Monday Musings ...

Monday Musings ...

Added risk to Energy today - for a trade

Today we leaned into Energy long - for a trade.

To be clear, we are not in the supercycle bull camp. We think the long Value trade is misinformed based on precedents that do not hold in today’s macro cycle. We also think the long Energy trade is more backwards looking than forwards.

But we also like to trade. We take profits occasionally, to the extent we generate them.

And we trade around themes while holding longer term views. Today was such a day. We’re net long Energy for a trade - not an investment.

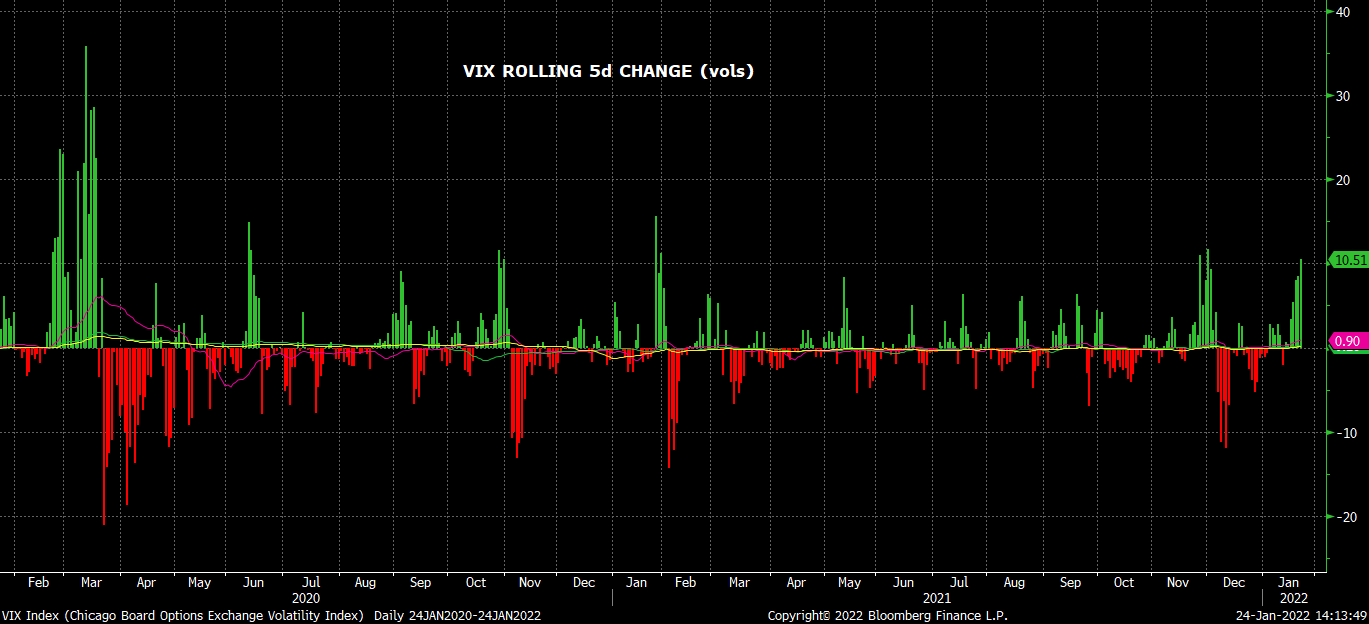

The VIX nearly kissed 40 intraday today. That level hasn’t been seen often since the COVID crash. And the ramp in VIX is new since 1Q21. Too much too fast. Time for a bounce.

VIX Index

Intraday, the rolling 5 day change in VIX, again measured in vols, was the highest since COVID came to the fore. That aggressive level of change and risk priced into the market signaled to us the likelihood adequately high levels of fear and the opportunity for a rebound in risk.

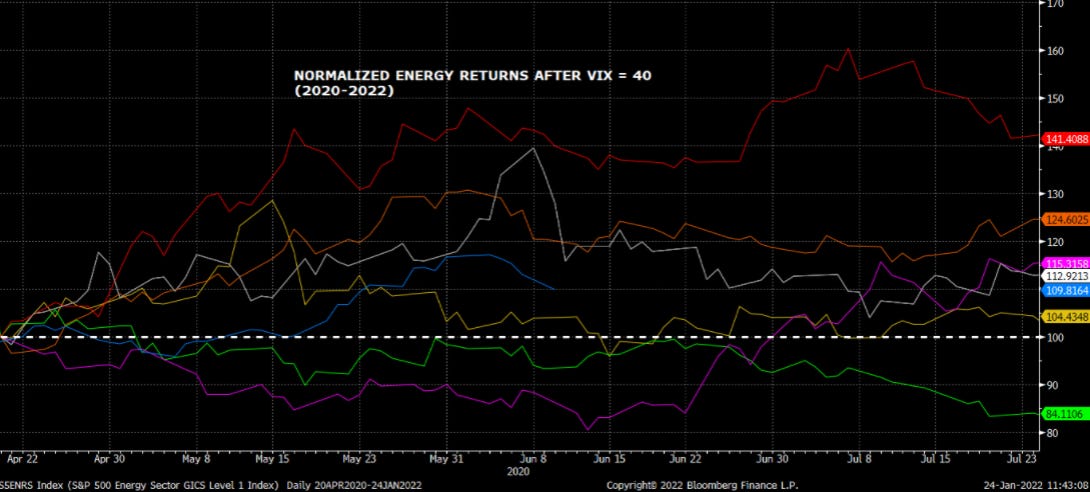

Below we looked at normalized returns for the Energy sector over the last two years after the VIX has neared 40. We like the risk/reward the precedents lay out.

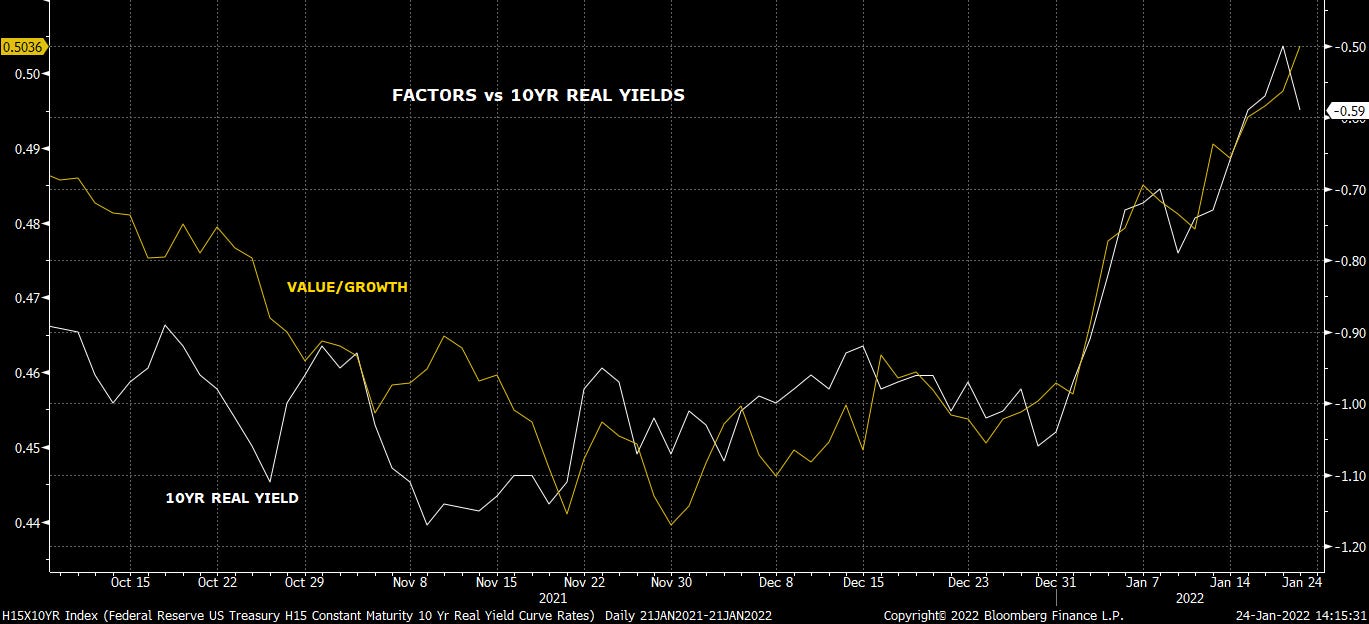

We expect real yields to keep trending higher until inflation peaks in late 1Q21 and the Fed begins to hike. As go real yields, so too goes Value over Growth. Energy is the beneficiary.

Hedge funds have been hit hard recently, and the losing performance accelerated in January. Losses from the long books have overhwhelmed gains from the short books. A few things make us constructive: 1) there remains over 11 months in the calendar year, plenty of time to make up underperformance, 2) hedge funds like to run net long, and will add to their long books here in pursuit of #1, and 3) funds are still very consensus in thinking Energy is in a bull market. They’ll follow one another and add to Energy length as they work on #1 and #2

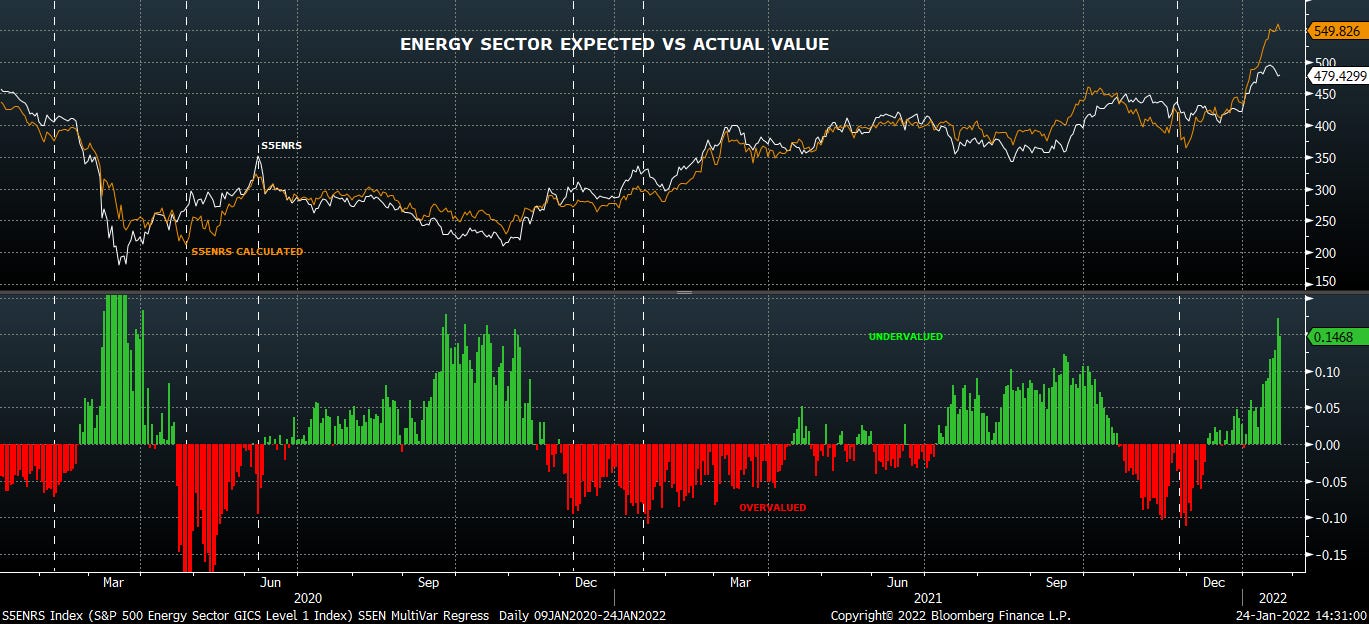

We’ve long held that the performance of the Energy sector is dependent on more than commodity prices and have constructed a multi-variable macro model to reflect this framework. We use outliers in expected vs actual value for the sector as a signal to add long or short exposure. Today’s delta between expected vs actual vis a vis macro inputs suggests a good risk-reward opportunity in adding length to the space.

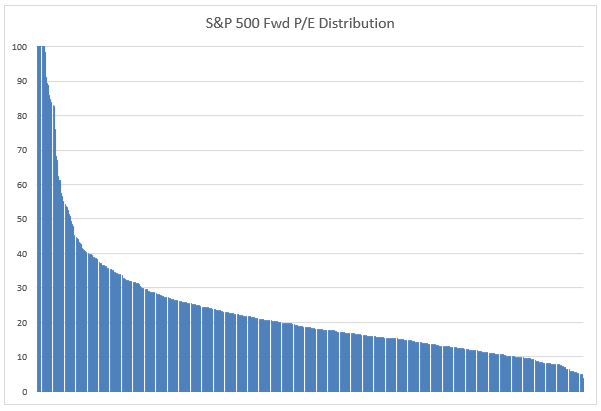

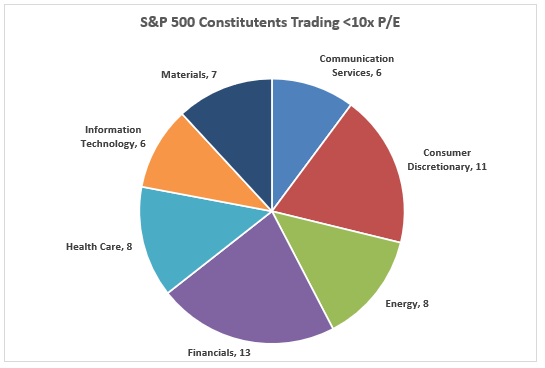

Looking at Energy vs the broader market, the gaps are too wide today and need to close to some degree. See below distribution of S&P 500 constituents’ forward P/E ratios.

We like using 10x P/E as a line in the sand for further scrutiny. Today some 59 members of the index trade below 10x. Financials - maybe. But this many in Energy - that’s too many for today.

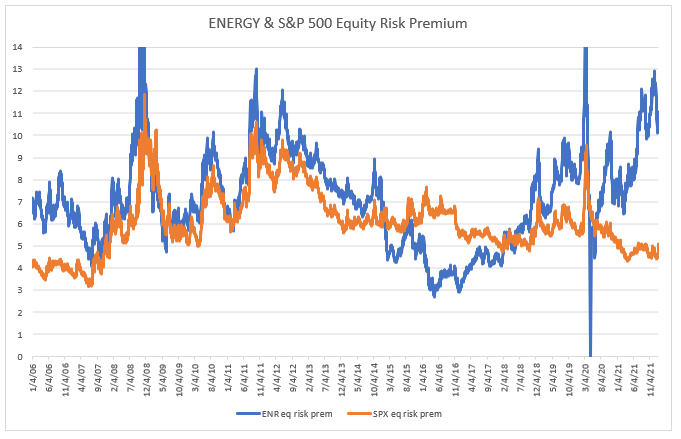

Finally, this chart comparing Equity Risk Premium (ERP) caught our attention. The Energy sector should in fact be burdened with a higher ERP than the S&P 500 due to a host of tailwinds the sector contends with. At 6 points wide, we think the gap is attributing too much risk to the group today and needs to close. We don’t call for a slight premium like in the pre-ESG days, but a few points narrower should be in the cards.

Positioning long-short (last update 1/7):

HES-OXY

EOG-COP

LNG-EPD

CTRA-EQT

DAR-MPC

VLO-PSX

PXD-HFC

MRO-APA

CTRA-EQT

OVV-RRC

CLR-AR

GPRE-REGI

DK-CVI*

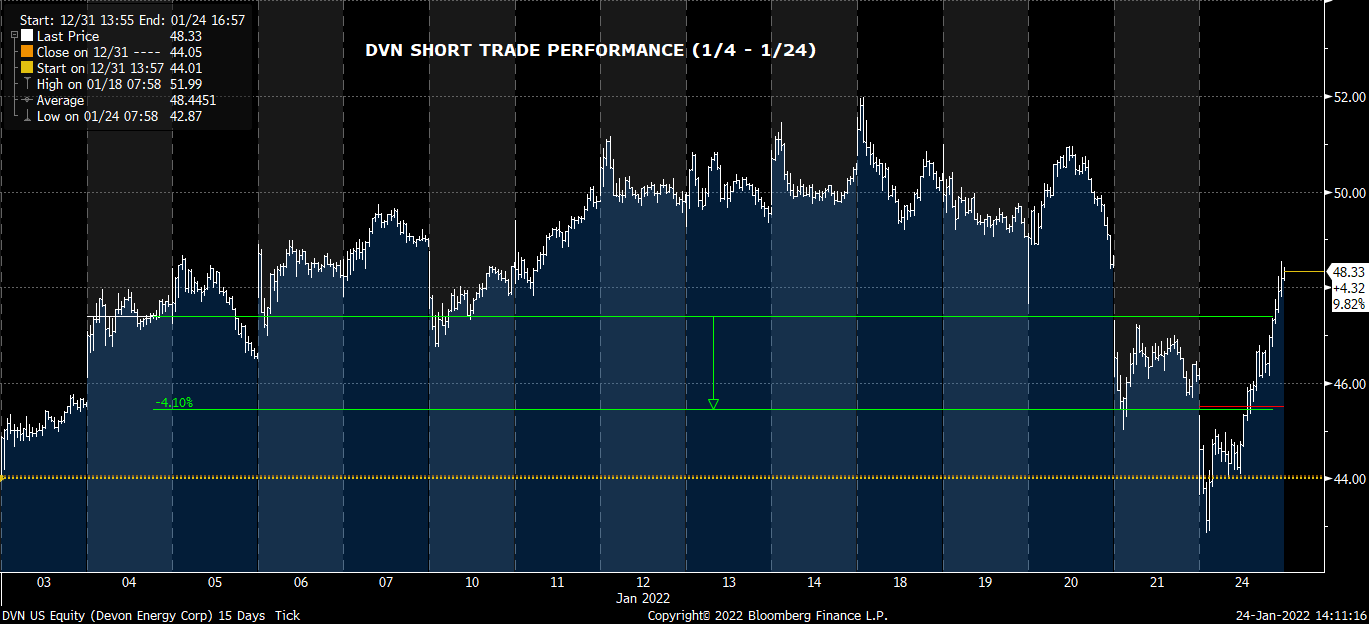

+ DVN long*

- AMTX short

*new 1/24

Trades 1/24

DVN: exit short (go long). +410bps VWAP-VWAP (1/4 - 1/24)

DBA-XOP: exit pair. +793bps VWAP-VWAP (1/5 - 1/24)

DK-CVI: new pair

Closed Trades Performance (VWAP day of entry - VWAP day of exit)

Viscosity Redux