DVN: That's a ton of cash

Do not succumb to temptation

We understand the underlying rationale behind variable dividend models - wherein management teams wanting to demonstrate a commitment to returning capital. But, seasoned and cynical energy investors that we are, dread the day when companies have to cut the variable dividend because commodity prices (and cash flows) declined.

That day is not today.

Devon has wholeheartedly embraced the variable dividend model. Alongside their 4Q21 earnings release, this $51 stock announced a $1 fixed+variable dividend based on 4Q results. Atop the dividend, they upped their buyback authorization from $1 billion to $1.6 billion, having bought back $600mm in 4Q21 alone.

DVN generated and distributed a bunch of cash last year. $4.9B cash from operations funded $2B capex, $1.3B debt reduction, $1.3B dividends, and $0.6B buyback. Cash at YE21 was effectively flat vs YE20 even after these moves.

DVN 2021 Sources/Uses of Cash

A very encouraging sign to us, DVN’s 2022 guidance follows CLR’s earlier today with a muted production growth trajectory. 2022 guidance is set for 570-600 mboed, rather flat vs 4Q21 at 611 mboed. Praise be.

Capital discipline is holding and that’s a big deal for these big producers.

DVN Actual/Forecast Production

It should come as no surprise that commodities are stronger in ‘22 so far vs ‘21, so DVN’s $4.9B cash flow last year is most certainly headed upwards. Capex is guided to only $2.1 - 2.4B for this year.

When we stare at numbers like this and get ready for the sellside to ask any iteration of “what are you going to do with all the cash?” our preference for conservative energy management practices leads us to debt reduction before all else.

Not this year. DVN is arguably underlevered today and will be more so by YE22, provided commodity prices hold. We aren’t calling for further debt paydown (though it would be nice all the same).

DVN Deleveraging Trajectory (strip pricing)

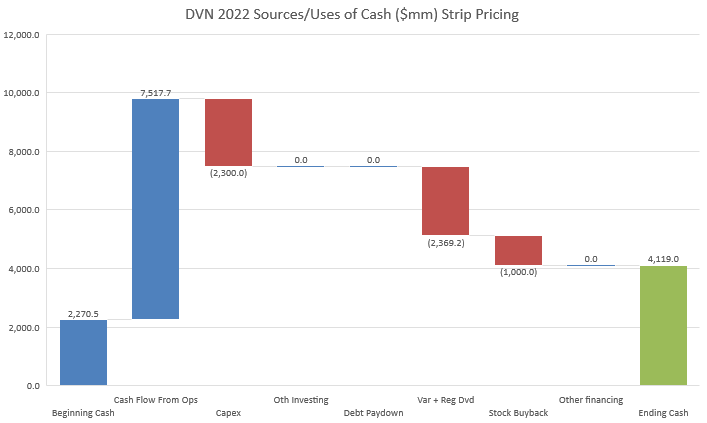

Here’s how it shakes out for us when we plug in Devon’s guidance. As the chart below shows, under their capital return framework AND strip pricing, Devon is building cash every quarter even after capital returns. This analysis assumes:

Strip pricing as of 2/15

High end of DVN capital budget guidance

Co completes the $1B left on their share buyback authorization by YE22

Co approaches, but doesn’t exceed (yet) their fixed+variable dividend governor (up to 50% of excess free cash flow after funding the fixed dividend goes to the variable dividend)

DVN Quarterly Cash Outlook (strip pricing)

Under the assumptions above, DVN returns $3.4B via dividends and buybacks in ‘22 and still builds nearly $2B cash on the balance sheet - under strip pricing.

In other words, ceteris paribus, DVN may feel comfortable enough later this year to further augment its shareholder returns IF it doesn’t chase higher production with more capex.

DVN 2022 Sources/Uses of Cash at strip

$3-5B capital returns is a big number. They’ll never get a “yield” like a constant, non-cyclical, non-variable dividend payer, but these are dollars coming back to shareholders all the same. At the close today, Bloomberg shows $35B market cap and $39.4B total enterprise value. Not a bad yield at all - risk it though.

DVN Enterprise Value

We remember well a period in 2014, pre OPEC circular firing squad, where EOG was supposed to generate absurd amounts of free cash flow based on analysts models. It was so much cash, incredibly compelling. Of course, it didn’t materialize. We take these extrapolations with a grain of salt, because it is Energy after all.

“Don’t screw this up”

I think even the most bullish know it cannot be treated as a normal, recurring dividend stream designed to grow over time. These are designed to grow some of the time and shrink others. It has to trade at a higher yield than conventional dividend streams - what kind of yield delta is what the market seems to be working through.

How do you think market participants are risking that dividend piece as it relates to forward strip expectations? Ie. back end of strip coming down and associated flow through to div sustainability