Just sayin'

Just sayin'

It is our contention that Energy has been rallying on an understandable, yet unfalsifiable series of theses. Unfalsifiable - at least in the near term. Performance started in early December as the Santa rally and picked up steam once we turned the page into ‘22. Energy +20%, next best sector is +9.5% since then. Worst is Consumer Discretionary at -3%.

Normalized S&P 500 performance (12/1/21 - today).

Where are the (relative) opportunities, until the unfalsifiable theses are tested? The rising tide has lifted all boats. There’s been predictably little discernment - if it’s classified as Energy, it gets bought. Normalized YTD subsector performance.

On one hand it makes sense. Just buy anything that touches commodities, right? Though, eventually, the market will have to figure out if all of these companies make money when commodities go up (hint: no).

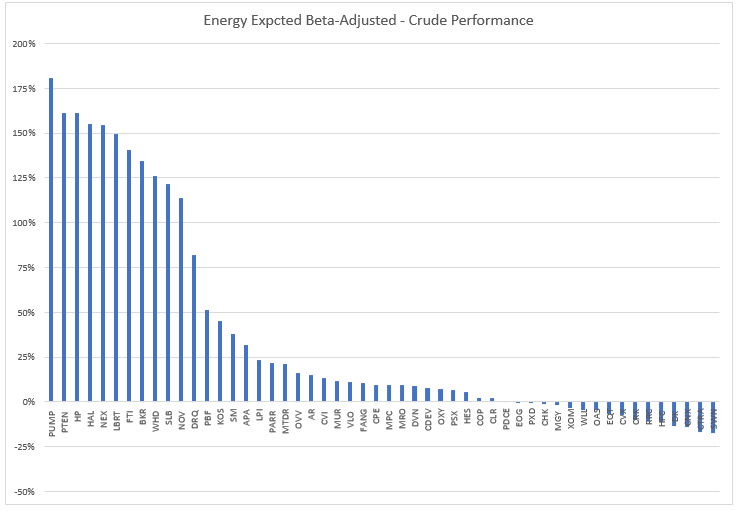

A look at which stocks have lagged crude is interesting. Chart below looks at actual stock performance, beta-adjusted, less crude performance. A positive value suggests stock performance has exceeded a normal relationship vis a vis crude.

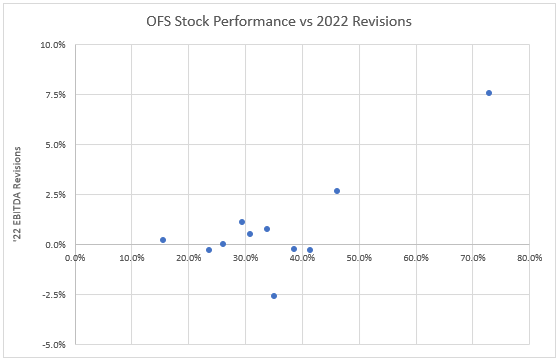

A lot of OFS names congregating at the “above expected” performance level. We suspect a couple things are at play here. First, and most importantly, the sector lagged in 2021 and you always have to buy the prior year’s laggards at the beginning of the year. They teach that at hedge fund school. We look at 2022 earnings revisions over the same period to see if that might be driving the outsized performance.

Not so much. Sure looks though as if every name was given a freebie +30% run and then relative performance was dictated by revisions. That outlier up and to the right? NEX, who did see a blip of positive revisions following a positive guidance update earlier this month.

So we’re going with some combination of buy-the-laggard and trade the hope for the strong OFS performance. Relative strength coming out of earnings will need to come from higher top line activity courtesy of increased upstream capital spending, with some level of margin expansion to offset cost inflation. For these reasons, OFS is not our preferred relative play from here.

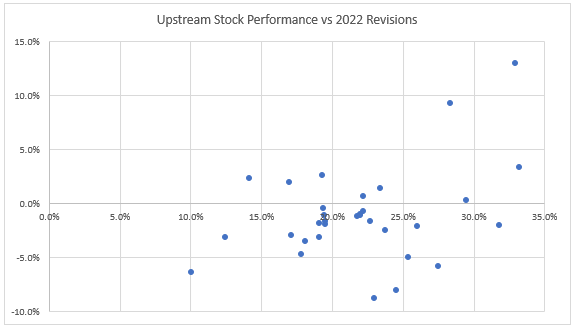

Other subsectors? Look at upstream next. Revisions since the beginning of the Santa rally have actually been negative.

Looks to be largely attributable to the drop in nat gas prices as analyst trued up their models towards YE21.

Since we don’t expect to see negative production revisions (at least on the oil names), we like the potential for positive revisions on this group.

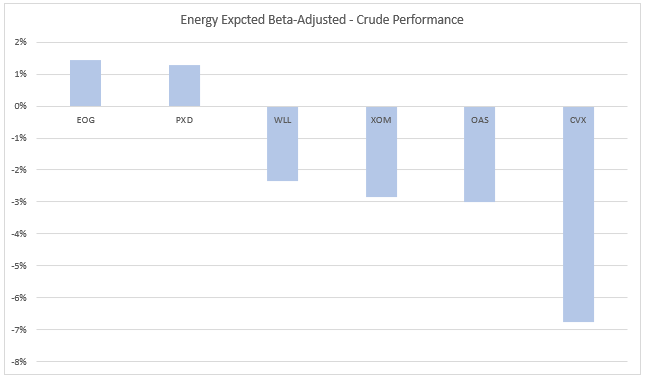

E&P names that have either underperformed or performed in line with crude (excluding nat gas names). Go figure - majors and good balance sheets.

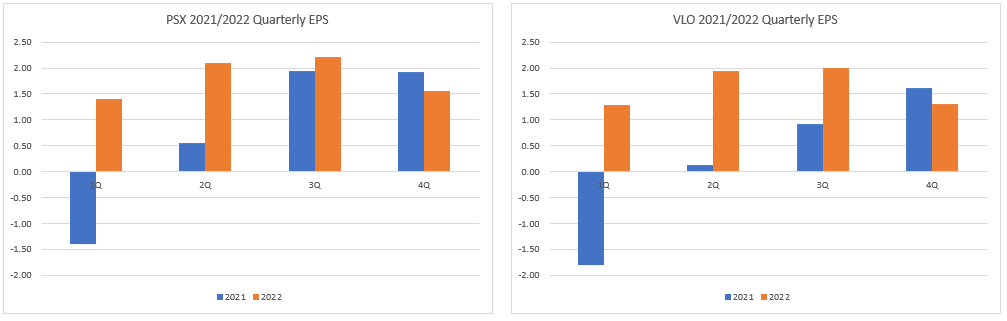

Downstream. Refiners are not E&Ps, a fact which at times is lost on the market - it is far from a foregone conclusion that a company whose main COGS is crude oil benefits when crude oil rises. Just saying. Nevertheless, when commodities go up, they invariably rally downstream equities.

Downstream revisions vs stock performance

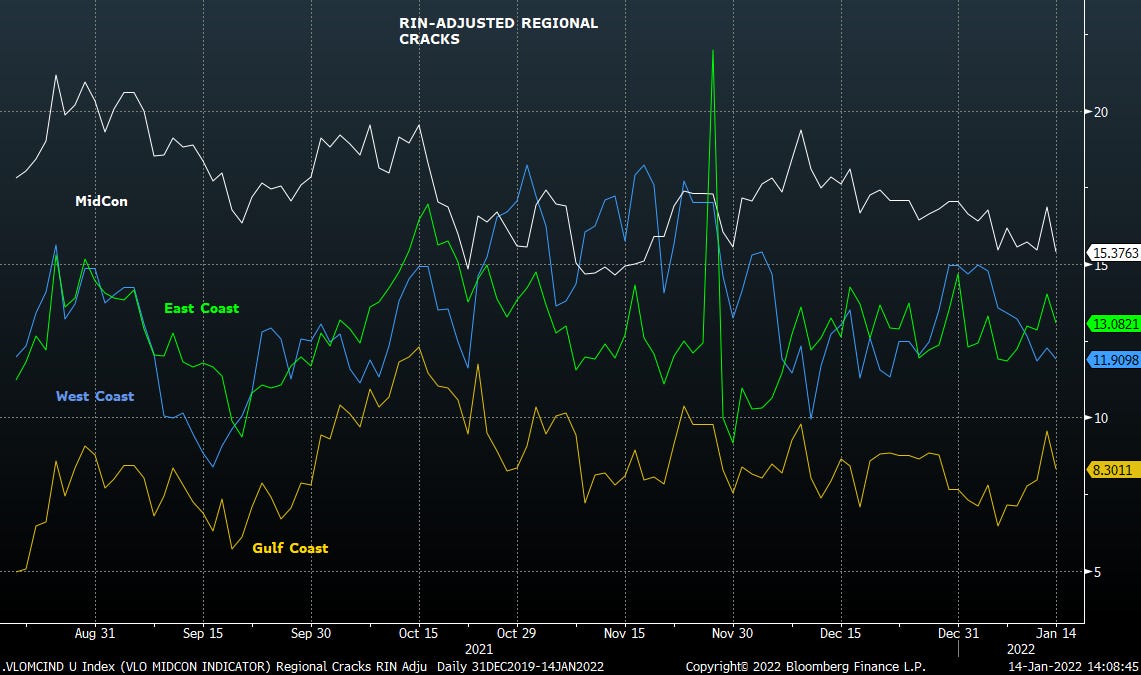

Here’s the thing though, refining fundamentals have not rallied with basic commodity fundamentals. Simplistically, refiners buy crude and turn it into products like gasoline and diesel. An economic operation finds the cost of turning crude into products is less than the price difference between outputs and inputs. That price difference, show below, is the refining crack.

The takeaway from the chart below: fundamentals aren’t improving, even if equities are moving. Refining is not improving and is arguably weakening. Which would make sense conceptually because the industry is oversupplied globally.

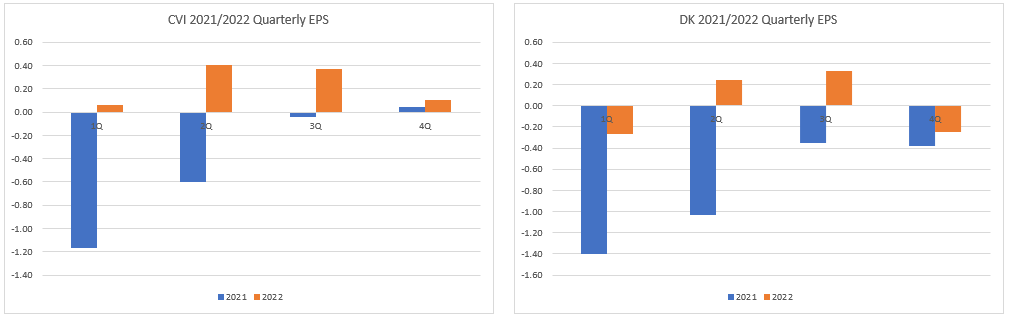

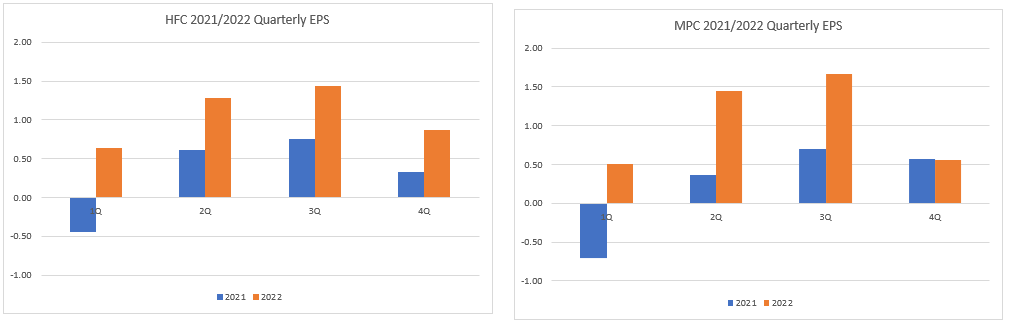

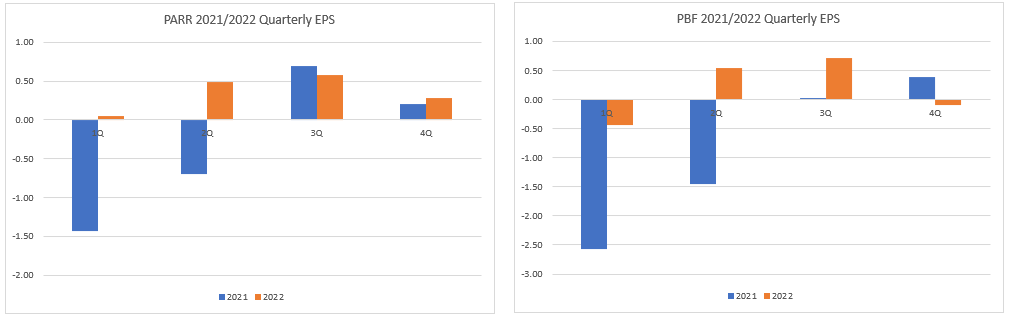

And the earnings estimates below - we’ll take the under on any of these guys closing the laughably large y/y gap between quarterly earnings 2021 vs 2022. In fact, it would surprise us none at all if, come as soon as 2Q22, the group is staring at year on year declines in earnings, as opposed to MEGA GROWTH.

Our conclusion: we prefer E&P over refining. OFS may see pockets of positive revisions, but the battle for net earnings increase is an uphill one as it will be hard for them to push pricing much beyond their cost inflation.

Back to the beginning of the post: the sector is rallying on unfalsifiable premises; namely Energy is a beneficiary of increasing inflation environments and the crude market is tight, really tight.

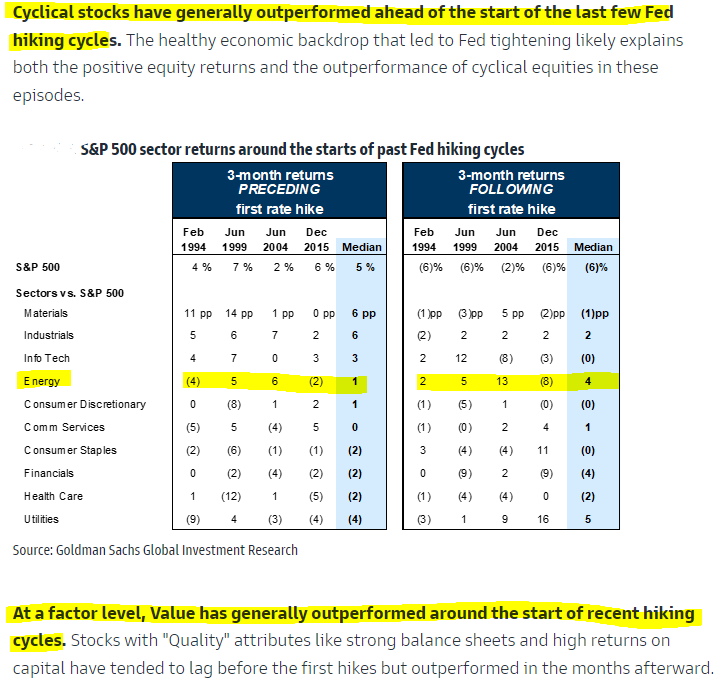

To wit: a typical example of the daily barrage of sellside research remind market participants to add length in Cyclicals (especially in Energy due to its [cough cough] idiosyncratic supply/demand tailwinds) and reallocate to Value. Because that’s worked in the past and every hiking cycle is the same.

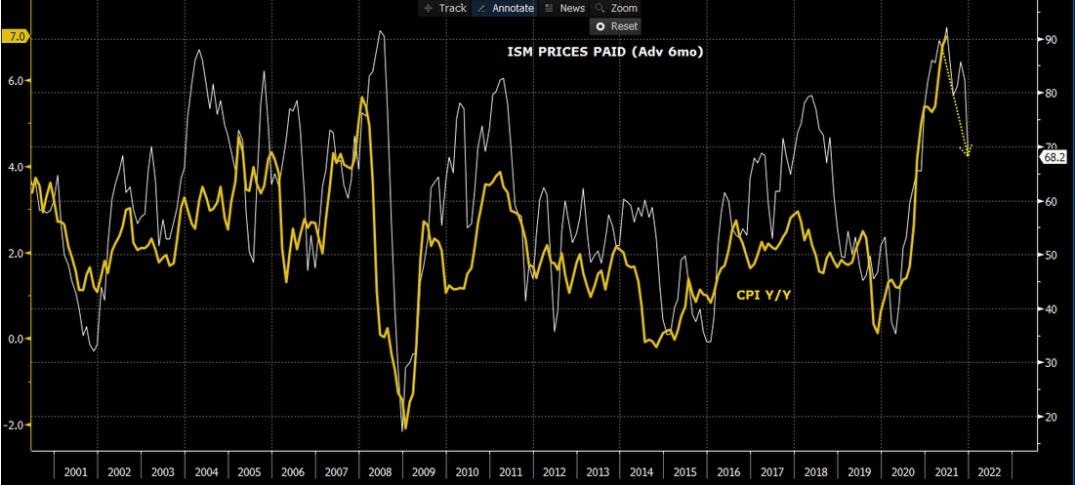

It’s rates and inflation. In prior cycles, high oil prices caused high goods/service prices; this cycle it’s inverted. But that doesn’t matter right now. Not until the thesis can be tested.

It will be though. As we keep mentioning, inflation will turn down, sooner rather than later.

Funny thing is, it’s not a secret. That inflation will be peaking iss understood, but it won’t be internalized until it’s happened. It’s been a backwards looking market for a while.

And what about inflation and energy? Energy earnings have in recent cycles peaked alongside CPI. Which peaks this quarter. Just saying.

I think this trade can work into late 1Q. No falsifying tests ‘til then. But by then we’ll see peak inflation and have to ask the sellside to tell us what works when inflation is falling (not Energy) and have to grapple with increasing global crude inventories.

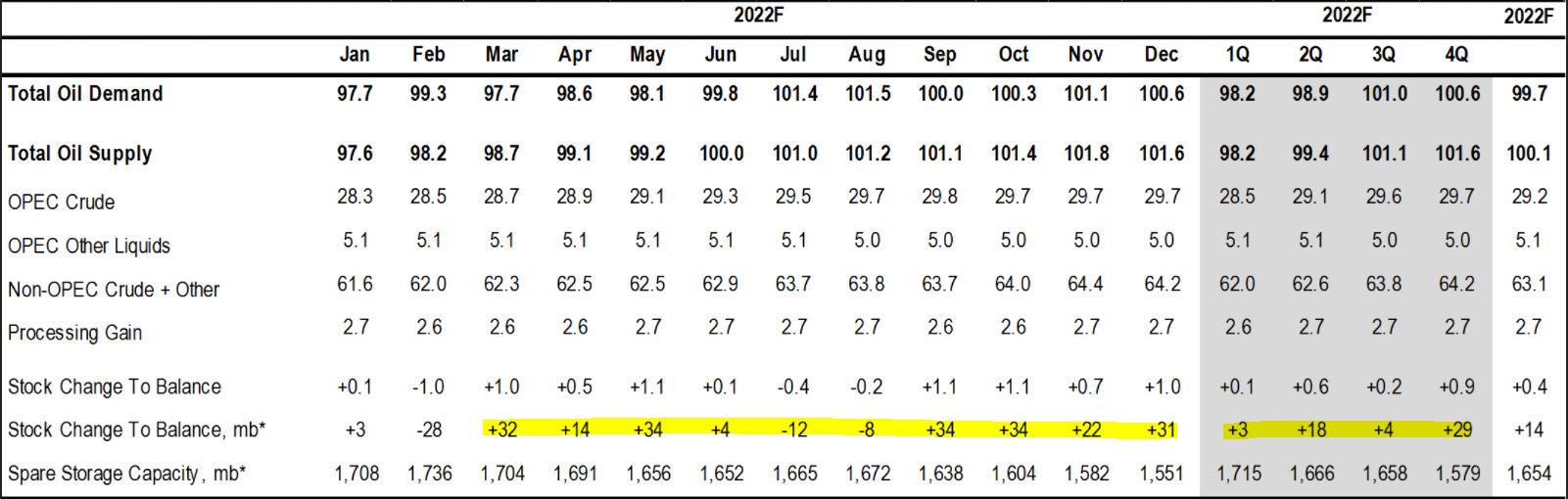

Daily update from a bullish commodity analyst - showing crude builds from March ‘22 onwards and upwards.

It is not time to go short the space (famous last words). At least that’s what we think. This narrative should hold into late 1Q, but by then have to confront some thesis-challenging data from the macro to the micro.

We’re watching a number of data points to look for leading edge weakness - a basket of equities and data we expect to roll first and serve as the portent of further weakness. This index is not rolling over yet.

In the meantime, keep in mind that this trade is very crowded, hedge funds are already down handsomely YTD, and conviction is a commodity in short supply.

VR

viscoscityredux@gmail.com