Fedfake (?)

Fedfake (?)

DOEs, Russia gas, Earnings, Positioning, and a trite comment on the Fed

Don’t read too much into market reactions 1) in the first 10 min after the Fed announcement, and 2) whatever happens from then to the close.

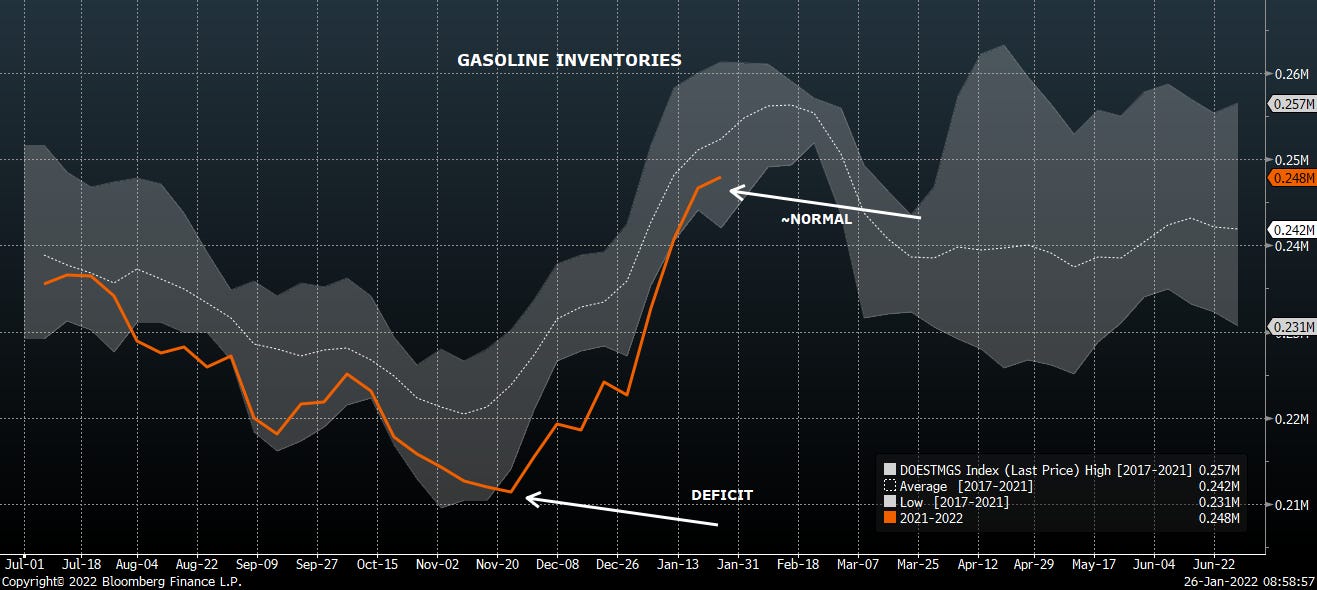

DOEs

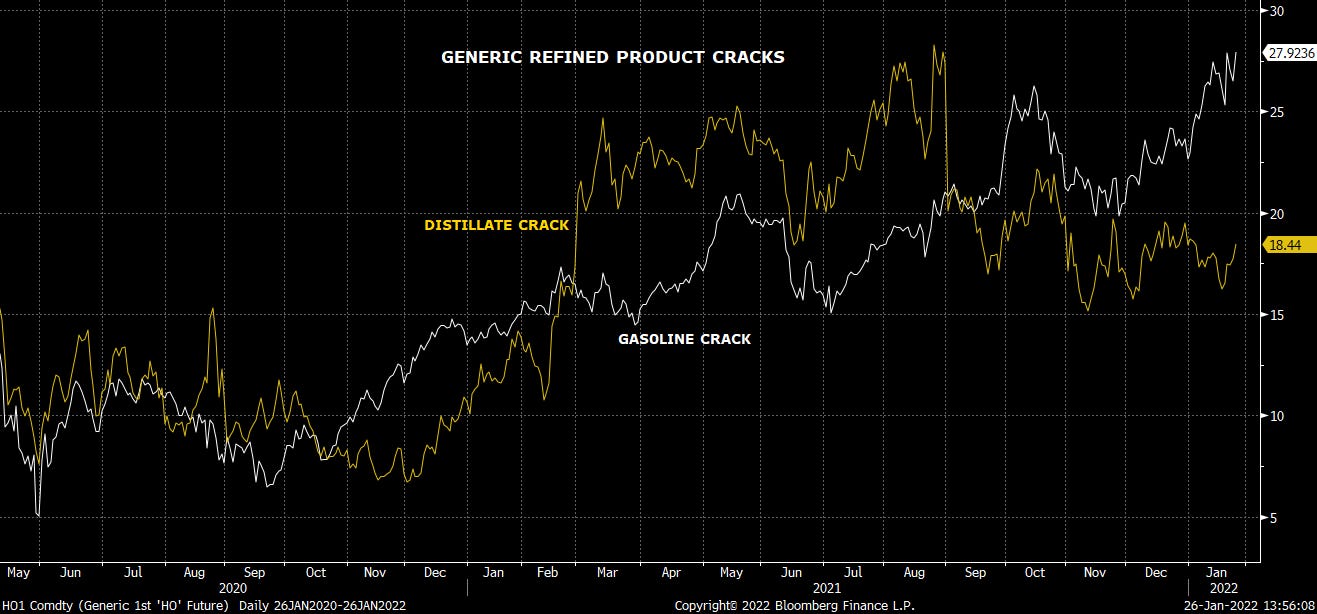

We’ve been harping on the discordance between gasoline and distillate product markets. Distillate is tight, gasoline is not - at all.

Only two months ago, US gasoline inventories stood at a material deficit to the 5 year average and were even below the low end of the lagging range.

The deficit versus the 5yr average gasoline inventory level has closed markedly since early December ‘21. Inventories have gone from 94% of the 5yr average up to 98-99% in a few weeks.

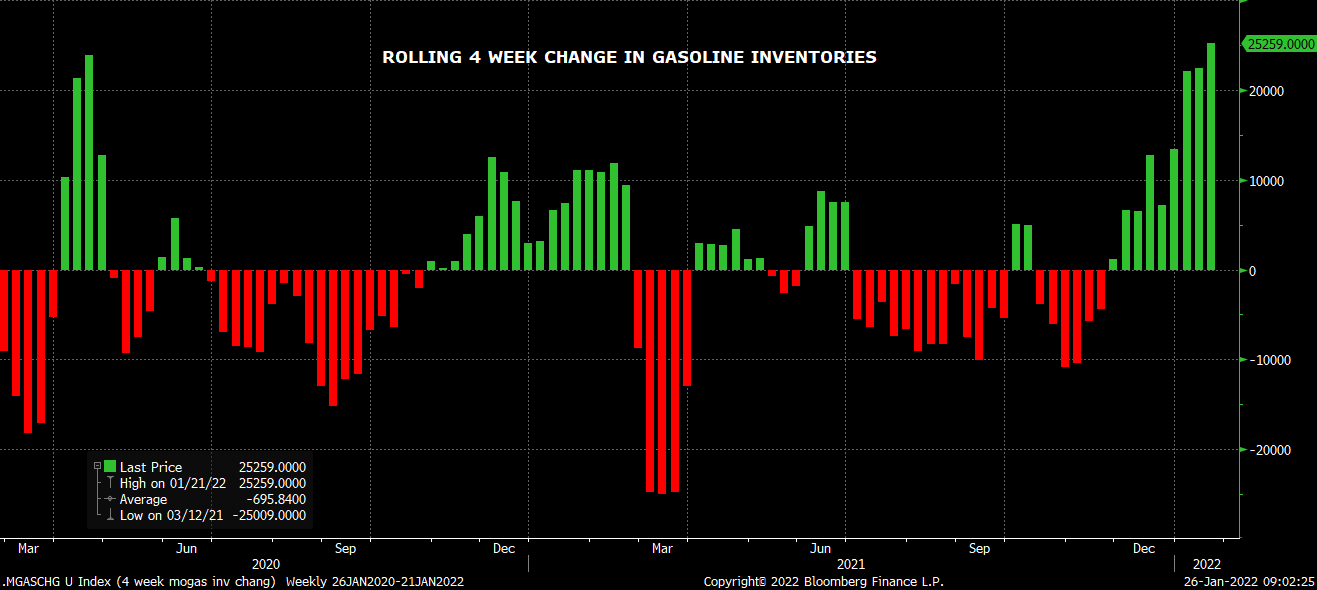

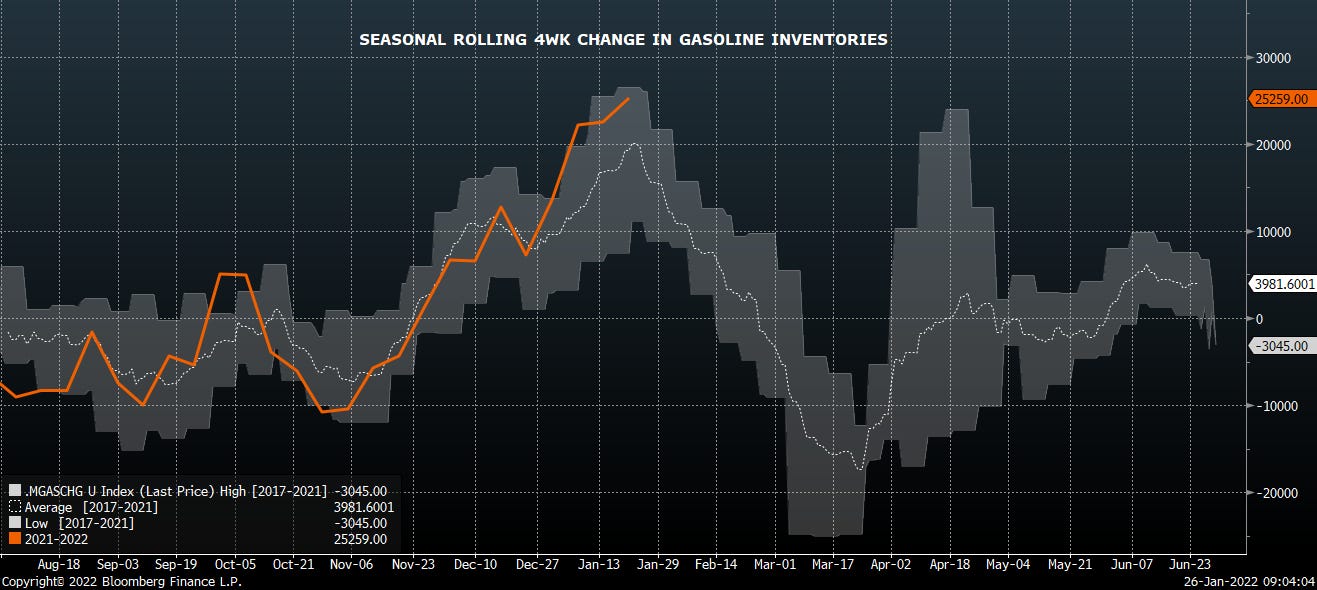

The market does tend to build gasoline inventories during this part of the year, but the last several weeks of builds have been well in excess of normal.

The market has built inventories as it seasonally tends to, but the pace of builds has well surpassed normal. Draws should seasonally in a few weeks, but the starting point of inventories will be a headwind.

Distillate on the other hand is tight.

This is what’s propping up the crude market, not a shortage of crude oil. The strength in distillate is what is keeping refiners showing up to work today. As long as distillate cracks stay strong, and gasoline cracks don’t implode, we think crude can hold its own.

But we continue to watch for looseness starting near the end of 1Q22.

Other Energy Stuff

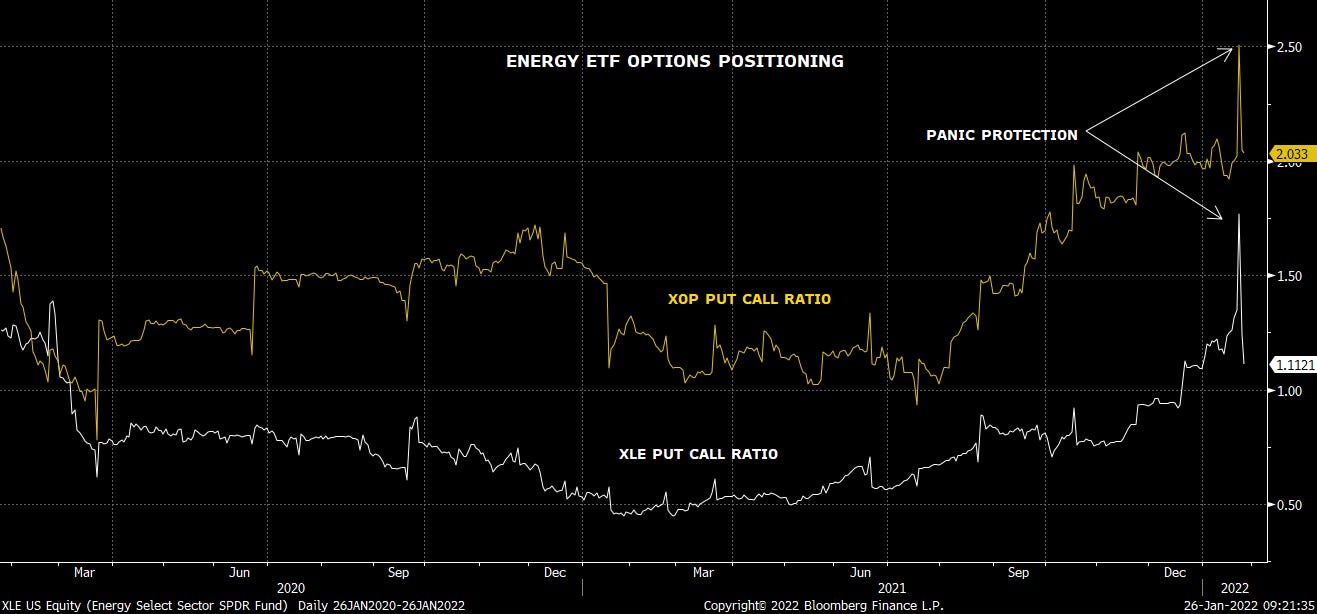

Check out the chart below on Put/Call ratio in the two largest Energy ETFs, XLE and XOP. Pay special attention to the panic protection purchase when the indeces sold off last week 5-8%.

The spike in put purchases has been quickly unwound this week and provided serious fuel to rally the space. We’ll watch this for the ratio to hit a more normalized level.

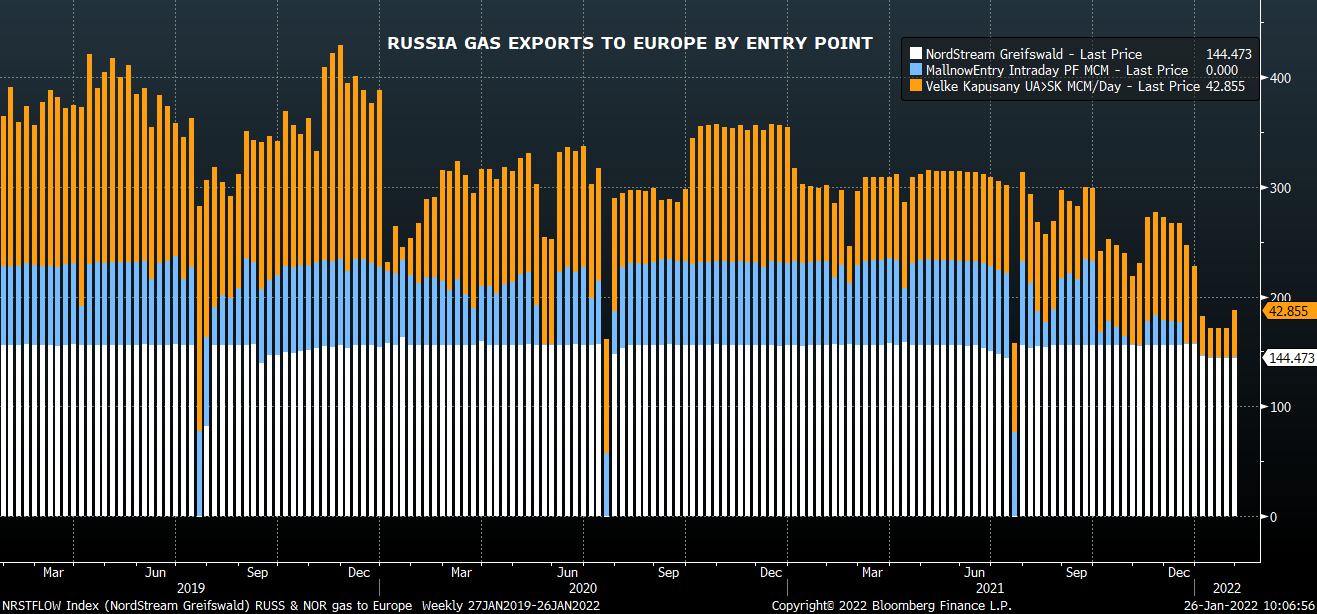

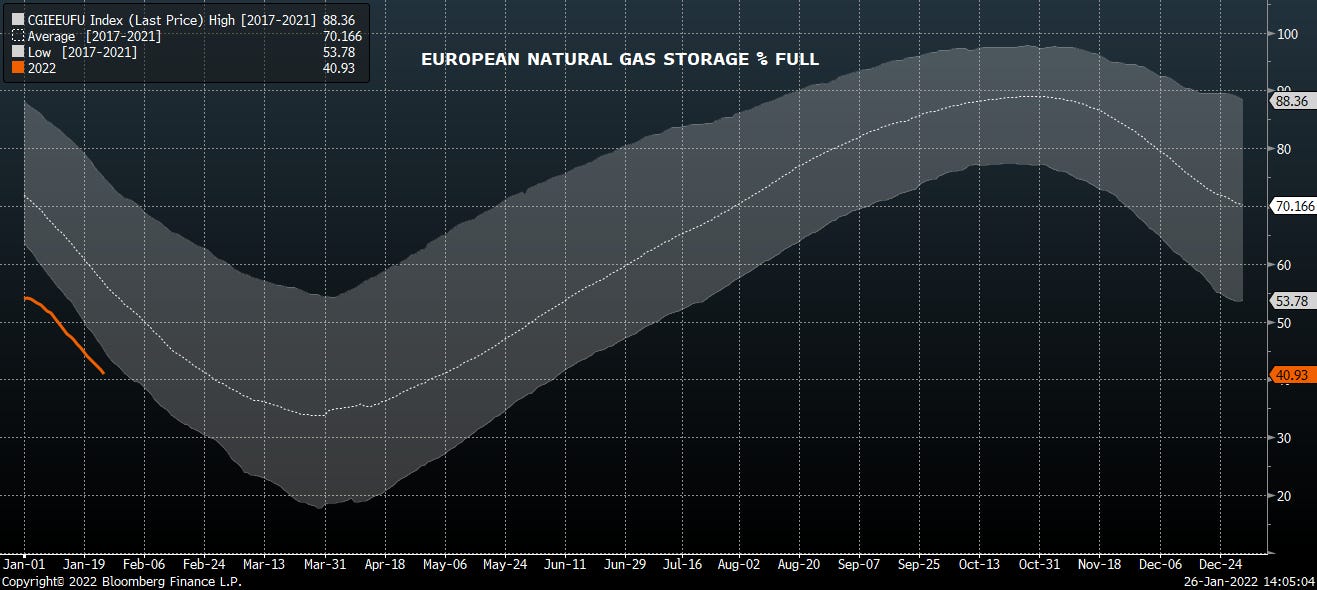

Russia gas

As we flagged last week in our natural gas note, European gas prices are one of the big drivers behind strength in the overall energy complex.

With the rally in European gas prices attributable largely to a year on year deficit in imported Russian natural gas volumes.

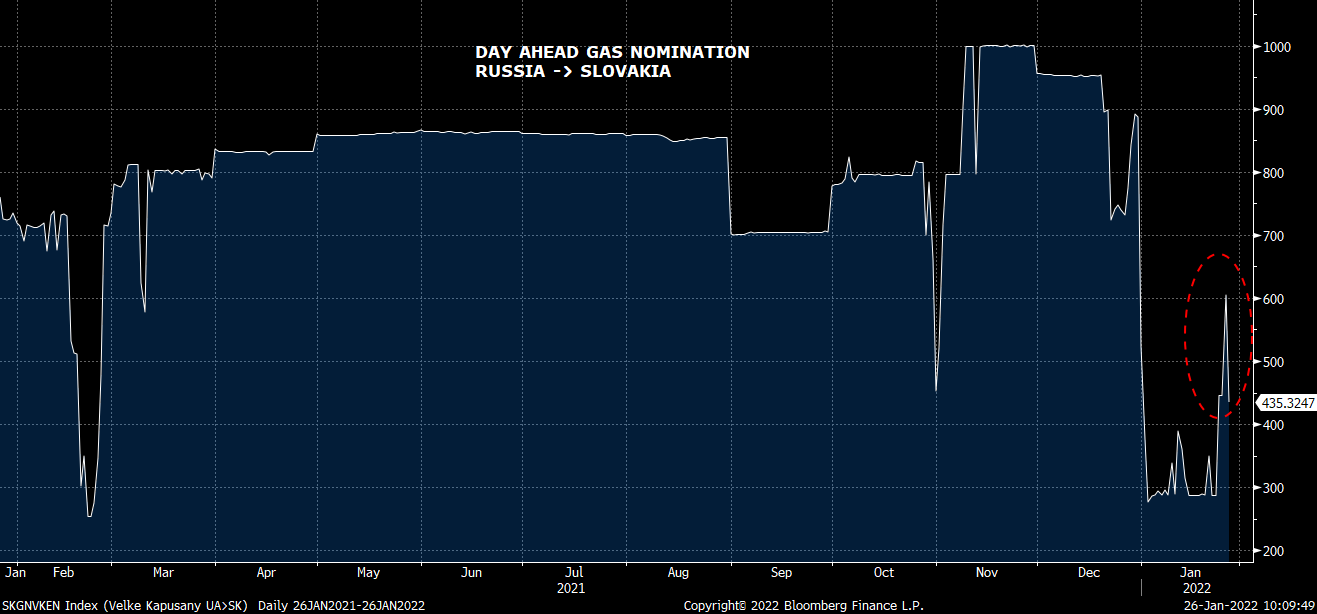

Today, a possible, potential ray of hope on the Russian gas front when nominations for one of the entry points into Eastern Europe (the blue wedge in chart above) picked its head up for the first time this year. Why it happened today in the midst of Ukraine tension and whether or not it’s sustainable is above our pay grade.

But any uptick in volumes will be most welcome in Europe where storage volumes at 41% of normal capacity are well below the normal ~56% range.

Earnings

We haven’t talked much about earnings for the following reasons:

If you gave us a company’s press release and full financials beforehand, we honestly would have no conviction on how to call the stock reaction when it starts trading. So much more comes into play now than just an EPS beat/miss

Derivatively, we flippantly say we don’t care about the earnings. We care about how the stock trades after the earnings are released

So we focus on #2, informed by #1. As is our wont, we love to use precedents and macro input when selecting equities, not necessarily eschewing the minutiae, but weighting it more appropriately.

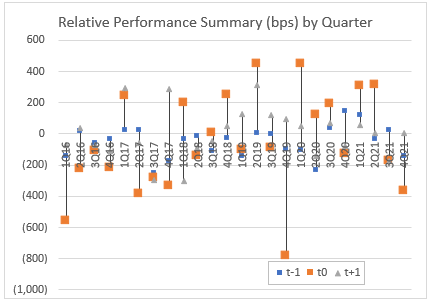

The first upstream producer out the gate, HES failed to impress despite an earnings & cash flow beat. The market was presumably underwhelmed with forward guidance and took the name down.

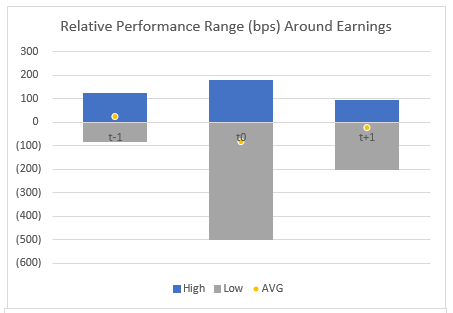

Below is a quick chart showing HES performance relative to the peer group in/around earnings over the last several years.

t-1 = day before earnings call

t0 = day of earnings call

t+1 = day after earnings call

Two quarters in a row of underwhelming performance on the earnings release. We like the assets, but don’t like owning the name on the quarter. Why did we own it today? Shrugs shoulders.

HES historical earnings performance

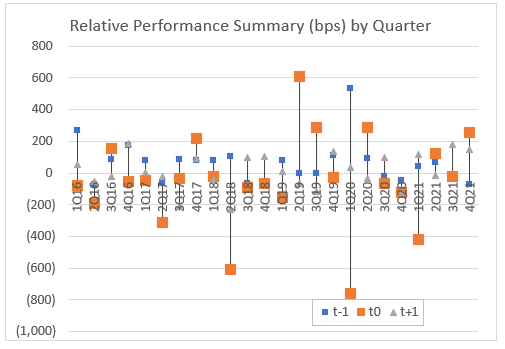

Contrast HES performance with the big 3 OFS names who’ve also reported 4Q21 earnings below:

BKR. Decent turnaround this quarter after poor run.

HAL avoiding earnings meltdowns the last few quarters.

SLB meh quarter again. Every quarter is meh apart from the outlandish 1Q20 print.

Trades 1/26

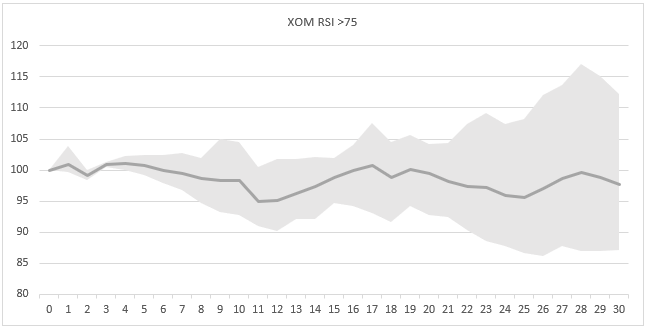

Speaking of earnings, we’re adding an XOM short ahead of their 4Q21 release next week. 4Q estimates have come up enough to taper the risk of an upside surprise and the name just has a habit of not knocking the cover off the performance ball when they report.

In a technically overbought position going into earnings, we like the probability of the stock giving back some of its recent strength.

Normalized XOM performance after touching 75 RSI

Also adding HAL short today looking for a pullback. We like the recent precedent of equity weakness after reaching RSI near 70. Short term trade.

With the sharp drop in put/call ratio, it looks as though a lot of protection has been unwound at this point and much of the associated buying pressure is likely to have dissipated.

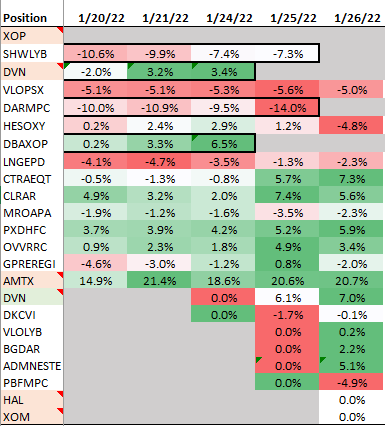

Live Positions & Cumulative Return