WTI price of $75 a barrel with a $3 differential to Brent and a Henry Hub price of $3.75. We estimate our 2022 full-year cash from operations would be approximately $21 billion … and our free cash flow for the year would be roughly $14 billion.

A thorn in our side has been the superficial bull case for energy based on “underinvestment.” Underinvestment and increased capital efficiency are at least in some measure being conflated. Prior to COVID, capex dollars were every year adding more reserves or production - full stop. Here’s a 2022+ case from COP showing another iteration of increased capital efficiency on its recently acquired RDS properties in the Permian.

The biggest opportunity in the near term is transitioning from 1-mile wells to 2-mile wells … the difference between drilling a 2-mile lateral on those properties and a 1- mile lateral, everything else being held the same, is a 50 basis point improvement on rate of return on well economics, which generates about a 30% improvement in cost of supply.

Thoughts on North America supply being revised higher

We put the entry to exit at about 800,000 barrels a day this year. And I think -- and in light of the last couple of announcements that I've heard, I would actually be moving that number up now. We're 800,000 to 900,000 probably barrels a day growth this year from the US and probably a similar kind of number coming out next year. This year dominated by the privates, with some influence by the publics. Next year, probably having that swap a bit and the publics kind of regenerating and coming out of a maintenance capital mode in 2021 and reenergizing, just like we are.

COP increasing their own North America activity

We plan to add some activity in all three of the big three, the Bakken, the Eagle Ford, and the Permian as well. The cadence of activity as we talked about before is kind of back-end weighted in the year. But right now, we're at 20 drilling rigs and nine frac spreads, and we would add approximately four more drilling rigs in the Lower 48 throughout the balance of the year.

Keeping an eye on upside risks to global supply, but inventories provide a bit of a cushion

And the fact that the inventories are down quite a bit globally and certainly here in the US. So, I think there's a little bit of time that we have associated with that. But certainly, if we're getting back to the level of growth in the US that if you're not worried about it, you should be, and be thinking about it.

Ugh, we hate to hear cyclical companies who produce commodities plan solely on using the balance sheet as a “hedge” during downcycles.

Yeah, we're unhedged. We think shareholders buy our shares because of the upside that it represents in the commodity price and the torque that we have to the upside in the way we set up the company. So no, we're -- we prefer to remain unhedged, and frankly, hedging would do little help. So, we have a very strong balance sheet, which helps us on the downside, and shareholders ought to expect full exposure to the upside that we're experiencing to date.

MPC (Downstream)

On stronger international gas prices contributing, in some degree, to strength in global liquids.

But if we stay in this $5 to $6 gas range, it will absolutely put pressure on those (European refiners), have that exposure and we'll look for upside, but it's one of many variables. But with that being said, what we're seeing right now out of Europe is just slight run cuts at best, because their margins are covering our higher OpEx costs. So we haven't seen the impact substantially yet. If it continues, I think that's another story.

What is an analyst to do when a company (at last) discloses capex for an in-flight project in the 9-figure range but won’t provide bookends on the EBITDA associated with the project?

Analyst: The follow-up is back on Martinez, thanks for the $1.2 billion. Is there a way to tie that into an EBITDA number, either with or without the blenders tax credit?

MPC: It is still a little early, what I was saying earlier is, we're still actively engaged in some feedstock discussions. So we can't go to that disclosure. We got to the point with our discussions that capital is now very open with everybody.

EPD (Midstream)

Indeed

We learned the hard way in April of 2020 that the barrels that come with a futures contract that doesn't have adequate physical infrastructure.

Starting to hear more chatter about sooner-rather-than-later need for incremental Permian gas processing/egress infrastructure. Not yet, but it’s coming. Who blinks and cedes economics first?

It feels like a lot of the majors in the bigger publics out there are fairly well set in terms of the gas takeaway capacity … they seem like they're in pretty good shape. So when it comes to basis, in the past, the private guys have probably been the last ones to step up for capacity.

Ultimately, somebody is going to need to step up or collection of people are going to need to step up. And every month that goes by without a gas pipeline being announced, it's just going to add the problem.

We talked to our customers about the potential for a pipeline project. But you know, right now, we haven't been able to get anything done on that side

But ultimately, the folks that are realizing $85 a barrel and the folks that are realizing gas prices at these levels and NGL prices at these levels. And in terms of how we go pitch projects, those are the ones that probably need to step up. Can we be complementary to it? Possibly. But to me, ultimately this is about producer stepping up to get this project done.

NGLs are getting on boats to Asia.

The market for the incremental NGLs from the United States, which are substantial. It is going to be at the dock. There's just no doubt about it. We're going to say they're largely pointed towards Asia. Am I missing something?

Surprised by recent Permian activity announcements, looking at 2nd tier drilling accelerating

Obviously, the publics remain very committed to discipline. That said, if you look at what Chevron has said in the last couple of days, you look what Exxon said this morning, the Permian is their hot basin and then both going to increase activity there for 2022 and beyond. The other thing that's very hard to get your arms around is there is a lot of acreage. And I hate to just use that term generically that's changing hands. And what I would call is Tier 2 acreage. And that will be drilled. The private equities are picking it up and the privates are picking it up.

When a fee-based business advocates for more commodity exposure ….

we think some of this is turning. But where there is an under investment in oil and gas globally, we just think from a structure standpoint, commodity prices will hold up well, and we just want up more exposure to it.

Marcellus relatively constrained between pipes & capex; sector dependent on Haynesville for gas supply growth.

I wondered 3 years or 4 years ago, where is the incremental gas can come from, is it going to come from Appalachia or Haynesville. Well, it's clear now that is going to come from the Haynesville. You know 50 rigs, 20 frac crews working.

HP (Oilfield service)

They want pricing uplift, but are having trouble getting customers to pay for it.

With commodity pricing hovering near 8-year highs, we're seeing an improving and tightening rig market. Against this background, average rig pricing has improved only nominally up to this point. Our customers have benefited from higher commodity prices. But from an oilfield service provider perspective and particularly as a driller, we need substantially higher pricing in order to generate the returns required to attract and retain investors.

Tired of ceding ground, planning on pushing pricing to upstream players

Leading-edge pricing and margins are growing as a result of super-spec rig demand and the need to offset the operating costs associated with reactivating idle rigs as well as other general operating cost inflation. Assuming oil prices remain strong, we plan to continue to push pricing in the coming quarters as the scarcity of readily available super-spec rigs becomes more prevalent.

Slowing pricing pressure on their inputs

We are still seeing some inflationary pressures on materials and supplies as mentioned last quarter, although some pricing pressures appear to be beginning to stabilize

This one gets to our struggle with oilfield services. There remains plenty of capacity, it just needs price to bring it in off the sidelines. How best should the market capitalize this latent capacity?

The significant US swing capacity can be deployed for the right economics of price in term duration … given the available idle rigs that can be deployed some time, we see no need for new build capacity on our mid to long-term planning horizon

Probably the biggest bottleneck to growth for us is just being able to get pricing at a level that makes sense to make the investments that we need to make in order re-commission the rigs.

One of the most fascinating trends in oilfield service the last several years is its persistent ability to put itself out of work via increased efficiency. HP has been trying some time to mitigate the loss in revenue they incur by drilling a well faster and faster (on a $/day fee). They are making ground slowly in getting customers to pay for performance.

It's been two years since we first started talking about new commercial models and changing away from the dayrate model and those for several quarters, it was pretty, pretty slow adoption… So there is no doubt that as you look at kind of a base revenue per day, that number has moved up significantly on the performance-based just like our spot pricing

Industry adding rigs

You have to also realize that just like last quarter, we put 27 rigs into the market. And again, hopefully this quarter, we'll be closer to 20.

And in other observations:

Russia Gas Exports

Hydrocarbons across the globe have been strong. Weakness in one may presage weakness in others. We’re not calling for it yet, but the trends in international nat gas warrant close scrutiny. Warmer weather and a Russian change of heart (?) are finding one of Russia’s nat gas export routes into Europe steadily ticking up.

Russian gas to Europe - points of European entry

The spike in inbound LNG volumes has also provided a measure of relief.

LNG to Northwest Europe

European gas inventories are still well below normal, keeping prices firm. The trend, ever so slightly, is towards less-tight inventories in the last couple weeks.

European natural gas storage inventories % full

Still quite strong, European and Asian LNG prices have trended down a bit lately.

Misc international fuel prices - $/MMBTU

DUCs. There are plenty of reasons to be constructive energy, but in our mind the inventory of Drilled Uncompleted (DUC) wells isn’t at the top of the list. The chart below, from JPM, reports DUCs spud from 6/1/19 to 11/1/21. Down from a peak to be sure, but the cupboard doesn’t look bare to us.

US DUC count by basin

Earnings check-in

Interesting mix of energy sector 1 day performance for the 4Q21 reporters so far. NOV a negative outlier on miss and performance, with MPC the opposite on beat and strength.

1 day price reaction (y-axis) vs earnings surprise (x-axis)

Though by 5d after earnings release, things are getting bid. Note though that a few of the names above have yet to reach the 5d mark post report.

5 day price reaction (y-axis) vs earnings surprise (x-axis). The sector is bid

Earnings reports of interest to us for the rest of the week:

2/8

BP CVE PSK AGCO CNHI DD LIN

2/9

PAA EQNR LBRT BG

2/10

EQT DCP TTE NESTE PBF PTEN

2/11

ENB

Finally, “Good Trade/Bad Trade” corner:

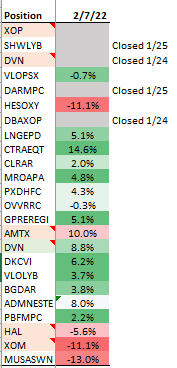

We try to document changes to the book whenever they occur. No changes since last week. Positions live in the book and cumulative performance.

(Live) good trade ~10%:

CTRA-EQT

ADM-NESTE

DVN long

(Live) bad trade (~10%):

HES-OXY

MUSA-SWN

XOM short